Empire building is hard

A deep dive on Vertex Energy, with a focus on the human side of the story

Many of my subscribers likely feel a bit sick when I mention Vertex Energy, which for a while was the best performing stock in the world, and has now fallen back to earth. Indeed, it’s been a rough road over the past year. In this post I’m going to discuss how I discovered the names, why I’ve continued to follow it, and what my best guess is on the chances it works out. Let’s dive in.

Vertex Energy

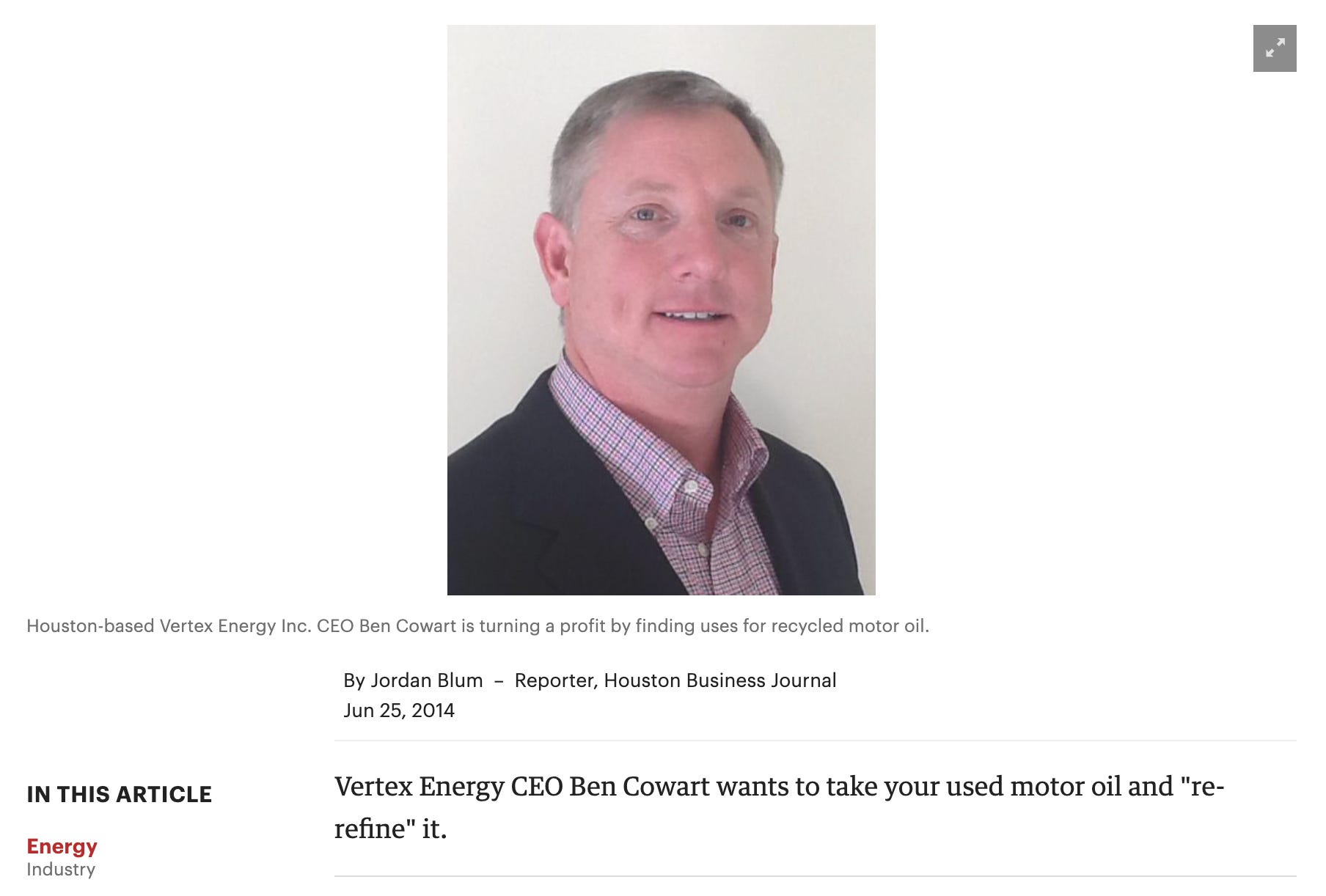

I began following what is now known as a single asset refining play back in 2019 when they had a hodgepodge of blending and re refining operations. In 2019, I was obsessed with the marine fuel regulation changes that would come into play in 2020, which promised to shake up the oil tanker industry, and led countless ship owners to install devices called “scrubbers” on their ship, which, to make a long story short, dump exhaust into the ocean instead of the air. Vertex was a small company that basically “started out of a garage” with a dream to reuse waste oil and turn it back into something useful.

