Q1 Results for EC, PBR, and the BAK buyout offer

It's been an interesting few weeks for my favorite LatAm stocks. Here's a roundup.

Now that we have numbers from Braskem, Ecopetrol, and Petrobras, it’s time to recheck earlier posts and assumptions to see if we’re still on track. As I’ve written extensively on both of these names in the past year, we have quite a bit to check from.

On the business front, I feel that all of these names are performing more or less exactly as expected. Ecopetrol and Petrobras both continue to produce strong earnings, even despite a lower crude price, and Braskem seems to have turned the corner in the petrochemical market and has recently had interest from both ADNOC and Apollo for a buyout of Novonor and theoretically, minority shareholders.

I’ll be creating a post for each analysis, with the Ecopetrol analysis coming first and being free, and the other two posts being for paid subscribers only.

Ecopetrol

First thing is first, the EC share price has suffered recently, falling dramatically on the ex-dividend date. Confusion around whether the ex-div was for 1 dividend payment or all three? Belief it will be the last dividend the company will ever pay? Short sellers?

I’m inclined to think a little bit of all the above, plus the new CEO gave an interview on Colombian radio that was taken horribly out of context by media (Seeking Alpha published a headline: “Ecopetrol plunges as new ceo struggles to raise production amid restrictions”, and Colombian president Petro fired his whole cabinet due to frustration around failure to pass health reforms. The attorney general said he was acting like a dictator. Short sellers piled on the morning of ex-div:

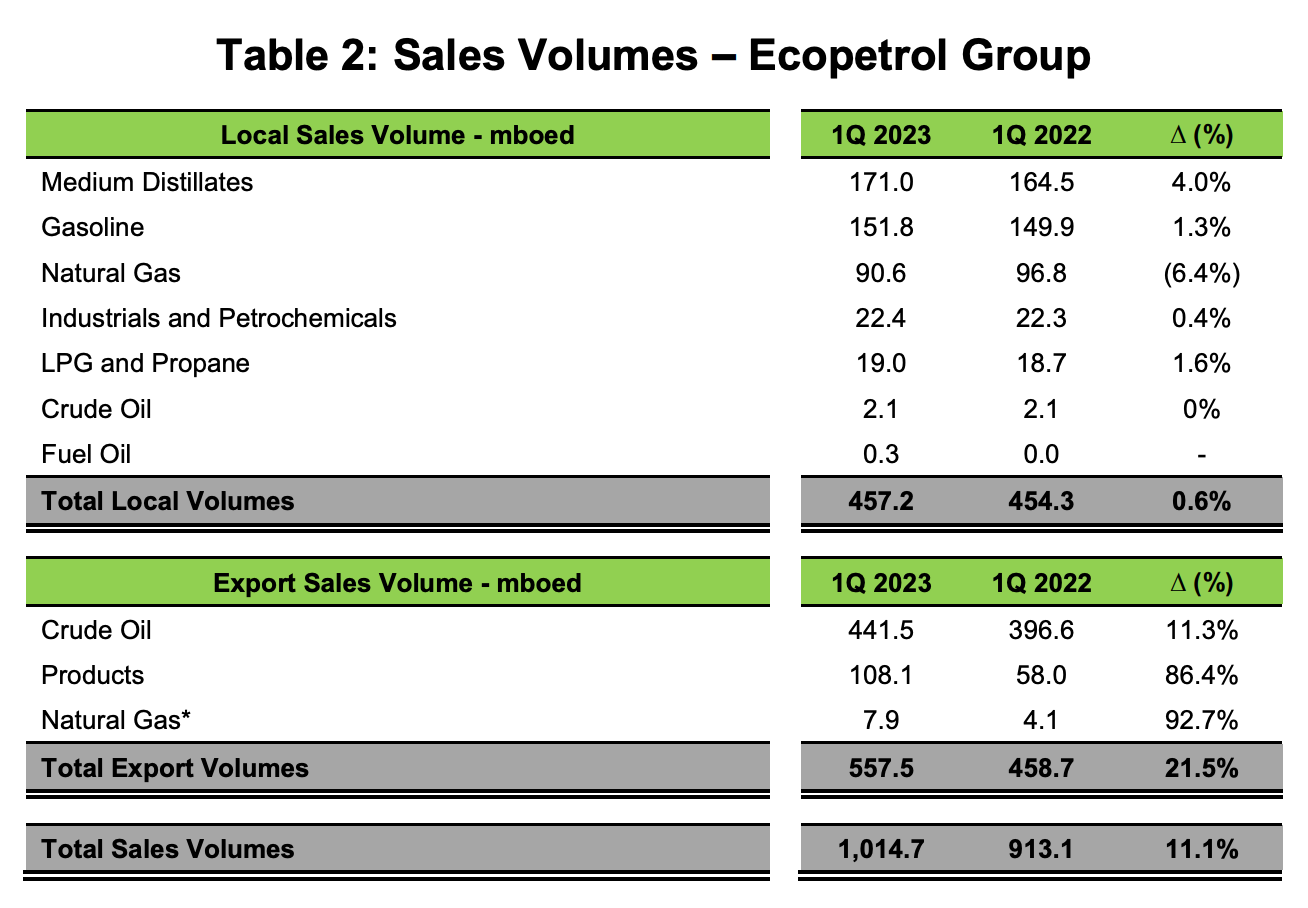

On the subject of production increases, the CEO actually stated that the company had the largest proven reserves in its history, and that the existing portfolio of leases was sufficient to drive production increases. Indeed, here are the actual Q1 production numbers:

