Demand destruction! Oil stocks crashing! Is it like 2008?

A look at Canadian firm Transglobe Energy, how it fared in the 2008 financial crisis and recession, and how it compares to today

After a spectacular start to the year, energy stocks are crashing. As I am more than 50% allocated to energy stocks (most of the rest to shipping and defense), as a sanity check I decided to go back and peruse reports from previous years, especially 2008.

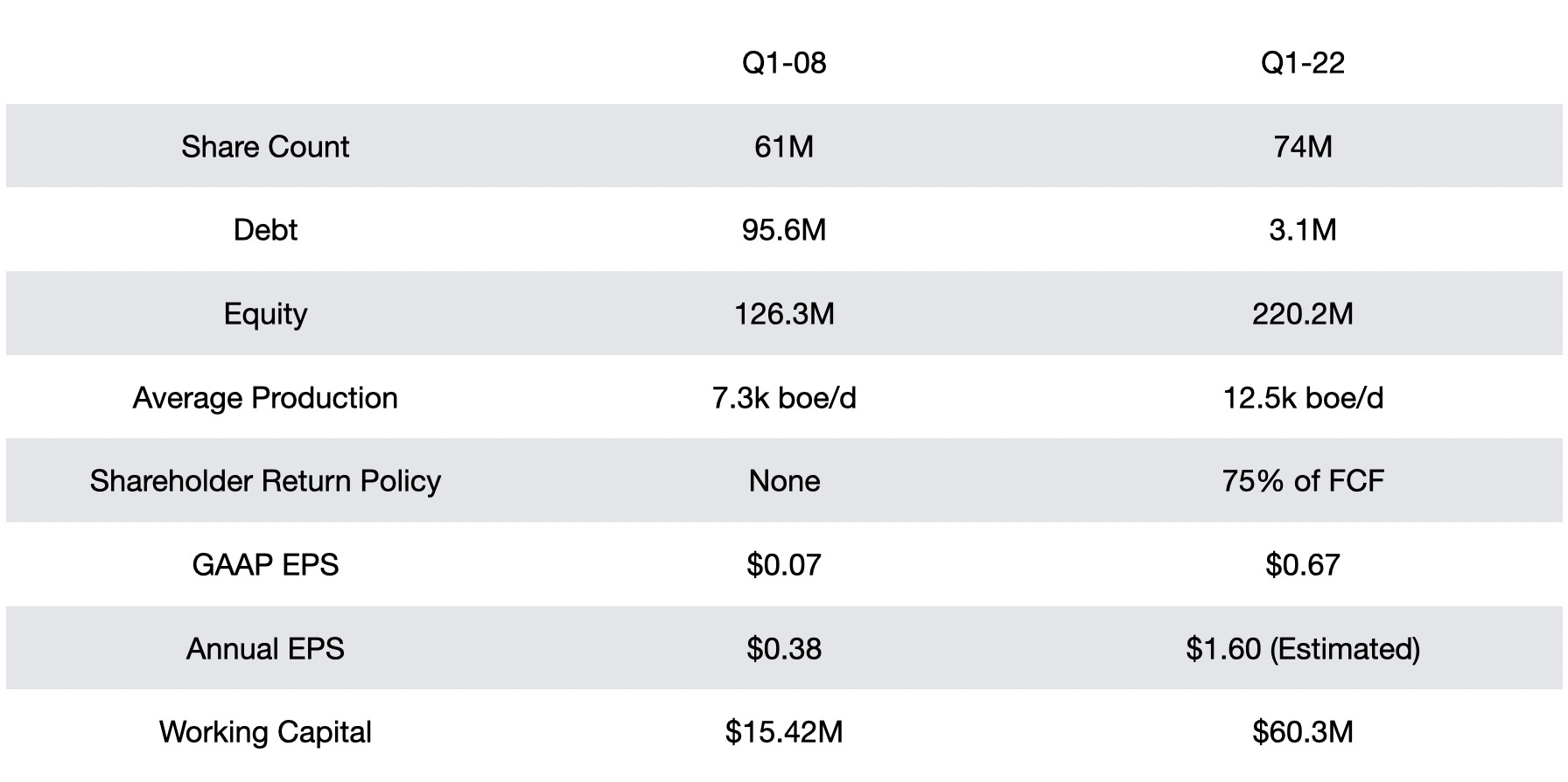

To start with “what was similar”, in 2008 the stock topped out at around $5.25/share. By October, they bottomed around $1.50/share. On June 8th 2022, shares topped at around $5.30/share. And this is pretty much where the similarities end. First, let’s do some high level comps to show what TGA looked like at the end of Q1-08 vs Q1-22:

One look at this chart should make something very clear. When the recession started in 2008, TGA was at a very different point. They were loaded with debt, had no return policy, very little working capital, and over the next few years, would dilute shareholders and pay no dividends.