Cowart literally started as a 16 year old working for his brother in the used oil collection and recycling business in Alabama.

There isn’t much on the internet from those early days, and Cowart doesn’t list education or any other jobs anywhere.

There’s not a lot on the internet about happened between 2000 when Cowart moved to Houston to go into business for himself, 2009 when Vertex became a public company through a merger, and 2014 when that company was spending forty million dollars to acquire a larger re refining business. I imagine, though, that it was a lot of tinkering in the garage, figuring stuff out, and hard work filling the gaps.

Just one of the assets Vertex acquired from Omega Holdings in 2014 would sell less than a decade later for nearly three times what Vertex paid for the entire business. One of those assets is still a major part of the Vertex portfolio.

In 2014, Vertex was producing around 80 million gallons of oil products annually. It now produces that amount in a few weeks.

When Vertex Energy first came onto my radar in 2019, it was trading at around $1 per share and profitably operating several small facilities. Since the company went public in 2009, it experienced a big spike on the acquisition of the assets, followed by a long walk in the wilderness. Things were just starting to look up for them again in 2019 after landing a big marine fuel deal when covid hit.

The company managed to survive, and then one day a press release popped out that Vertex had agreed to acquire a refinery from Shell that would increase the scale of their business by around 20x. This is when the knowledge that most people have of the company starts.

I hope by now you can realize why I tend to defend these guys despite the volatile ride. What Benjamin Cowart has achieved over the past 20 years is nothing short of amazing. A literal kid from Alabama working in his brother’s waste stream business has grown his company to a multi billion dollar business. He didn’t have any pedigree, he never worked for anybody but family. He just kept building his own little empire, for decades, rolling with the punches.

Now Cowart is in the big leagues, running a real refinery, screwing up hedging to piss away what would have been a Godsend of a quarter, failing to disclose said screw up in a timely enough manner, entering into egregious agreements with blood sucking banks and product marketers that put his company over a barrel, deciding to dilute himself (as the largest shareholder) to pay for mistakes and bad market timing, and having the whole world ask who is this idiot that doesn’t know how to run a refinery.

Gentlemen, on a scale of 0 being someone who has accomplished nothing at all in the past 20 years, and 100 being Bill Gates, Jeff Bezos, Warren Buffet, or Carlos Slim, Benjamin Cowart has to be ranking in the high 80s. Cut the man some slack. Extreme success means sometimes taking loans at high interest rates, sometimes signing agreements with counter parties you know are screwing you, sometimes diluting the crap out of yourself to make sure you don’t go bankrupt later, and needing to hear the rest of the world call you an idiot. When Ben Cowart moved to Houston, I’ll bet you he was the only person in the world who believed in what he was doing - and on some days that’s probably true even now.

Most of the expert commentators on Twitter who are obsessed with what warts the company has - what mistakes they made in taking over an asset that exponentially increased the scale of their business - just aren’t seeing the big picture here. There just aren’t many underdog stories in the world that are this good. They went from $50M in quarterly revenue to $1B in quarterly revenue in a year. You try pulling that off without a hitch.

With my “cut the guy some slack” out of the way, let’s get to what you all really care about - is Vertex a good investment? The best answer I can come up with is maybe. I personally found getting paid 30% to sell puts on a good old southern boy that spent the past two decades beating the odds with grease on his hands compelling.