The sensationalist SeekingAlpha article probably bordered on illegal manipulation, and completely misrepresented the reality, as the company was able to raise production by 4% YoY.

The flurry of negative news items, none of which had anything to do with financial fundamentals, drove the stock price down including the dividend effect, by 18% in a matter of days. The stock has recovered some, but is still down 12.5% since the day before ex-div, including the dividend payment.

In the end, the dividend - the first of three - was for $0.84/share. According to my own experience and many reports from others, no taxes were withheld from the dividend payment.

Now, to discuss what I believe to be the material issues: the numbers, the FEPC balance, and the effect of new taxes.

In my original article about EC, I postulated that the FEPC balance would be reduced by the amount of the dividend paid to the state.

That being said, there have also been some positive changes with the new government. For example, for years the government has used a method called the FEPC (Fuel Price Stabilization Fund) to effectively subsidize domestic fuel pricing. 19T COP (around 4B USD) has been included in the 2023 budget (according to recent conference call) already for paying back what the Colombian government owes the company. Additionally, over the summer the government agreed (and I think it is still the understanding) that the FEPC balance would be reduced in lieu of the government receiving dividend payments for its 80% holding.

While the FEPC balance still increased in Q1, according to the CEO this is due to a lag in the numbers. The expectation is still that 21.6B COP, around 2/3 of the current balance, will be reduced by the 3 dividend payments (minority holders get the dividend, the state does not get the dividend and instead reduces the debt owed to the company). Another 4.8B - in total the entire 2022 balance - may be compensated in another manner. The company is retaining the majority (~88.5%) of the cash from the dividend to offset the nation’s debt to the company.

Fuel prices have also been increasing every month since November. In effect, the “socialist” government is slowly reversing the subsidies put into place by the previous “right wing” government, raising prices by around 9 cents per gallon every month.

