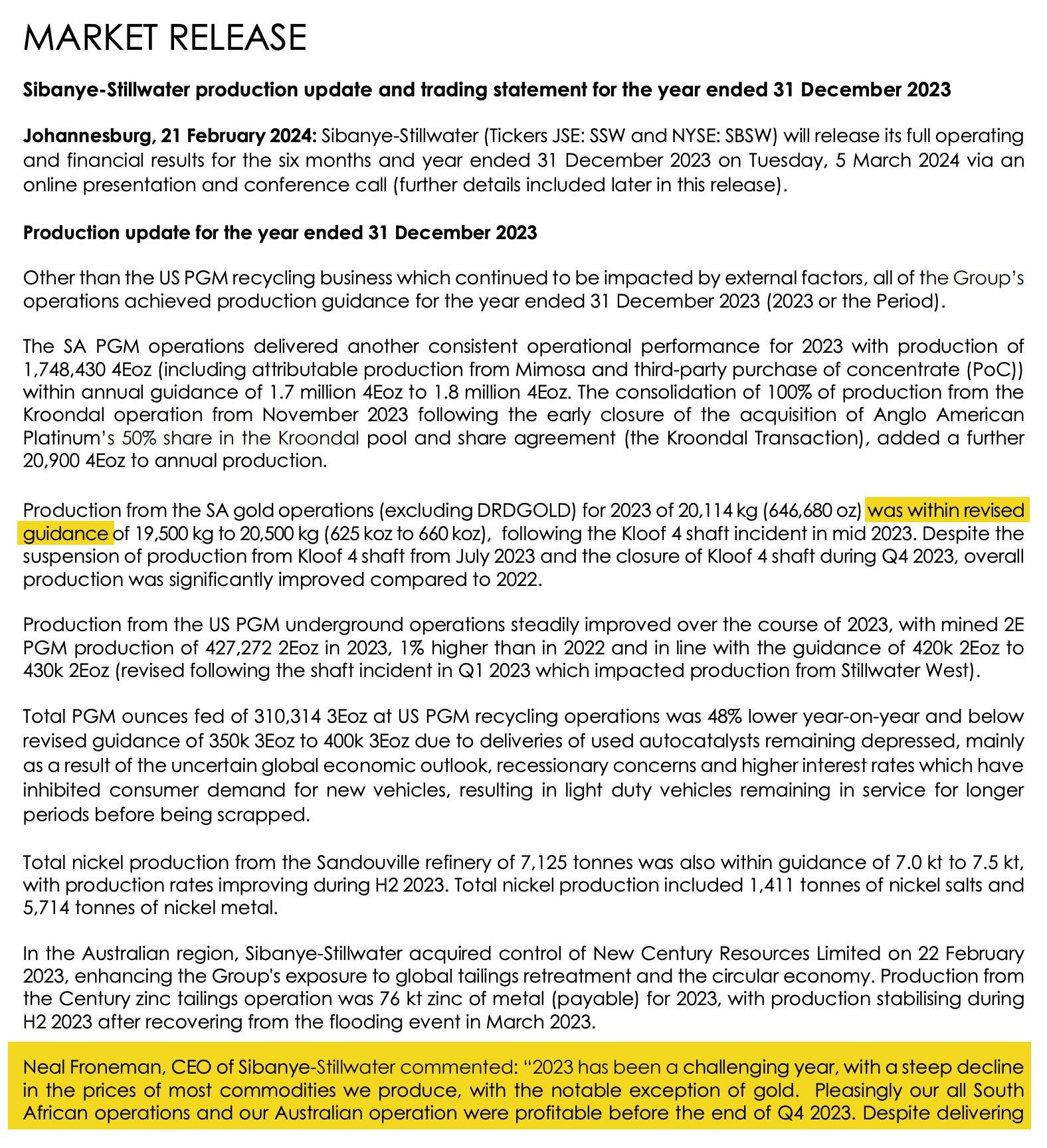

Sibanye Press Release on Production & Trading

My take on Sibanye two weeks before earnings

Sibanye Stillwater released the following statement in preparation for its 2023 earnings release. The US stock is down 7% in the US though still above the intraday lows made back in November. For me, the key point is that there is no adjusted loss (cash basis). The 2023 loss due to impairments was expected. See my highlights below.