The Current Vertex Challenge

We have a Marhelm member, known both in Marhelm and on Twitter as argonbeam. He’s a surgeon and enthusiast in idiosyncratic gulf coast oil related companies like OSG and Vertex. Here’s what he had to say:

They need to show good RD reliability with the low-CI feedstocks discussed in the call - distiller’s corn oil/DCO and tallow. Make sure can run RD at nameplate while not poisoning catalyst. Get CARB LCSF certs for those pathways. Then manage feedstock inventory so as not to lose money to Macquarie there. They also lose a bit to the middleman providing their low-CI feedstock vs VLO/DAR for instance, who has their own pretreatment units. Once handled, up both their catalytic reformer (more hydrogen) while also upping hydrogen supply not related to reformer. 14 kbpd is what they rate the RD unti for assuming they can do the other things I mention. CVI and DINO had issues with their units but seem to be figuring it out. Vertex tech team seems to be competent minus destroying a feedstock pump somehow, but these are complex processes and I expect some teething issues. Just need to do it before they potentially get short cash and forced to make tough choices. Regarding petroleum side, they are limited both on crude slate as well as product % due to refinery simplicity. Makes them a marginal refiner compared to other PADD3 people with more sophisticated secondary units that allow greater high-value product extraction from cheaper/heavier/sourer crude slates. All this my two cents, and worth about as much. I invested for the RD and want to see how they do there before throwing in the towel. Hopefully two more quarters to discovery on the RD side.

For those of you who aren’t neurosurgeons or refining experts, I’ll translate in the “crude” terms I’m known for. Vertex is running an older asset that Shell wanted to get rid of. It doesn’t have all the fancy bells and whistles that the newer, bigger refineries do. Vertex doesn’t have the commercial scale that an Exxon or a Shell does. It’s harder for them to buy feedstock and sell inventory. They have some tough agreements with counter parties. On the renewable diesel side, they’re literally turning beef fat into something you can run your truck on, and that’s a bit harder than making salty tweets.

Can the refinery make money? Management thought so. I hope so. Perhaps it was Cowart’s ambition that led to financial models that suggested incredible upside that have since been scrubbed. So I’ll just tell you what’s actually happened. The Mobile refinery made $51M in profit last year. The Mobile refinery has made about $30M YTD. In the 14 months since they acquired the refinery, they’ve put $80M net on their income statement from it (the $63M interest hit from the convertible debt was non cash). This happened while they put $115M into capex for their RD project.

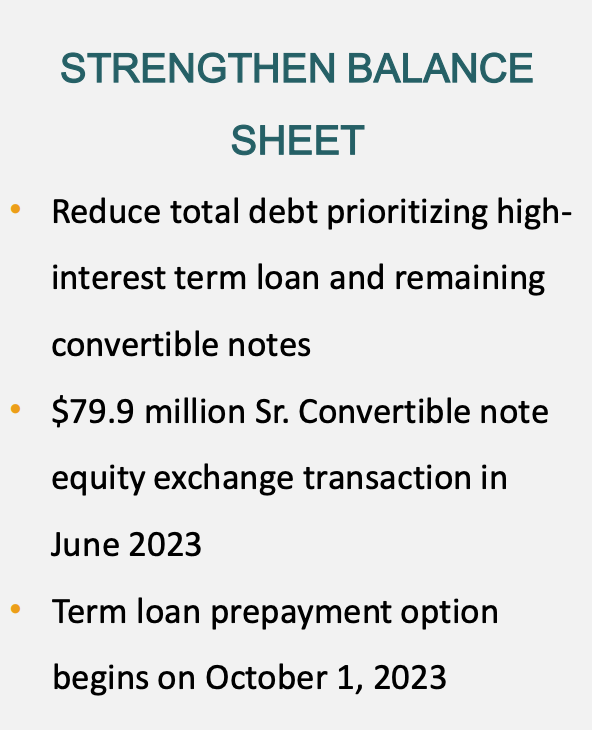

Looking forward, they’ve got a gigantic term loan at an egregious interest rate (15%) maturing in 2025 (the term loan) to pay off. They’ve finished their RD capex and they diluted to get rid of the convertible debt. They can start prepaying their term loan in October.