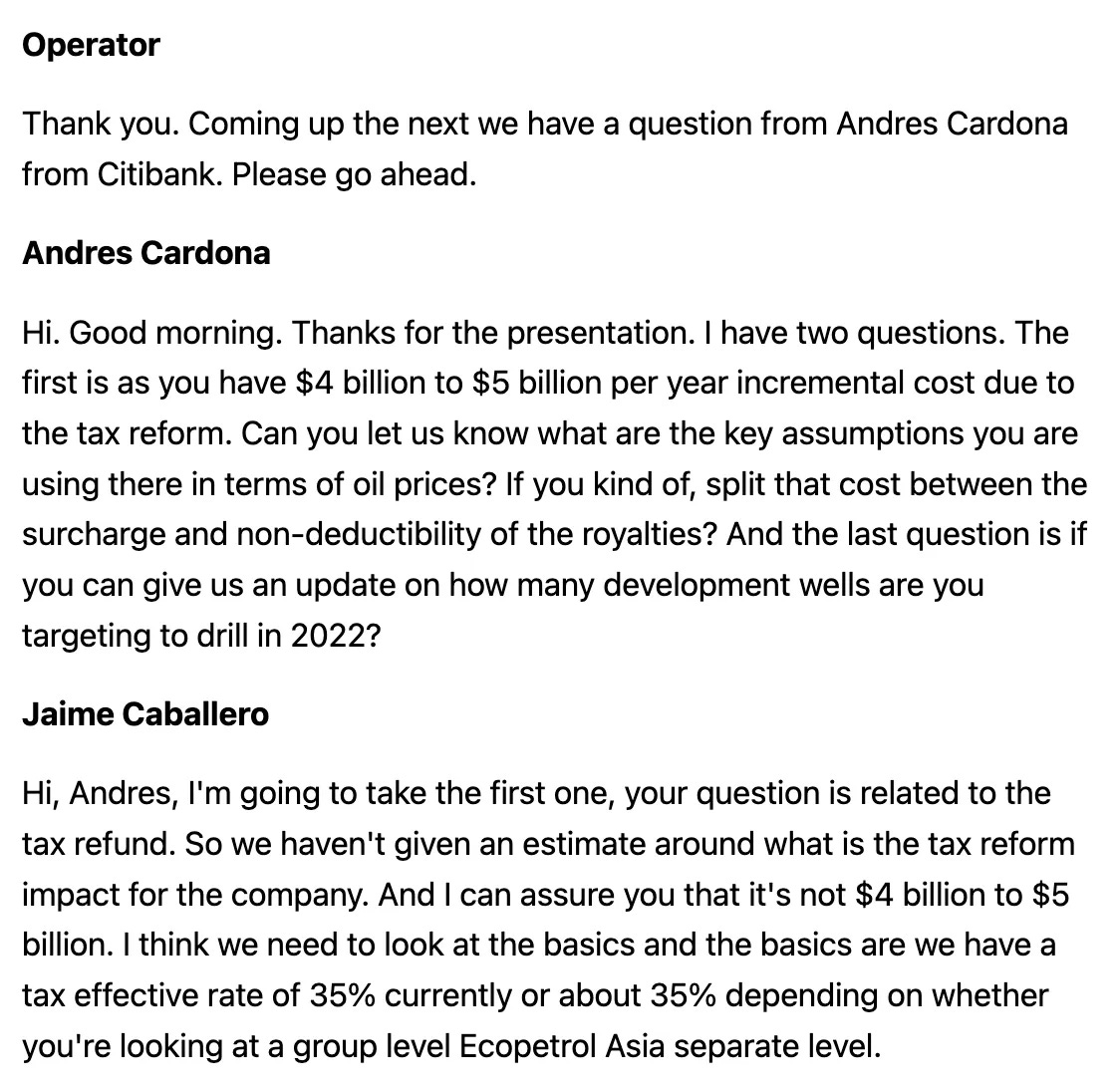

As for the tax changes, in my original article, I postulated that the market was dramatically overestimating the effect of tax changes (An export tax and loss of royalty deductibility) would be in the 7-15% range total added to effective tax rate.

