Brazilian Steel Tariffs - Two Companies in Focus

A look at CSN (SID) - A Brazilian industrials conglomerate with heavy steel exposure, and Gerdau, the largest producer of long steel in the Americas

A wave of anti dumping laws have been adopted across Latin America as Chile, Brazil, Mexico, and Colombia all fight to protect domestic steel makers from Chinese competition. All of the aforementioned except Colombia have already adopted strong new anti dumping measures against Chinese competitors. Chinese steel has been flooding American markets as the Chinese real estate slump has forced Chinese steelmakers to market their products more aggressively overseas.

Companies like Gerdau and CSN have been seeking assistance on what they call predatory imports from China, and a last week, the Brazilian Ministry of Industry gave them what they were asking for - more than doubling tariffs (from 11% to 25%) on any products that are being “dumped” on the Brazilian market - technically defined as any product which saw imports increase by more than 30% from the 2020-2022 average.

Brazilian steel makers had a muted reaction to news that should have been positive (there was a small pop right before the announcement of new tariffs, which was promptly sold).

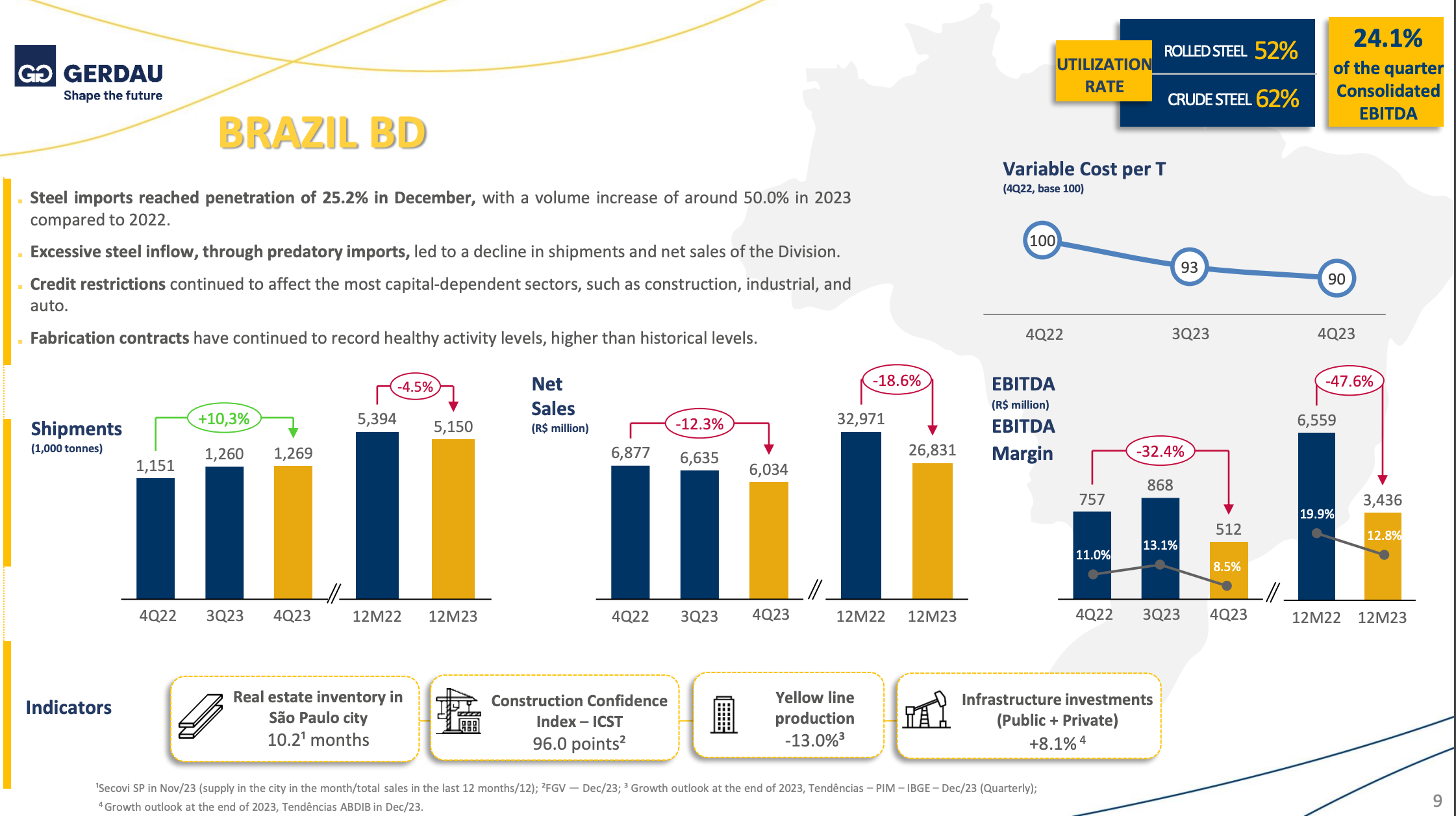

Looking at recent earnings presentations from Gerdau and CSN, we can see the impact that Chinese dumping has had on domestic sales for Brazilian steelmakers. Gerdau pulls no punches and highlights a volume increase of imports of around 50% in 2023 vs 2022.

