Altisource Portfolio Solutions - the blood in the streets update

Shares are down 23.5% today and down nearly 70% from a recent peak. Is the company going banrkupt?

So, is ASPS going bankrupt or what? The short answer is maybe, but not tomorrow. I bought this name in 2021, sold some calls on spikes, got shares called away, and after the recent action, I’ve moved back in with some common shares.

The sequence of events for why Altisource crashed seems to be the following:

Calvin's thoughts is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

- People who didn’t know what they owned pumped the name last year

- Seeing the share price spiking like crazy, the company filed a shelf offering to do an ATM

- The company hired Guggenheim to help it restructure its 2024 maturity wall and Twitter jumped to Chapter 11

So first, let’s check and see how things have changed since my initial bullish call in 2021:

First, we can see that the Pointillist sale (i.e. when Altisource sold a cash drag minority revenue contributor unrelated to their core business to net $100M) had a huge short term impact on the company. At the time the sale was announced (Q3-21), Altisource was adding debt, bleeding cash, and had deeply negative operating income. At the time the sale was announced, any observer would have said “this company only has less than a year till bankruptcy.”

And then - a miracle. Cash increased, debt decreased, and losses narrowed. Fast forward to today and we’re back in panic mode. Receivables are tracking down - which could very well mean more decreases in revenue ahead. A debt maturity wall (their entire debt profile) looms just 15 months from now. Between the equity offering and the possible debt restructuring, the market is super spooked. I saw long term bulls puking their entire position today. Yet I was buying. Why?