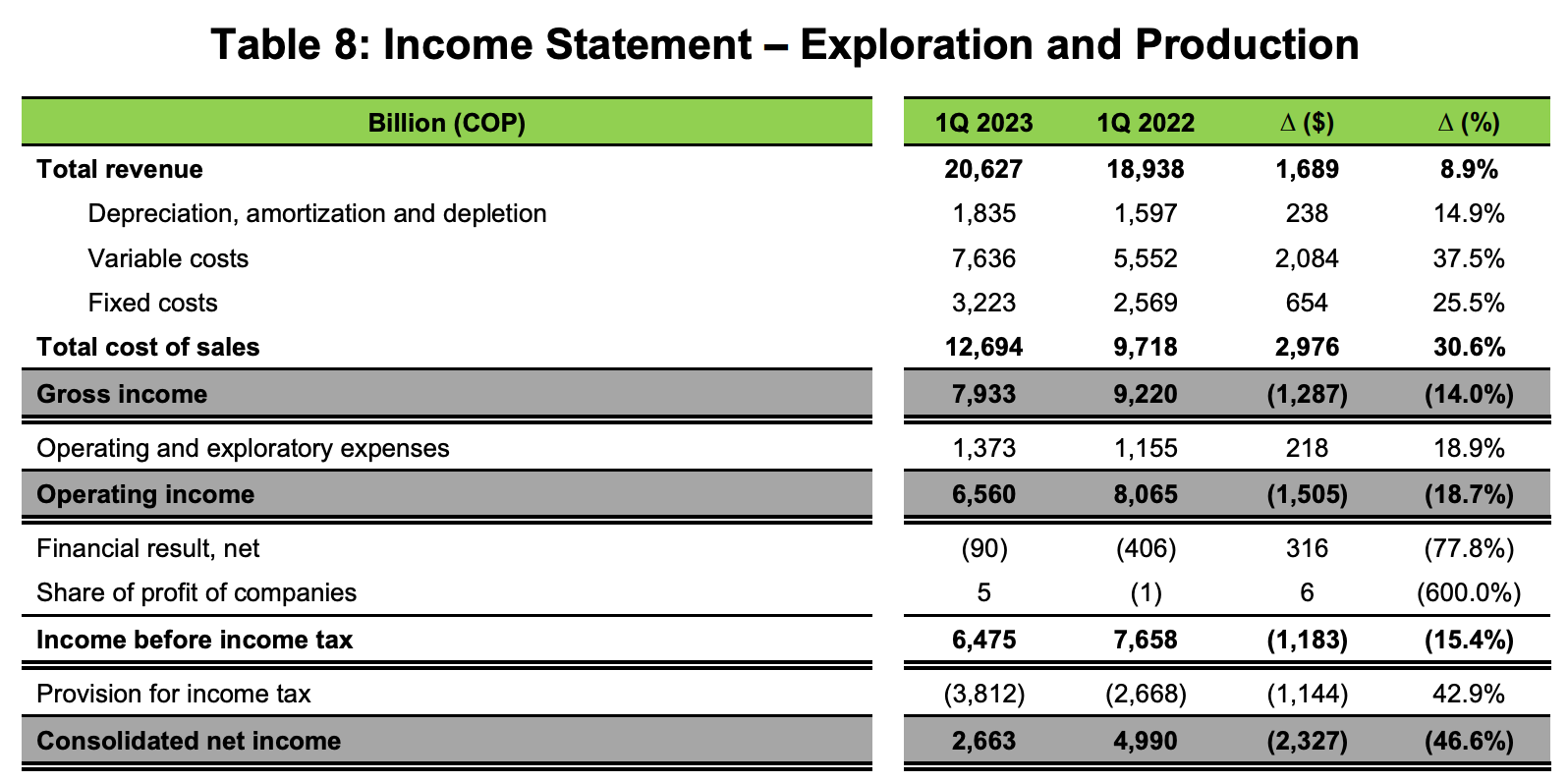

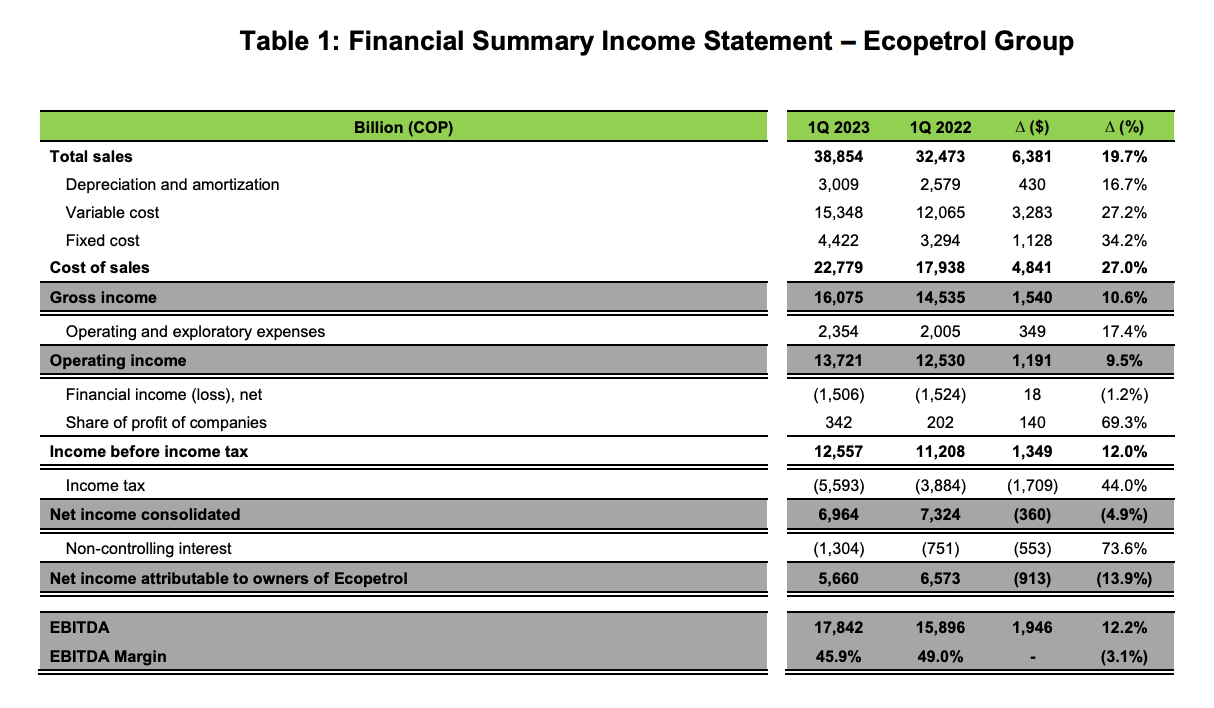

The company’s effective income tax rate increased in Q1-23 from 34.6% in Q1-22 to 44.5% in Q1-23. Consolidated net income was down by 4.9% and net income was down ~14%. In other words, my expectations were pretty close.

Now, let’s discuss Q1 results. The company managed to increase sales by an astounding 19.7% YoY. This was partially due to the new trading unit in Singapore, and partially due to the effect of growth from ISA (the utility acquisition). The biggest part of the equation for the better top line performance (operating income up 9.5%, EBITDA up 12.2%) was higher export volumes. Ecopetrol exported ~55% of their volume in Q1.

