Braskem: new car smell

We've been following the Braskem saga for several years now - from the previous buyout attempts and the environmental issues, to the panic and chaos as the company became distressed, to eventually a number of wins that are starting to derisk the company for a recovery. To review the challenges:

- Multi billion dollar environmental obligations due to Alagoas disaster (salt mine collapse)

- Deteriorating debt maturities (credit rating downgrades and discontinued coverage)

- A bankrupt primary shareholder with past links to corruption and scandals

- Continued operating losses

- Failed acquisitions by multiple suitors, from Middle Eastern conglomerates, to Brazilian banks and business men, to Apollo

- Braskem Idesa (Mexican subsidiary) troubles

Since I first announced I was long at an $8 cost basis, the name has fallen more than 50% from those levels, hitting a low of nearly $2 per share in October 2025. I have traded in and out from the name, I have carried and realized losses. And yet unlike another one of my bad calls - Vertex Energy for instance, which I pulled out of when I knew the situation was hopeless - I have not given up. My thesis has always been this - Braskem has traded at much higher levels in the past - and those prices were justified by the earnings and dividend payouts of the company. Even since covid, the company has paid out approximately its current share price in dividends.

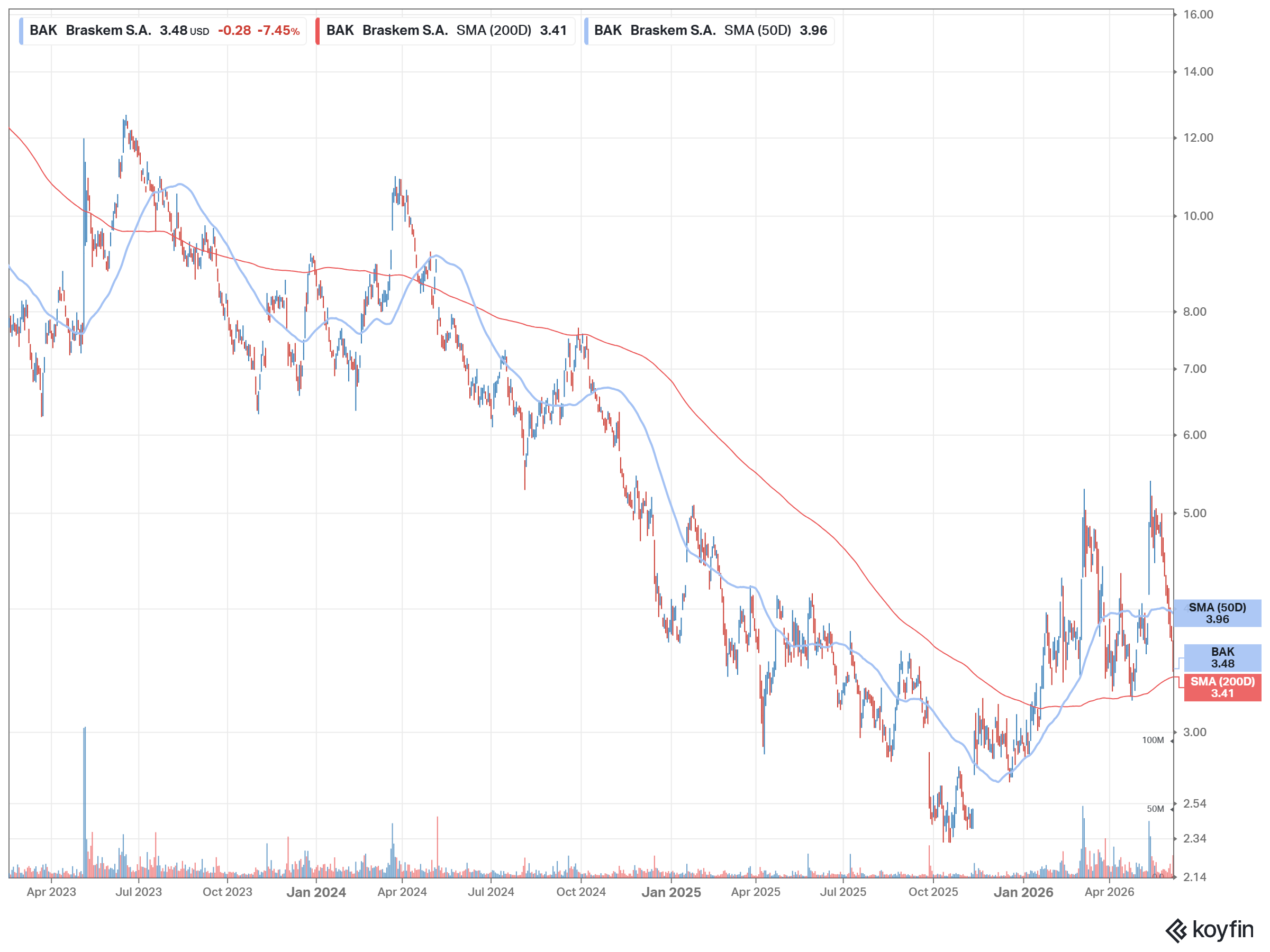