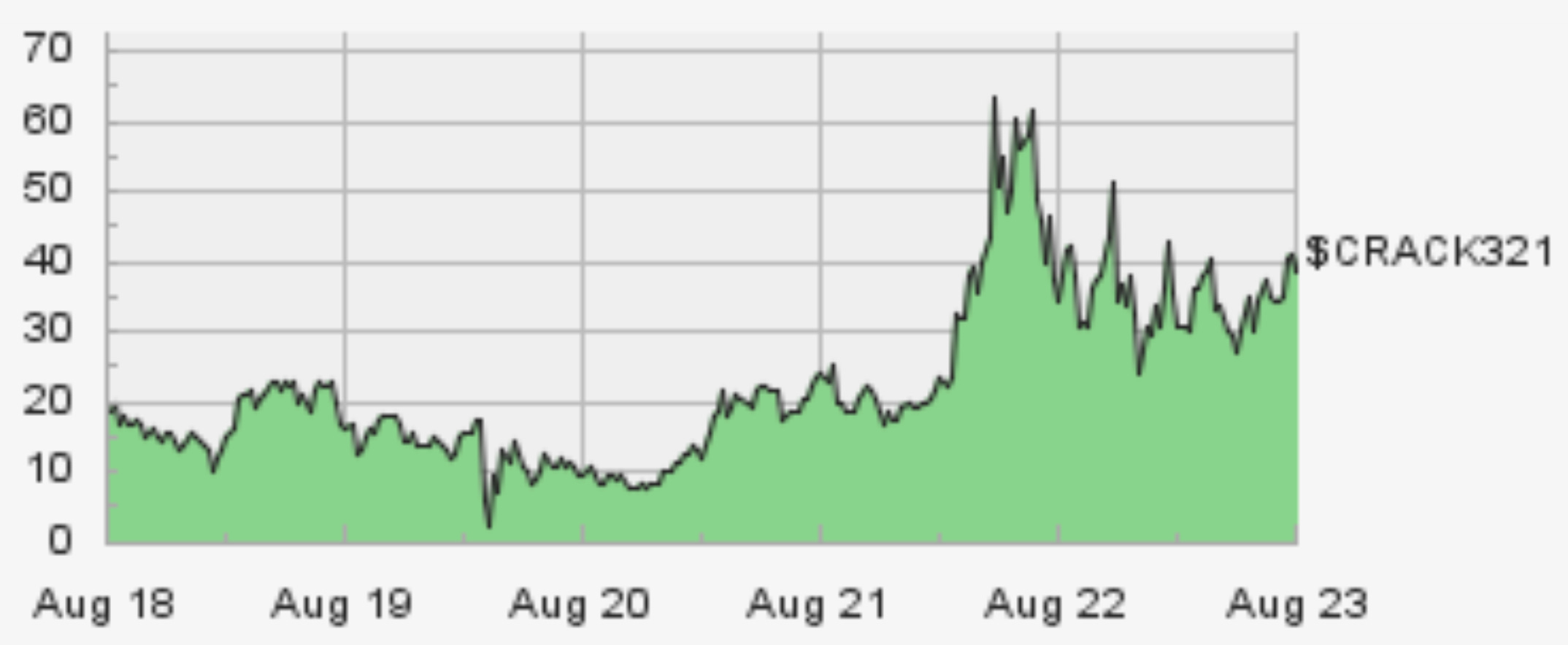

Crack spreads have been strengthening recently. They ended Q2 with $215M in inventory on their balance sheet (60% more than what they had at the end of the year) that will be converted to cash when sold.

I’m short $5 puts. I’m synthetically long the stock at around $4.50/share. I’m inspired by the Vertex story and I have my position sized reasonably (around 4% of portfolio if puts are assigned). Armchair CEOs can criticize Cowart’s decisions, but they can’t challenge his track record. The man has been winning for 20 years. If the term loan can be paid and the renewable diesel project works out, I can see this business generating $100-150M/yr in net income. If not, the Mobile refinery may be Cowart’s White Whale. Regardless, the cheaper it gets, the better it looks. I welcome the opportunity to sell $2.50 puts.

I don’t see Vertex as a no brainer. It’s a relatively small company. It has different risks. They’re doing something hard. They’re an underdog. Yes, they’ve made mistakes. There are many safer investments. Personally, I want to stick around and see what happens, and I’m rooting for Mr. Cowart.