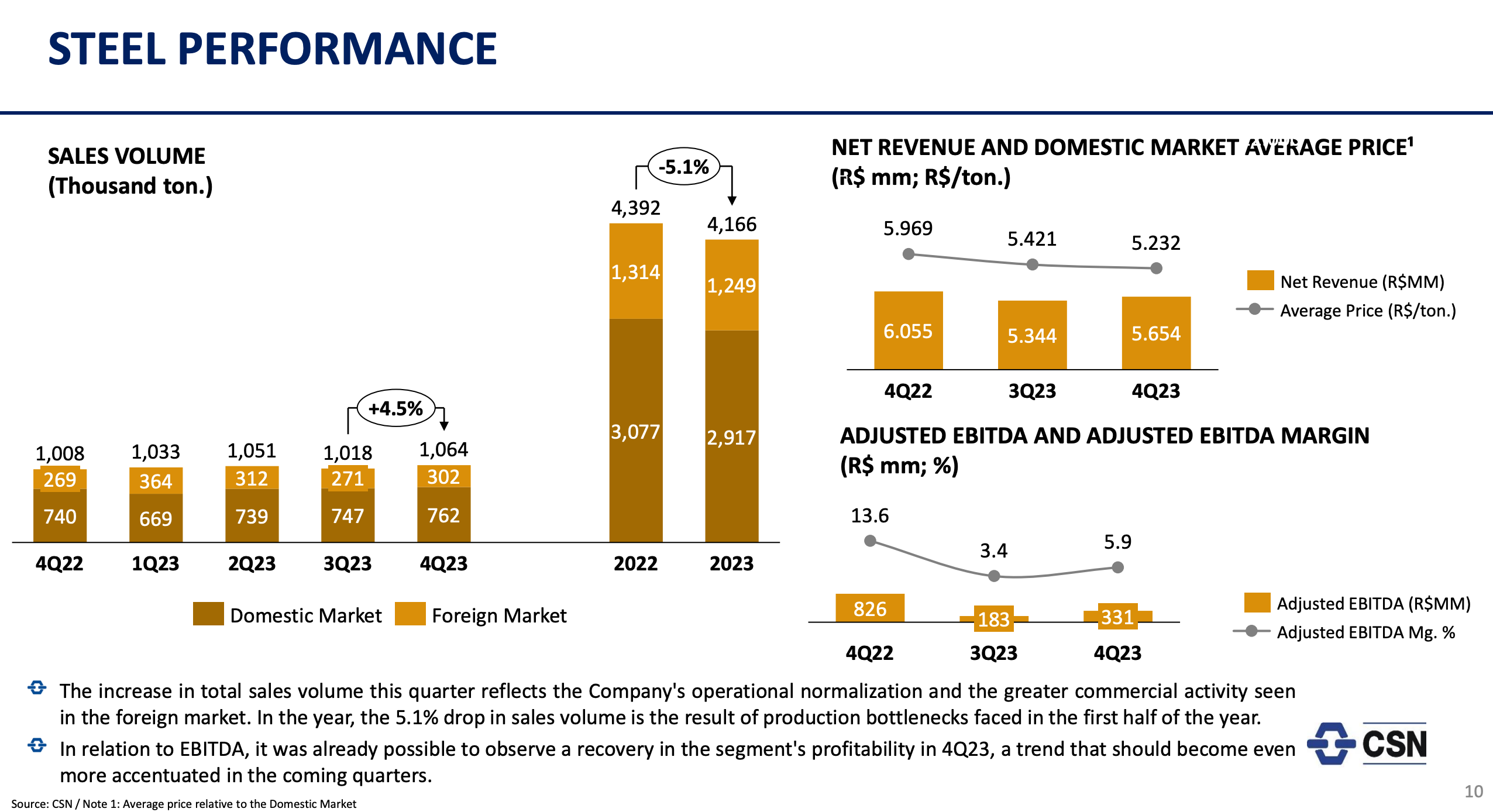

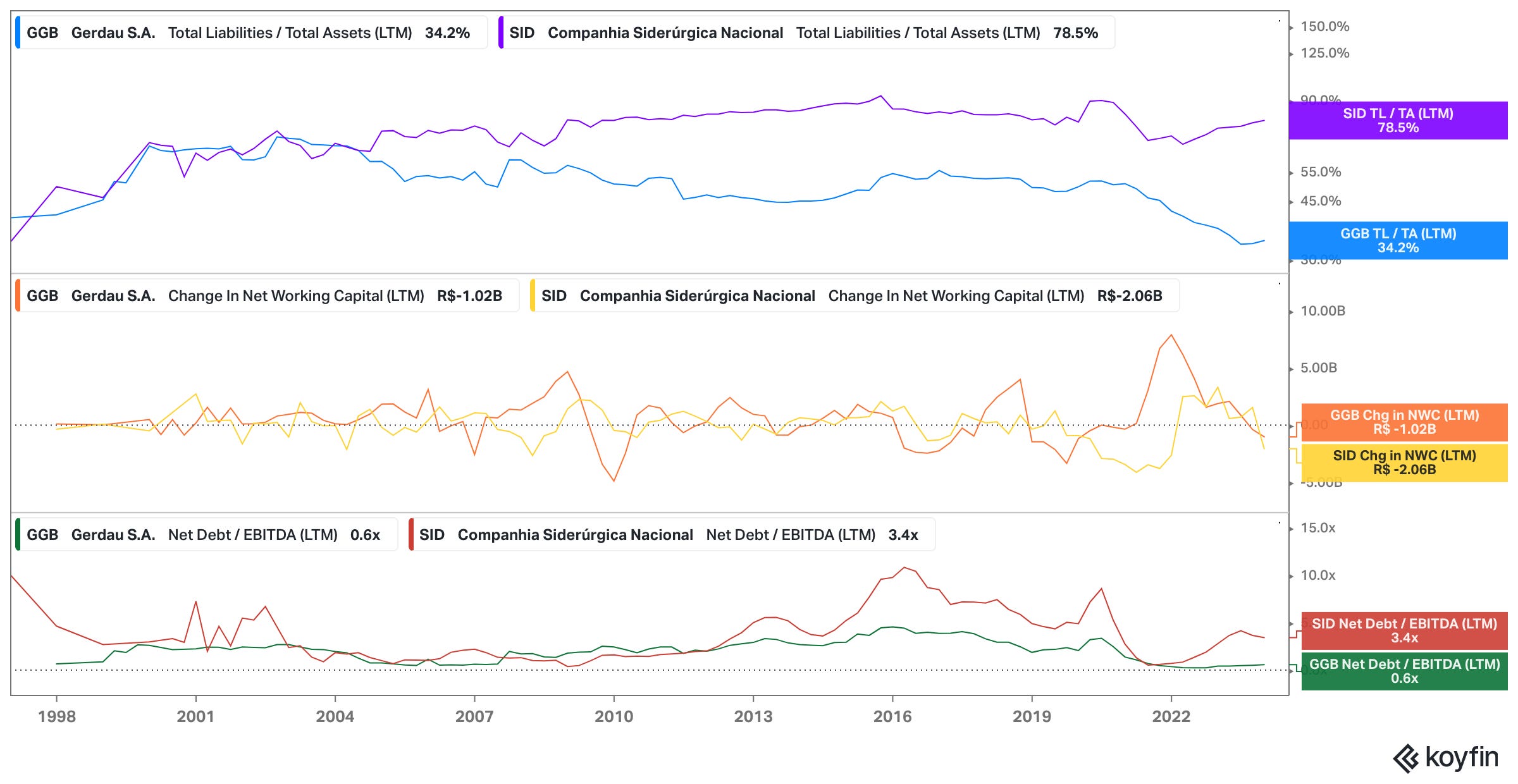

CSN has held up better than Gerdau, but both have seen their sales volumes decrease. In the case of both companies, we can see that working capital has deteriorated recently. CSN has taken on leverage versus recent years, though it remains well below Debt/EBITDA levels seen in the 2010s. CSN has run with more leverage than GGB for decades. Working capital changes for both companies have been historically significant, showing recession level deteriorations.