Revenue realization lags, insider support, and operating environment changes

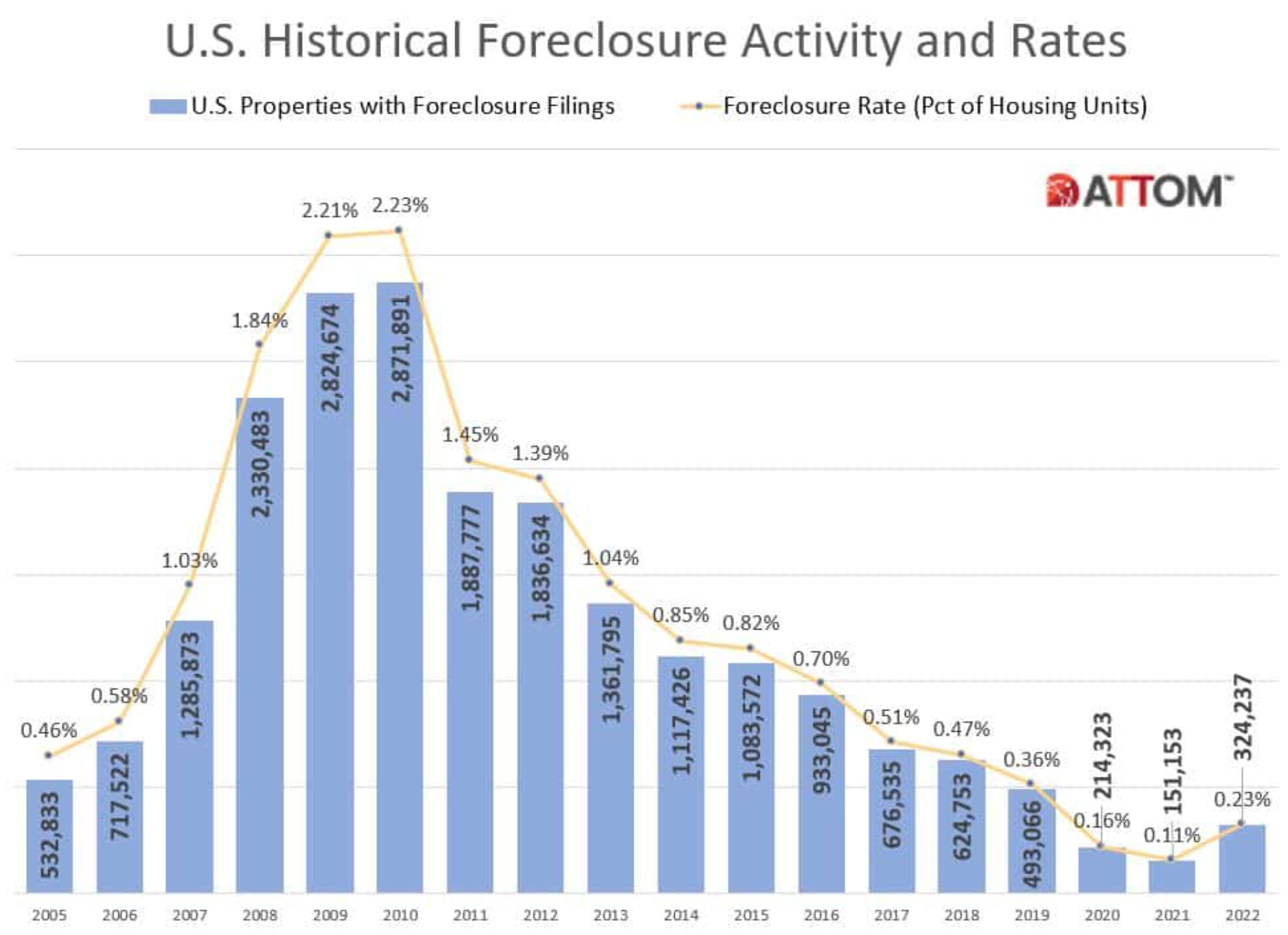

The first thing I want to say is, this company is out of my core competency. There are people who are very competent in this area (distressed debt, mortgage servicing, etc.) that think the company is a dumpster fire. So take what I’m about to write with a grain of salt - I may not know what I’m talking about. That being said, let’s start with a chart:

The rate of foreclosures in the US hit unimaginable lows in 2020 and 2021 after falling for a decade. Altisource’s core business is processing foreclosures. As you can imagine, it’s hard to make money when the industry you operate in is seeing those kinds of declines.

But - after bottoming in 2021, foreclosures ticked way up in 2022, and really weren’t all that far behind 2019 levels. So while the operating environment for Altisource is still pathetic, it is at least trending in the right direction, and despite the continued drop in revenue, Altisource has at least managed to reduce operating losses from 2021. That being said, debt is trending up and may continue to trend up, and revenue is trending down and may continue to trend down.

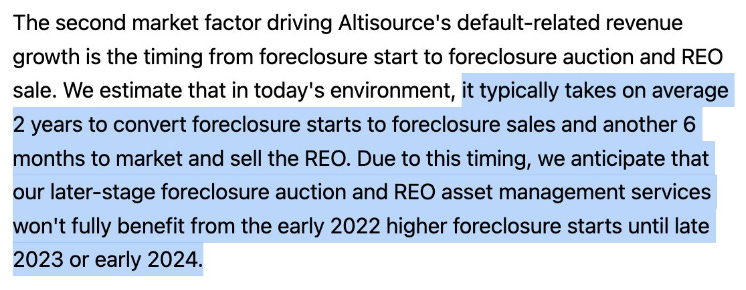

The revenue lag

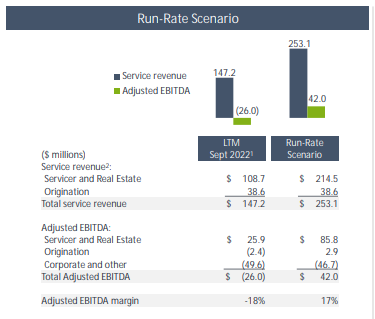

Here is a snippet from the last Altisource conference call. Foreclosures were basically illegal until Q2 or Q3 21 in the US. We are still seeing pandemic effects reflected in today’s numbers. Here are the estimates on a more normalized scenario:

$42M in EBITDA on a stock trading at $100M whose primary revenue driver is at its cyclical lows (2019 was an all time low year for foreclosures before covid hit) is somewhat attractive in the world of cyclicals. Even after the $15M in annual interest payments (and assuming an extension can be made), the debt disappears pretty quickly in a more normal scenario.

Now again, I’m just assuming what management is saying is accurate, and this is a management team in a business with cyclicality going against them for the past decade, who have constantly revised their projections lower. The controlling shareholder was basically convicted of backdating past due notices to start eviction proceedings sooner and lost most of his fortune. It’s not the best shareholder base, it’s not the best management team and insider base, but they own 65% of it.