The technicals for the stock have markedly changed, representing what looks more like a hard bottom, and yet fundamentally, we still need to see some improvements in order for Braskem to survive without dilution or bankruptcy. This is very much a special situation now. I want to review the positive changes that have kept me interested in the company, why I think it has a "new car smell", and what might lead me to abandon the idea completely.

First, a summation of the positives:

- The Alagoas environmental disaster was settled with both the city and the state

- Real concessions were given by the federal government of Brazil to help the company survive, including anti dumping provisions to fight Chinese competition, with even stronger provisions passed in April

- Tax benefits were given to the company in the form of REIQ and PRESIQ regimes

- Novonor, the bankrupt former Odebrecht, was pushed out of the company in a deal between its creditors and IG4 Capital

- Last week, Braskem announced it will present a plan for restructuring its capital structure to creditors, a plan which proposes grace periods, term extensions, and lower coupon payments

- The Strait of Hormuz closure has materially improved petrochemical spreads in the Americas, pushing them to some of the best levels in the past decade. This has been concentrated in Q2. Numbers in Q1 do not yet reflect improvements from this.

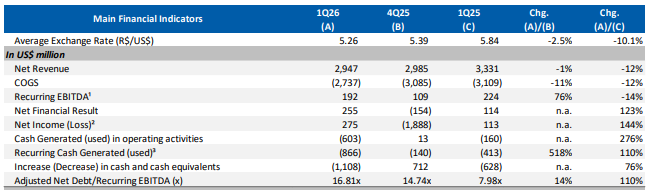

To summarize the position that the company is in financially, we can see in Q1 (Net Financial Result, Net Income) that things have improved over the last quarter and previous year. However, we can see an enormous cash burn and debt to EBITDA ratios blowing out.