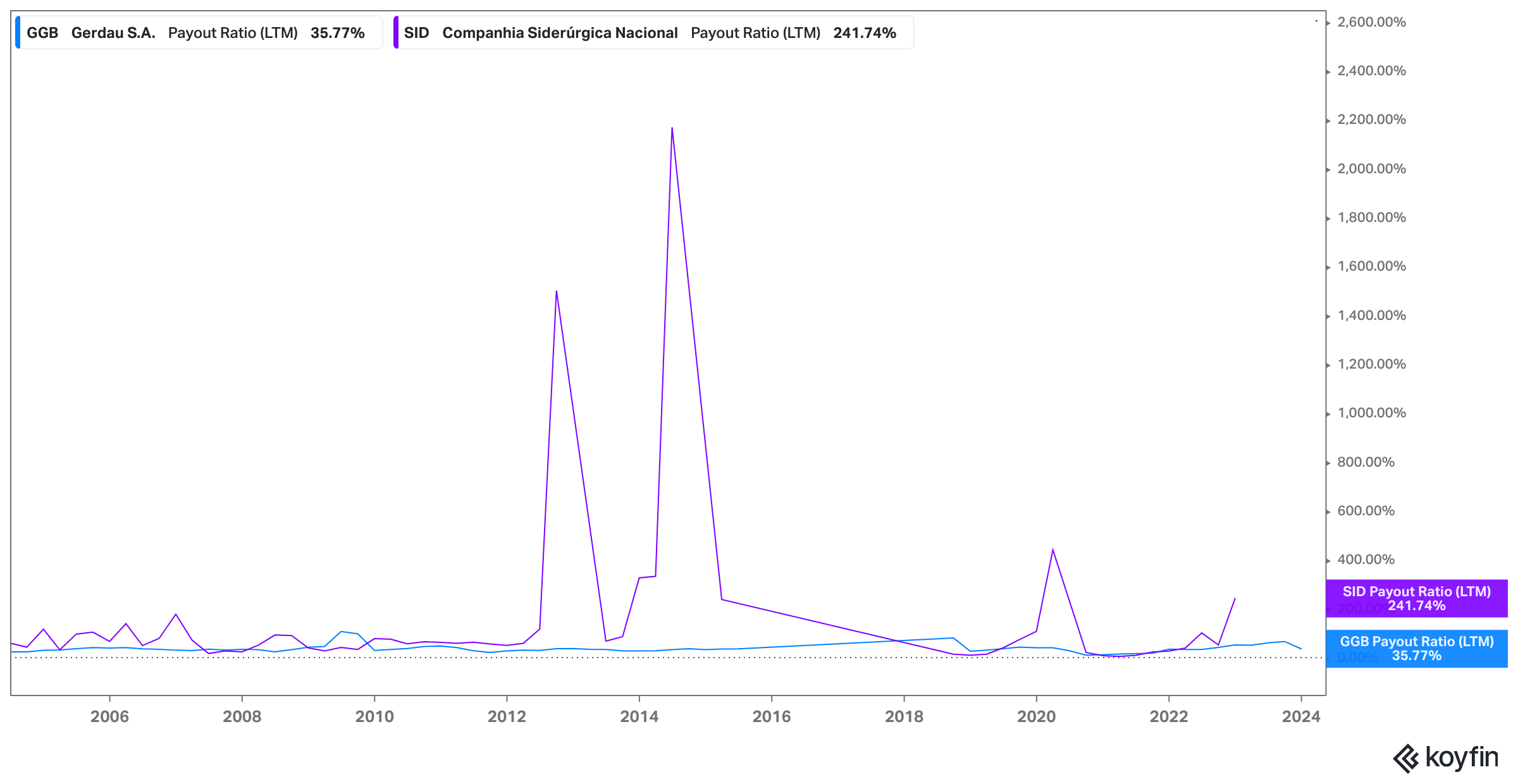

From a dividend perspective, both companies have historically paid quite handsome dividends. I fear, however, that CSN may be a bit too leveraged.

This is, however, a historical norm for CSN, which has historically used its balance sheet and even taken on debt to keep the dividends rolling. Gerdau has historically been far more conservative.