Between 2012 and 2019, Altisource made like $800M in operating income and bought back 1/3 of the company. It’s obvious now that spending those profits on buybacks was stupid, but one thing is clear: this is a business that has the capability to make money. I think a lot of the negativity just comes from the fact that their operating environment has been bad.

I fully acknowledge the shady insiders (some people call Bill Erbey a criminal, Kamala Harris personally persecuted him) - but they’ve supported the company. While Bill Erbey has openly called for the liquidation of Front Door Residential, he hasn’t made similar comments about ASPS. The second largest shareholder, Deer Park Road Management, gave ASPS a credit line in 2021 (which I think is currently non utilized, and does expire).

The management team isn’t heavily invested, but the shares owned by the CEO are certainly nothing to sneeze at. Regardless, my point is this - in a Chapter 11, I don’t think these guys get anything. If dilution happens, the insiders are diluting themselves. William Erbey who may have been the most hated man in America at one point, is now 73 years old, but he seems to still be actively investing, and I am going to speculate that he would like to make money on Altisource if he can.

My assessment of the situation is pretty simple: Altisource will either cease to exist and any investment in the company is worthless, or it will be supported (management says Q4 23 or Q1 24) by revenue increases and shareholders, and the maturity profile on the debt will be extended.

I don’t know this for a fact, but I don’t think the company’s shareholders have zero options. I think the Pointillist sale proved that even their non core business units have some unexpected value, and Altisource has a number of other business units it may be able sell off. The Pointillist sale proved that Altisource couldn’t be judged just on its negative book value. I do think it is interesting that Guggenheim (the company that tried to market the origination business for sale) is running the debt restructuring.

The worst case scenario

Chapter 11 bankruptcy. The shareholders have no options. There are no buyers for any of the other business units. Existing common stock is worthless. This will be the outcome if the existing insiders and management team give up on the company.

Other smart people think this business is a zero. The shares could trade ever lower on negative sentiment - right up to the day a change in the debt structure (i.e. maturities are pushed back) is announced, or down to zero on the day they declare bankruptcy. The bears could be right, and I could be an idiot who has no edge here and is out of his depth. But I see what I commonly see in shipping, mining, refining, and other cyclical sectors: a business in a bad current operating environment being mistaken for a bad business. I think of coal companies in 2019 and refineries in 2020. I think of tankers in 2021. Some businesses came within months of bankruptcy before an improved operating environment saved them. That could be what it all comes down to with Altisource.

Will foreclosures increase?

As I’ve already shown, foreclosure activity dramatically increased in 2022 vs 2021, and that the CEO stated on the Q3 conference call that revenue will not be realized by Altisource until Q4 at the earliest. These are objective facts. Will foreclosures increase from here? Let us again examine the facts.