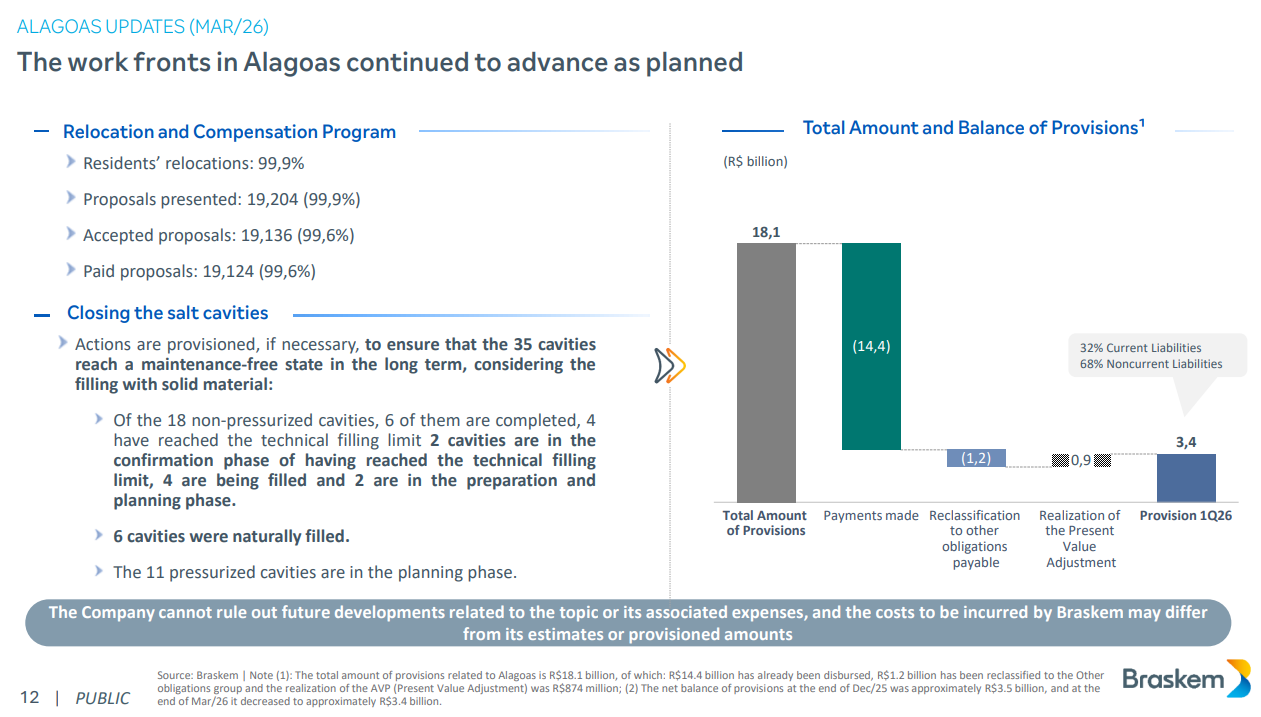

On the Alagoas front, which has sucked billions out of the company, we can see that things have stabilized.

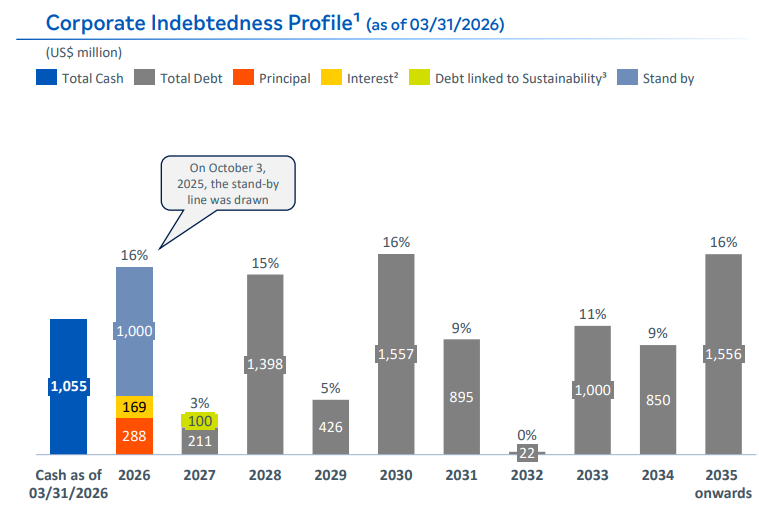

But on the debt maturity side, the company barely had enough cash remaining at the end of Q1 to cover the stand by credit line maturing this year which they drew last year. The company now must generate positive cash flow - or restructure its debt profile - in order to survive.

The Middle East conflict has theoretically given a lifeline to Braskem as many Middle Eastern and Asian producers were forced to cut runs or declare force majeure. It's important to remember that IG4, when they agreed to become the controlling shareholder of the company, was not betting on a Hormuz closure. The benefits from tax and tariff changes are expected to generate somewhere in the range of $500M annually for Braskem. To review a bit who IG4 Capital is:

IG4 Capital is specialized in investing in special situations and market dislocations

We are focused on generating performance through value creation and business transformation

IG4 Capital’s private equity investment approach seeks to mitigate key risks before tapping into investment opportunities using restructurings, conversions of debt into equity and promoting change of control while partnering with banks and other creditors. IG4's industry experts and operating partners enhance the capacity of the investment team to source opportunities and transform companies.

Here's what Rio Times said about IG4 and the transaction:

For IG4 — a private equity firm specialized in distressed assets — the transaction is its largest-ever single deployment and a test of whether a Brazilian manager can execute an operational turnaround at petrochemical scale. IG4 is known in the market for handling complex court-supervised situations, but Braskem’s combination of cyclical petrochemical compression, environmental liability, and currency-mismatched debt is an extreme case.

While IG4 was only established in 2016, we can see that the firm is basically built around exactly this type of transformation. IG4 is trying to save the company. Given the company's AUM of 1B in equity and 3.8B in credit, I think it's fair to say that IG4 - who was able to negotiate an agreement with Novonor's creditors (mainly Brazilian banks) in order to acquire the controlling stake - has more or less full ported on Braskem. Whether or not they will succeed remains to be seen - but someone doing a multi billion dollar all in bet - well, that's not something you see every day. I don't think billions in capital would have gone into a distressed industrial play in Brazil unless they had a plan, and to some level - assurances that things would play out. Many things had to fall into place for us to get here.