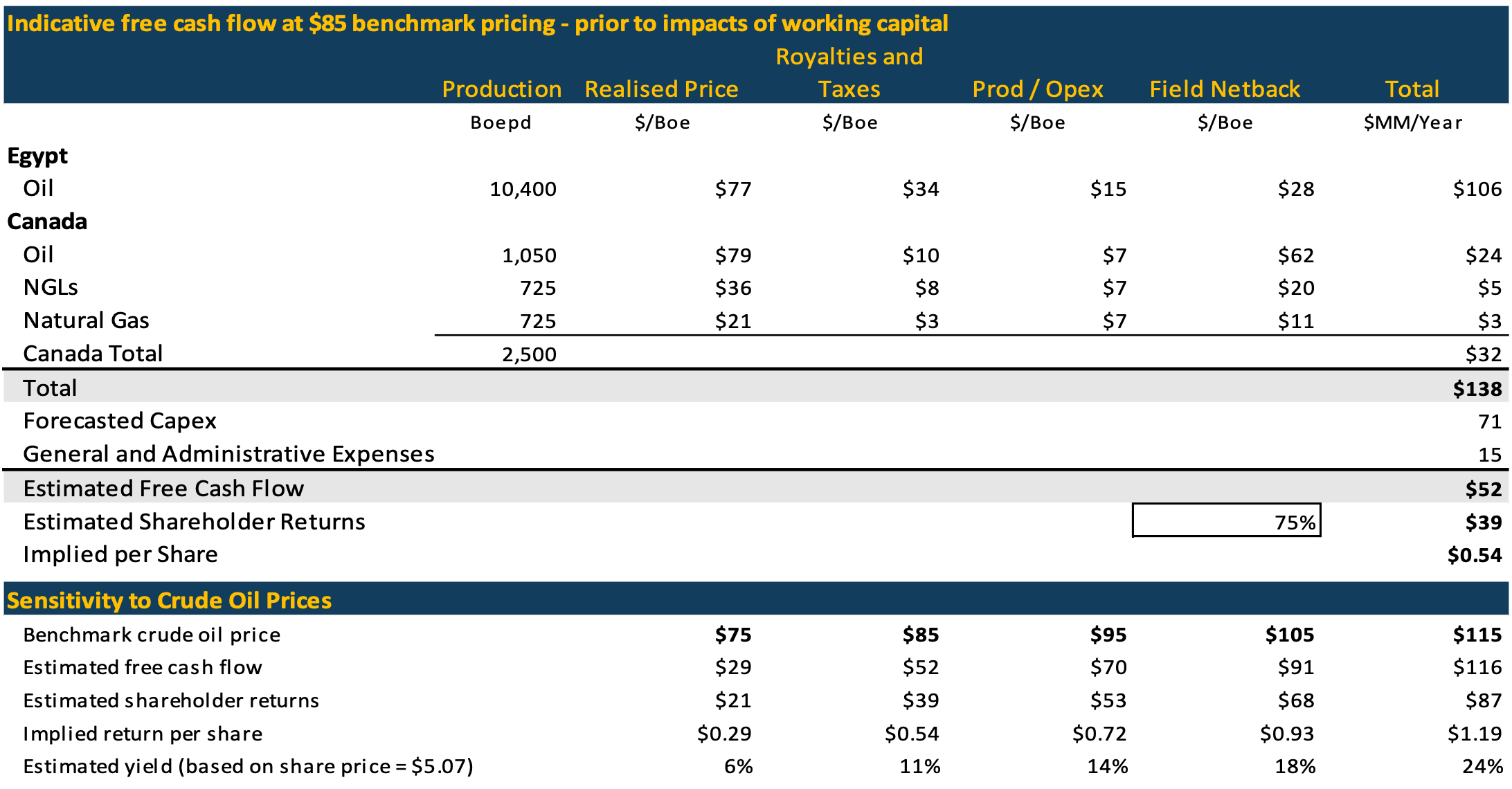

Looking at today’s situation, the company has instituted a very generous return policy of 75% of FCF going to shareholder returns, with well covered capex:

With Q1 and Q2 already a done deal, if 2H 2022 were to average ~$90/bbl Brent, we could expect more than $1 in shareholder returns, implying an ~29% yield on today’s closing price.

Now look we can talk about demand destruction till we’re blue in the face, but that doesn’t change the fact that this company is debt free, funding capex from operations, and more than half way to returning $1/share this year. Were the stock to trade down to its 2008 low of ~$1.50, it would trade < 1x GAAP earnings and close to an 80% FCF yield. Were that to happen with oil still anywhere close to $100/bbl, I’d be tapping credit cards to buy more.

I’m already long TGA at around a $4 cost basis. I thought I was getting a great deal at a 25% yield. This post was mainly just as a sanity check for myself to answer the question: is it like 2008? The definitive answer seems to be no. I can’t speak for all oil companies, but at least TGA is in a completely different point in its capex cycle and outlook. In 2008 it was risky. Today working capital is greater than an entire quarter’s revenue.

As far as the oil market outlook, the US is at the lowest SPR level since 1985. Commercial inventories around the world are low. Refining cracks are high, and VLCC rates are low. OPEC has been missing quotas every quarter, Libya and Ecuador have both declared force majeure, there’s a major war in eastern Europe, and China just lifted its crude import quota by ~50% YoY. It’s not 2008, not economically, and not for Transglobe Energy. Were the stock to trade down, I would continue to add more. Most of the rest of the market would need to trade down 75% or more from here to offer these kinds of returns.

Will the price go down in the short term? Who knows? I’ll be buying either way.

Calvin's thoughts is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.