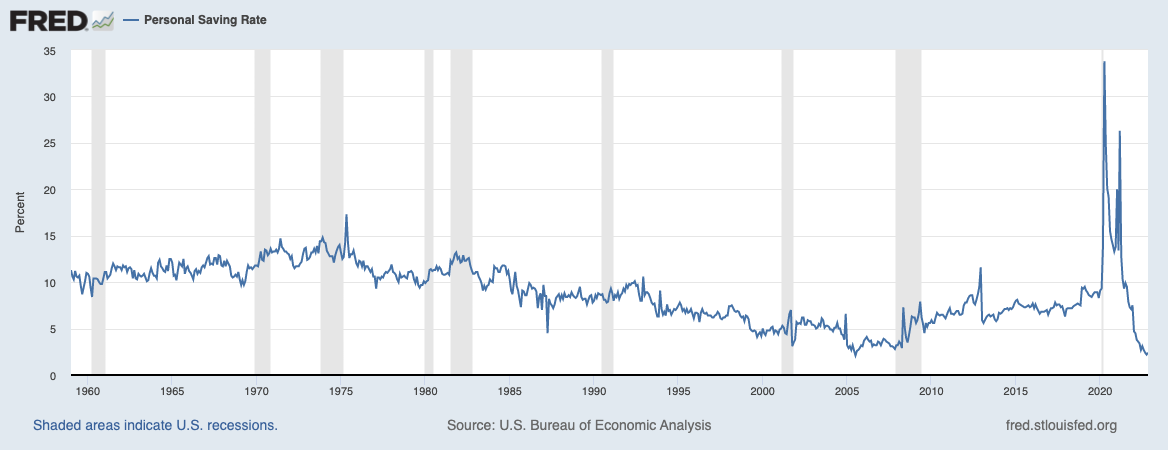

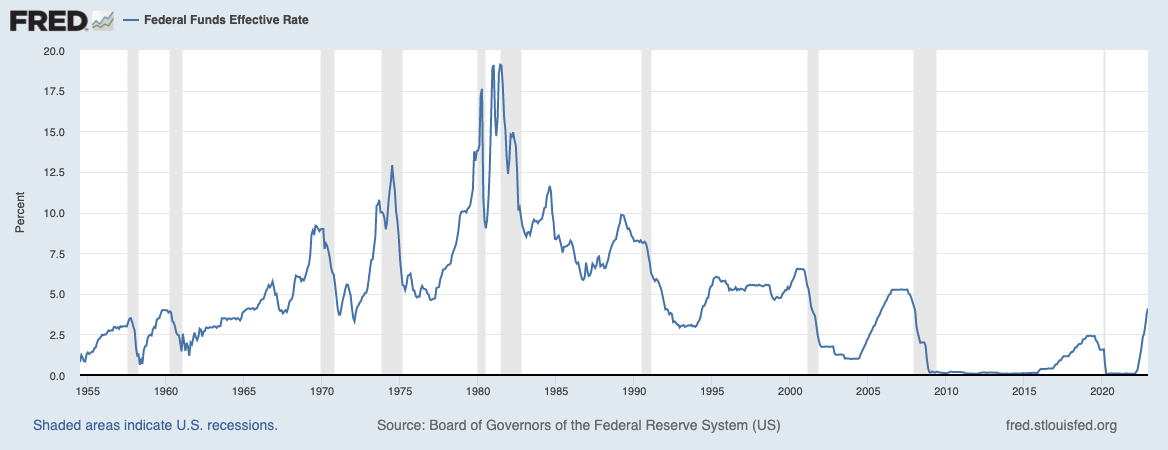

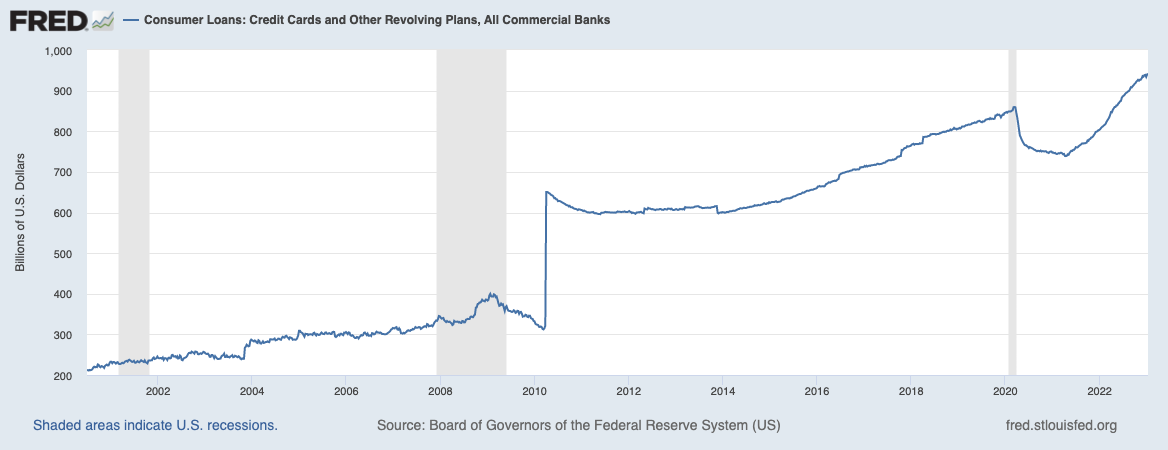

The narrative here is pretty easy to follow: interest rates are rising, savings are down, and consumers owe more on credit card balances. Subprime auto delinquencies are also mooning.

Am I saying that we have another 2008 coming? No. Not at all. I’m saying that it’s unlikely that foreclosures stay at a cyclical low, and if ASPS can simply manage to push back its maturities long enough to see a better operating environment, they can generate more cash in a year than they trade for today. I’m long with an ~$7 cost basis, but this is a risky name - a gamble - and one you should be comfortable with the possibility of losing 100% on before you buy a single share.

Calvin's thoughts is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.