AOI Q4 Recap - Big Oil Find, Disappointing Hedging and Dividend

An oil find of truly gargantuan proportions and a very cheap stock is being overshadowed by poor short term perception of management decisions

Several months ago, some members of fintwit had suggested that because Africa Oil delayed announcing an expected shareholder return policy, it meant that there would be no dividend and no buybacks. I suggested waiting till earnings to find out, and that the very cheap FCF multiple the company was trading at meant a big dividend was at least possible

Reality was somewhere in between, of course. The yield on AOI’s dividend at today’s share price ($1.77) is 2.8% - certainly nothing to get excited about and much lower than inflation. Even more disappointing, the company has hedged most of its cargoes for the next year at just under $80/barrel, meaning they are missing out on explosive upside. However, to say investors are getting no exposure to more upside is misleading. The reality is that while the base dividend is $25M/year, the cash flow per year was estimated at $300-400M, while the market cap at time of writing is ~$840M. Management stressed that this is a base regular dividend policy rather than the only dividend which will ever be issued. Of course, being long AOI, I would certainly prefer a larger dividend as well.

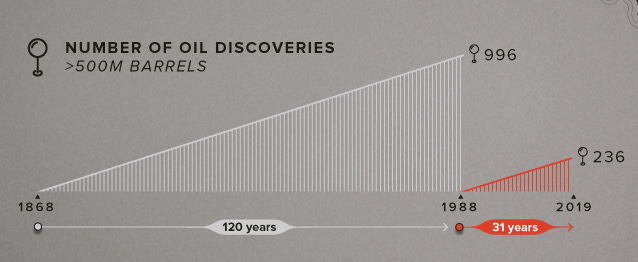

These two points have overshadowed a much more significant development for the company - a development that at the time of announcement caused shares to surge 35% over a few days. The company owns over 6% of one of the largest oil finds in the past 20 years. To put the number in perspective, since 1988, there have been only 236 discoveries estimated at over 500M barrels. The VENUS-1 find off the coast of Namibia is estimated to be near 3 billion barrels.

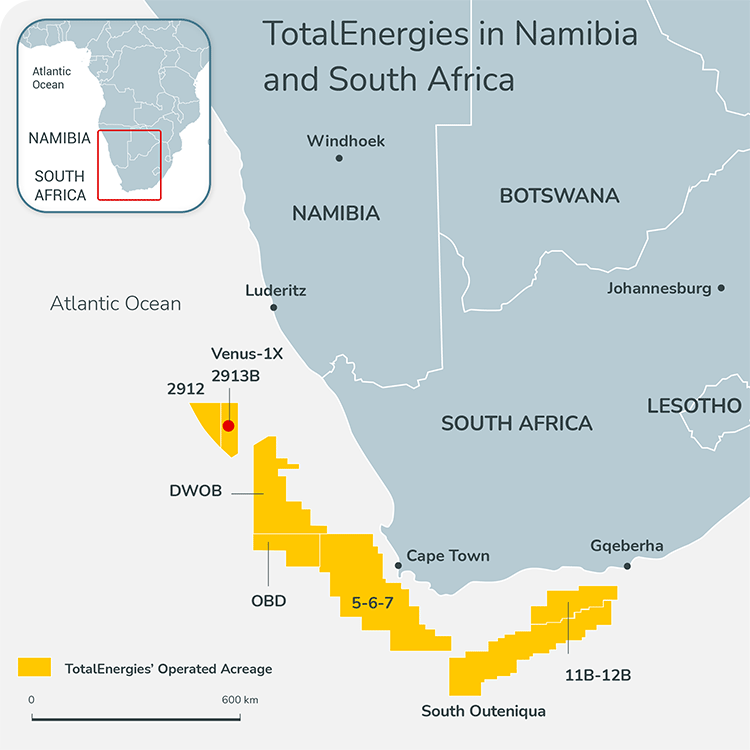

Even better, the find is majority owned by one of the most capable and well capitalized energy companies on earth, and is easily retrievable in a friendly jurisdiction, meaning it’s only a matter of time till the project happens.

To put some napkin math to this, assuming a profit of $20/barrel (and most of the other projects AOI is involved in have an opex/barrel of well under $10), and assuming half of the oil actually gets recovered, we can expect AOI to generate something like $1.8B in net profit from the project. If we use less conservative assumptions and assume something like an $100/barrel profit on the full 3B barrels, AOI could make something more in the realm of $18 billion dollars. This is a company that trades at just over $800M today. In other words, regardless of your thoughts on the company’s dividend and hedging, it’s good to remember that their existing assets are profitable, a shareholder return policy has been put in place, you are receiving a base dividend, and the exposure to further long term upside in the price of oil via the VENUS-1 field (one of many AOI interests), is 100% an asymmetric opportunity.

I am long AOI, and have been long since well under $1. I see a much higher share price from here as a base case using the napkin math above, with life changing returns being possible. There aren’t many opportunities to own an already profitable company with low decline rates and easily recoverable energy in a friendly oil and gas jurisdiction these days, especially one piggy backing off a major like Total. I’m staying long.