Let's break down what IG4 actually did.

They first acquired Novonor's debt from creditors. The banks were bought out by the Shine/IG4 fund which now controls the former Novonor stake. So basically, IG4 replaced Novonor by acquiring their debt, which they had pledged their Braskem shares as collateral to secure. Bank claims convert to equity; the equity channels into the fund; the fund inherits control. Novonor retains a residual 4% stake and gives up its seat at Braskem’s control table.

Novonor is bankrupt, but still tried to cling on to Braskem, which was its last remaining position of any value. A company called NSP was set up to manage some of these obligations, and in 2018, this company issued debentures, essentially unsecured debt, which it defaulted on, through the insruments OSPI12 and OSPI22. Shine/IG4 went out into the secondary market and bought up all of these paper claims which were in judicial recovery, and then delivered them back to Novonor. Effectively, the original holders of the debentures may have lost their shirts, but the claims could still theoretically be forced in court for them to be repaid. IG4 bought these claims, and then gave them back to Novonor, as well as paying off the banks who owned their debt. IG4 basically bought out Novonor's various debt.

Now, the next step given IG4 control is that as a change in control has occurred within the company, a tender offer will be presented to all minority shareholders. Since no cash was exchanged, no monetary exchange will happen - instead the tender offer will be for debentures.

Brazilian Corporate Law (Art. 254-A), Braskem’s bylaws, and CVM rules require Shine I to make a public tender offer for up to all remaining common and preferred shares (including ADRs) on the same terms as the control block transaction. This is a minority protection triggered by the change of control. Shine I has committed to filing it and cannot avoid it (CVM registration approval is even a resolutory condition for the overall deal).

Minority shareholders (including you) can choose freely whether to tender your shares or not. You are not obligated to participate. If you do nothing, you simply keep your Braskem shares (BRKM3/BRKM5/BRKM6 or BAK ADRs) and remain a shareholder under the new control structure (Shine I + Petrobras shared governance).

If you tender, you receive 2 OSPI12 + 1 OSPI22 debentures per Braskem share (same as the control deal). You become an unsecured creditor of NSP/Novonor in judicial recovery. In my view, that puts you at the mercy of Novonor cancelling or purchasing these obligations in the future. In other words, you're getting the same deal Novonor got, but if you accepted the tender, you'd basically be an unsecured creditor in a structure controlled by Novonor, where theoretically you can sell your shares in the secondary market or wait for them to be retired by NSP/Novonor. For each Braskem share tendered (common BRKM3 or preferred BRKM5/BRKM6, including ADRs):

- 2 debentures of the 1st series (ticker: OSPI12)

- 1 debenture of the 2nd series (ticker: OSPI22)

Theoretically, these have a market value of around 3 BRL each, but there is no trading volume or liquity to realize a sale, and realizing a value in another ways involves NSP buying back debentures or some sort of court ordered settlement. Not very attractive, and only someone very close to this action, with a very deep understanding of the mechanisms would likely be involved here.

Basically, there will be no cash buyout offer. Unlike many speculated, however, you will not be forced out of the capital structure. You will be a minority shareholder in a structure controlled by IG4 and Petrobras. You have no vote, but you have the same economic incentives that IG4 and Petrobras do. The banks are out. Novonor is out. Novonor's unsecured creditors are mostly out (there may be some residual debenture holders). Petrobras now has the board chair seat and is said to be increasing involvement in Braskem. IG4 will be replacing some of the executive team, and essentially have day to day control of the company, with their main barometer for success being a net debt-to-Ebitda ratio to 2.5 times or less for three consecutive quarters. The upside for IG4/Shine, Petrobras, and minorities comes from equity upside and dividends.

Will IG4 and Petrobras take things this far only to now abandon the recovery effort and let the company fall into bankruptcy? I very much doubt it. I believe that the recovery is here, and while some risks remain - it's time to hold on and enjoy the ride. I believe that the recovery for the company was strategized and envisioned before the Hormuz crisis increased petchem margins. I think extended Hormuz difficulties is an unexpected tailwind for Braskem, and I am surprised that the equity price is not higher now. I increased my position during yesterday's selling.