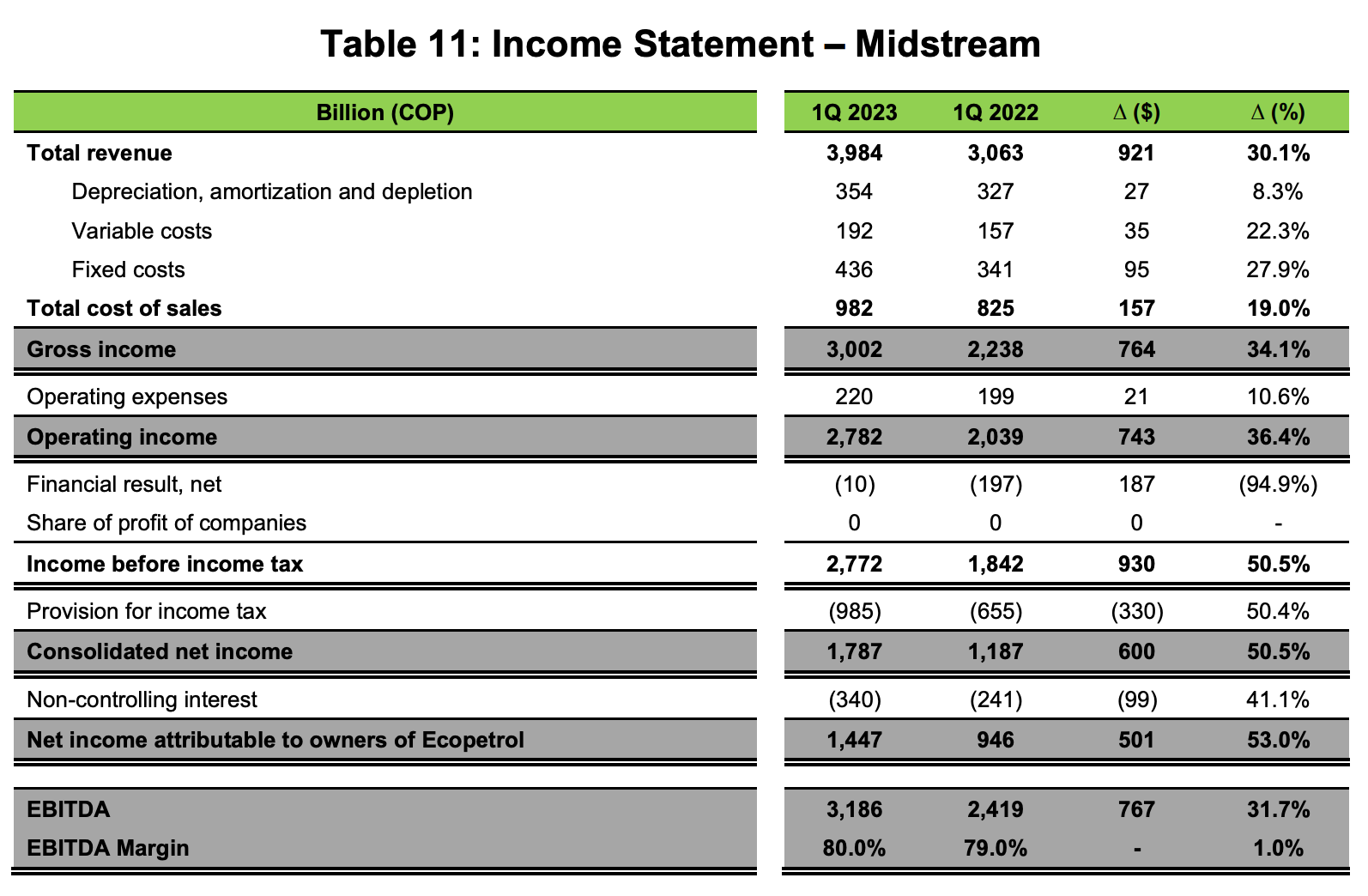

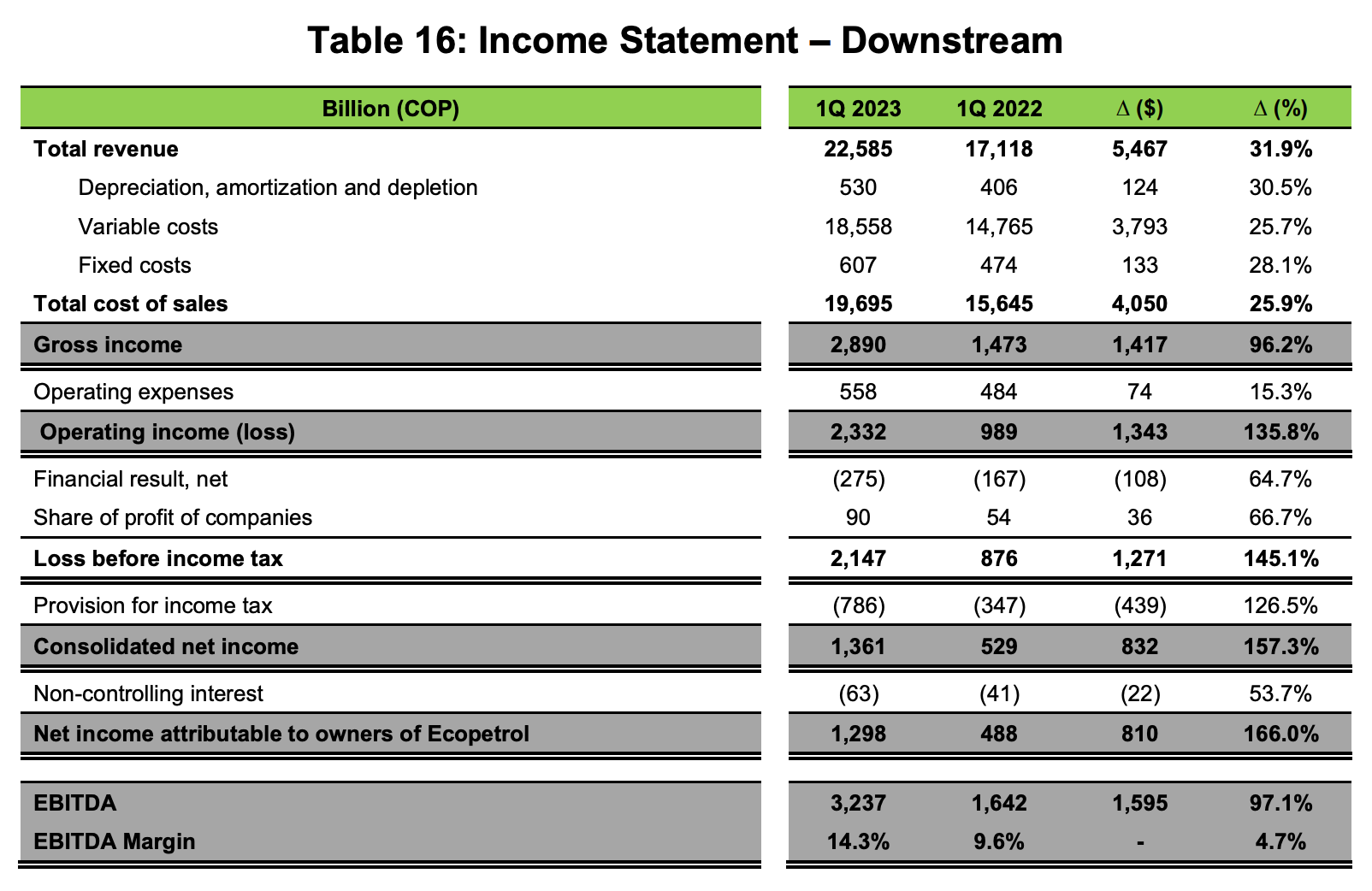

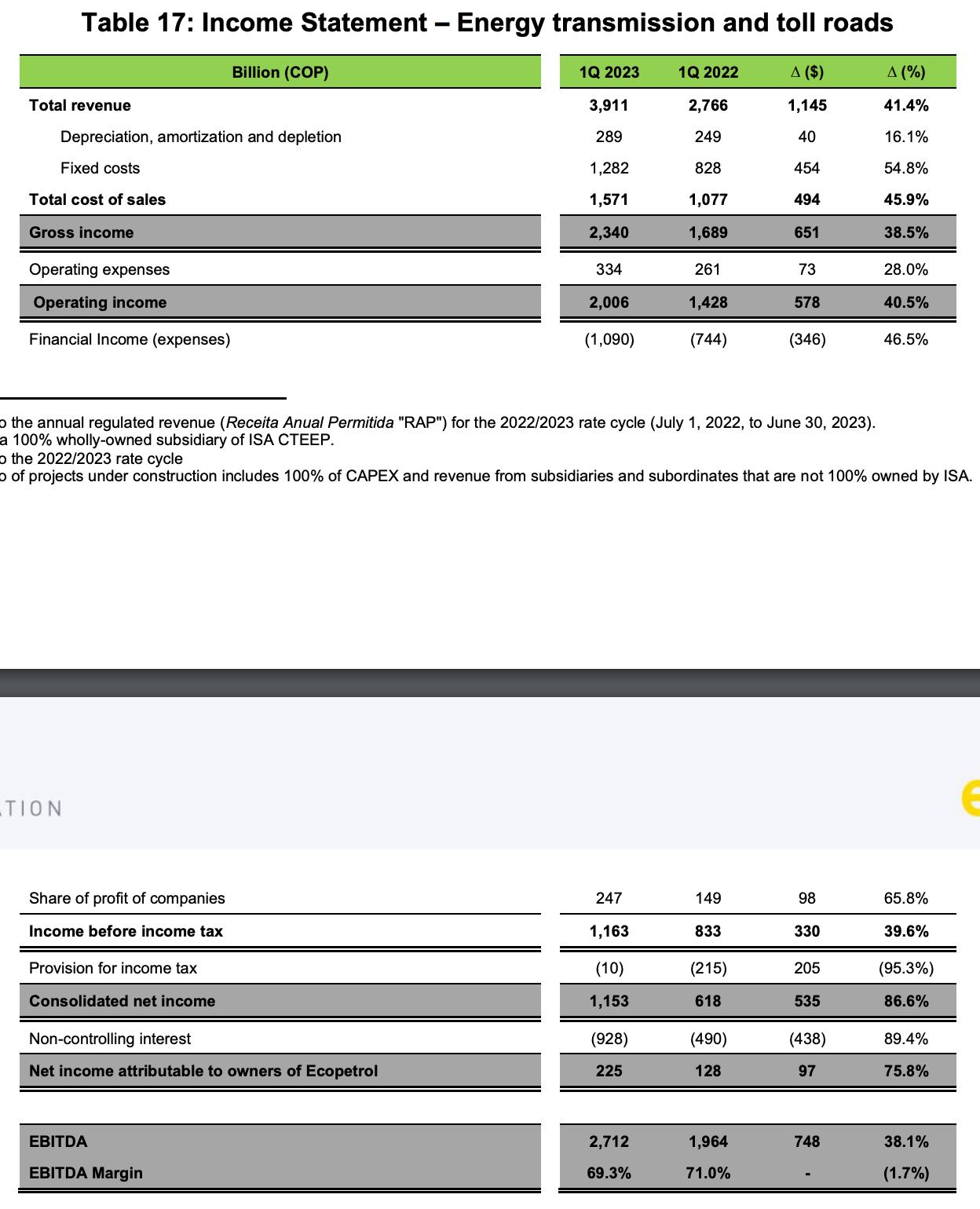

On a segment by segment basis, it’s worth noting that most of the tax impact showed up in the E&P segment. In effect, we as minority shareholders are getting a much smaller piece of the E&P pie. That being said, while the bottom line was down nearly 50% in the E&P segment (partially due to lower commodity prices, partially due to the higher tax impact), it was up 53% in midstream, 166% in downstream, and 87% in toll roads/energy generation (ISA).

In conclusion, while the tax changes are unfortunate, and I hope in future budgets the taxes don’t increase even more, we knew that this was coming and the total impact was very close to what we anticipated.