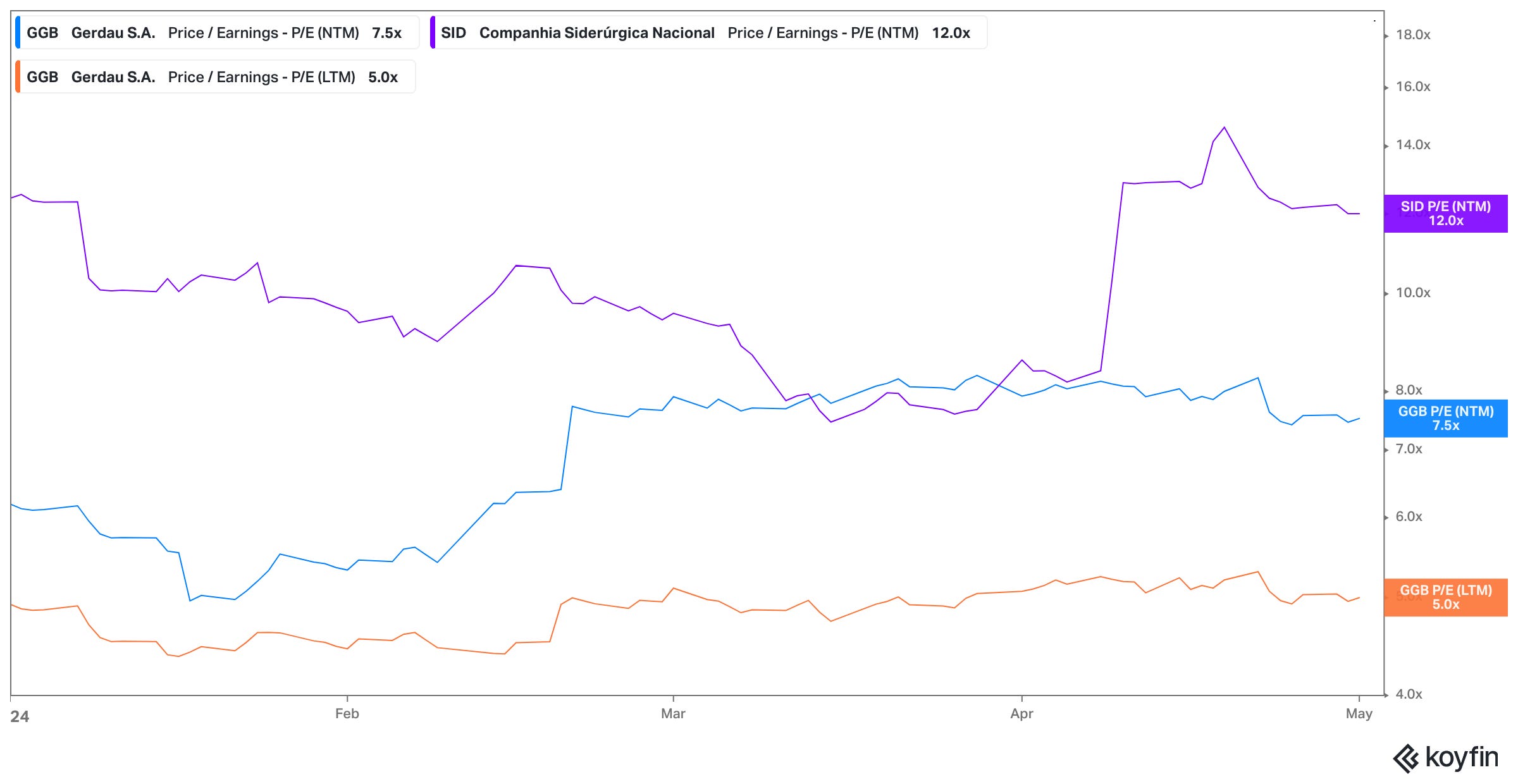

On the earnings estimates side, estimates haven’t really moved after the anti dump rule moves - NTM estimates are about the same. If the measures indeed have a positive impact on the domestic market, I would expect earnings estimates to improve.

Conclusion

Anti dumping laws should help protect the margins of domestic steel makers in Brazil, who have been flooded with fierce competition from the Chinese. CSN and Gerdau are two options you might consider playing if you want to take. Both names are down double digits YTD (30% and 12% respectively) and have historically paid very strong dividends.

Among the two, CSN (SID) has higher leverage and carries more risk, but could deliver much better returns if Latin American countries can fend off Chinese competitors using tariffs. Gerdau runs a much more conservative balance sheet and should offer a strong all weather yield. I would consider Gerdau a portfolio bread and butter name, while CSN offers much more potential for appreciation in a favorable pricing environment for their products.