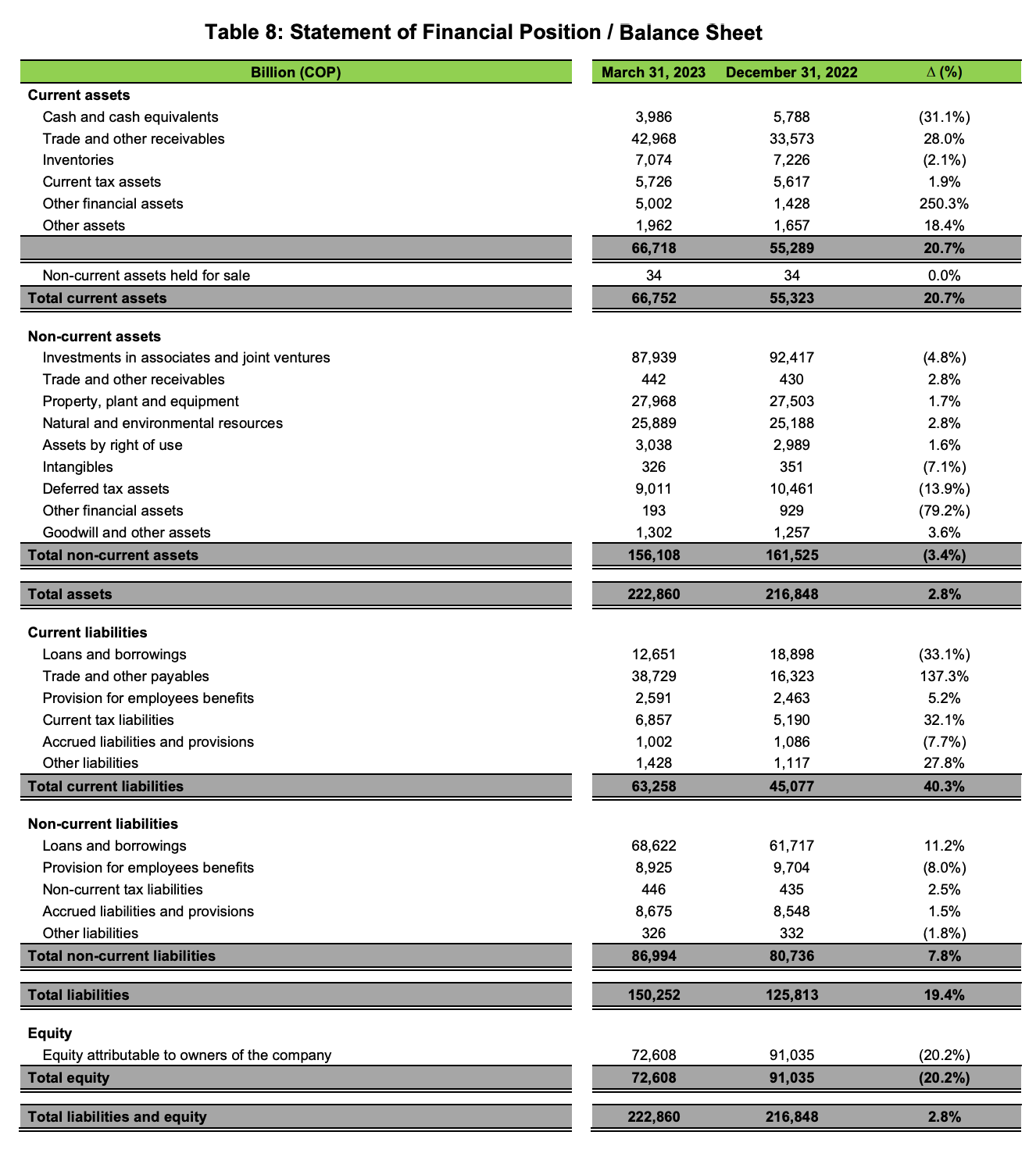

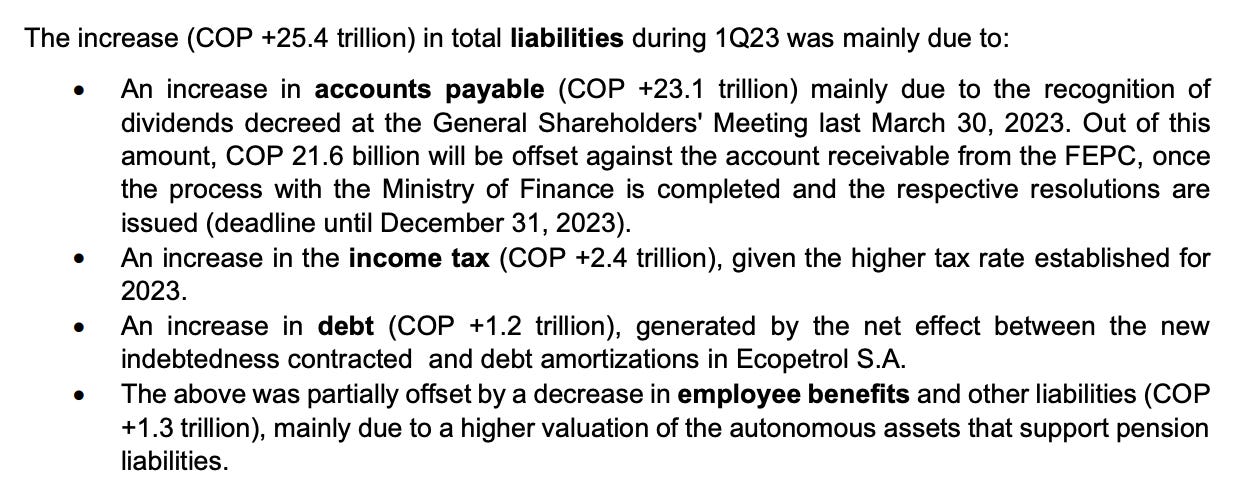

On the balance sheet side, the large “Trade and other receivables” balance is mostly the FEPC, while the “Trade and other payables” is mostly the dividend. These will offset each other. Equity is down due to the size of the dividend declaration, it doesn’t actually indicate that the value of the company is decreasing.

Conclusion

In summary, the tax changes are annoying, and the profits this quarter would have been significantly higher under the previous taxation regime. That being said, due to the excellent performance of the business and massive top line sales growth in spite of lower commodity prices, the bottom line is still quite good. They made $1.24B net this quarter, which puts them at likely a 3-4x valuation going forward. However, if we exclude taxation, from EBITDA, the business recorded closer to $2.7B in profits. Capex was significantly higher in Q1, but considering the incredible growth in several business lines and in the top line, it’s obviously working.

I want to highlight again market expectations on the tax reform impacts versus reality. Citi was estimating $4-5B USD in additional cost due to the tax reform. In the end, Citi overestimated by around 4x the total impact. If this year’s tax rates were applied to last year’s numbers, taxes would have been ~32% higher.

Ecopetrol significantly beat market expectations for the quarter, and the non E&P businesses are showing outstanding growth and profitability.

It’s important to keep in mind that the tax reforms have an impact on all the private producers as well, and Colombia may be forced to revisit tax policies which harm investment (and reduce state revenue) in the future. Luring private producers back to Colombia will also mean positive changes for Ecopetrol.

As for the political risks, We’re a few weeks away from the 1 year point when Petro was elected.

What would make me sell? Additional negative tax changes each year he’s in office, or changes to the constitution which imply he will become an actual Chavez/Maduro style dictator. We’re a year from the half way point for the Petro administration, after which I think the market will begin to fear less “what’s coming”, and begin to look at what has actually happened. I remain long EC, and am essentially at breakeven for the moment. I will continue to collect dividends and occasionally sell puts and calls.

Calvin's thoughts is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.