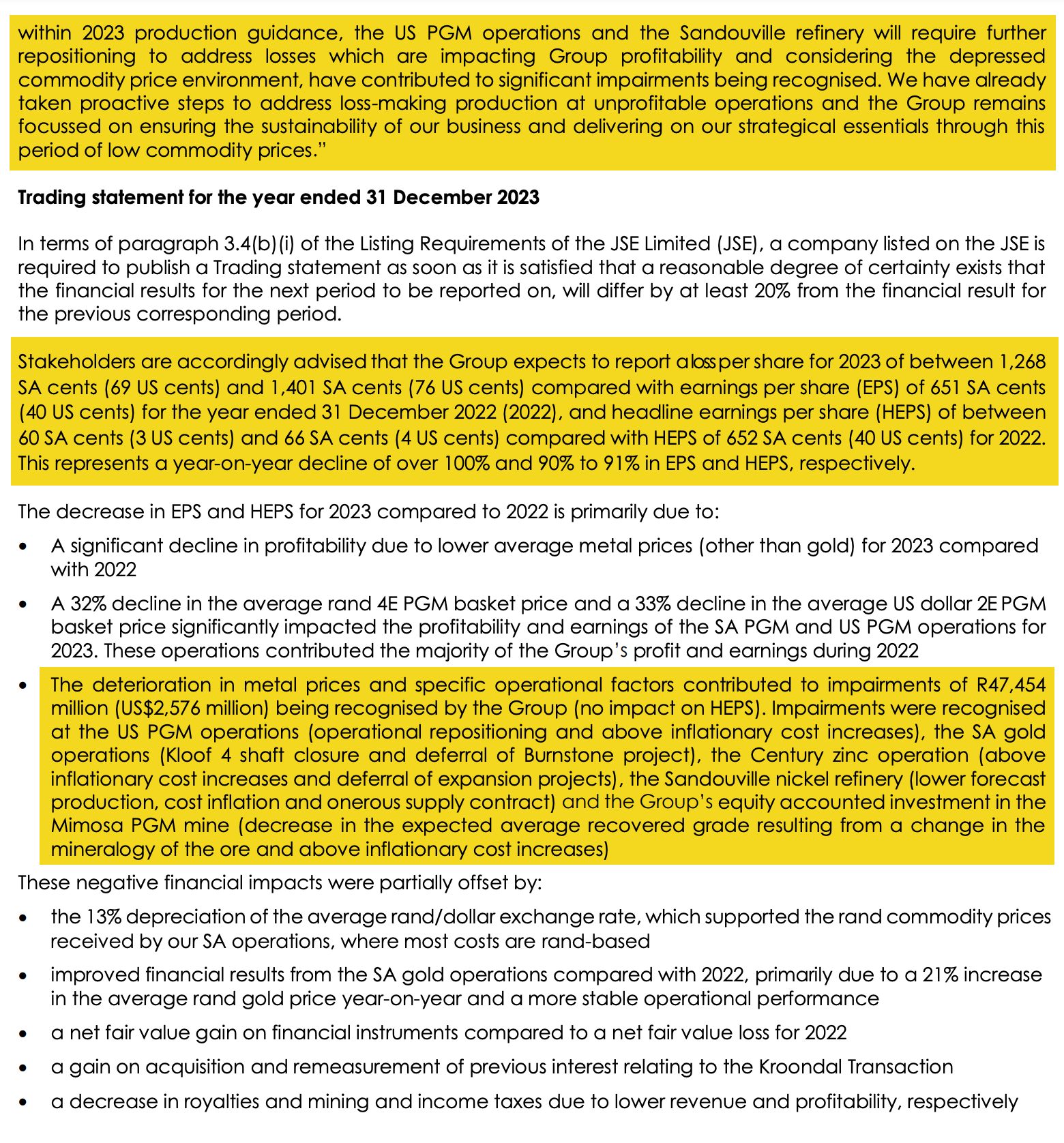

Let’s deconstruct a bit more. Where are the losses (impairments) coming from? As far as I can tell, likely from “Property, plant and equipment”, which would result in a ~50% write down vs 2022 levels.

It’s not pretty, but it’s not going to have much of a cash impact. The most important statement of this release was what the CEO had to say:

Pleasingly our all South African operations and our Australian operation were profitable before the end of Q4 2023. Despite delivering within 2023 production guidance, the US PGM operations and the Sandouville refinery will require further repositioning to address losses which are impacting Group profitability and considering the depressed commodity price environment, have contributed to significant impairments being recognised. We have already taken proactive steps to address loss-making production at unprofitable operations.

As I have been saying all along, Sibanye is able to adjust its operations to deal with the current pricing environment without suffering big cash losses.

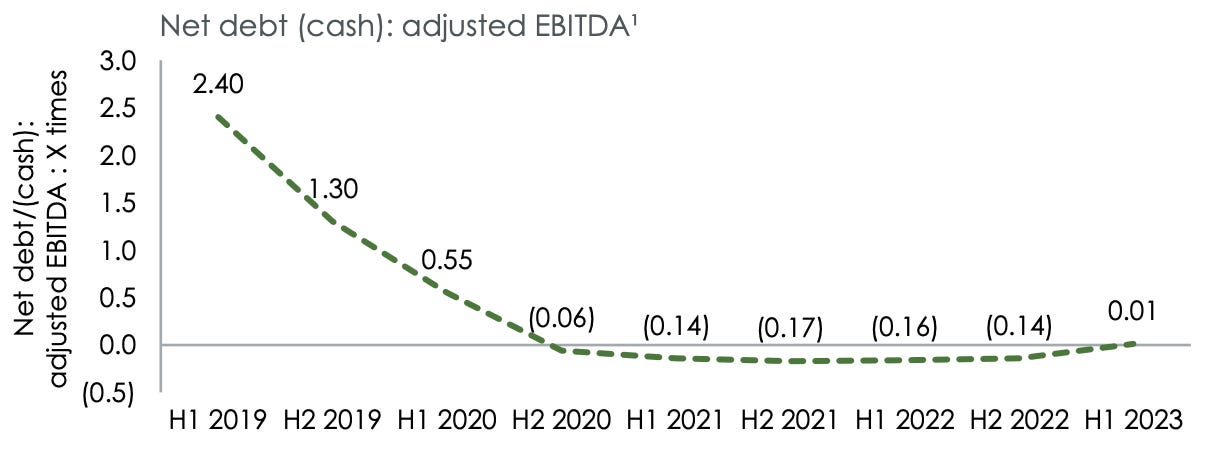

The fact remains (from February presentation) that the company remains essentially unlevered, having weathered the worst drawdown in its pricing environment in decades.

Anyway, my point is that the company itself is fine.

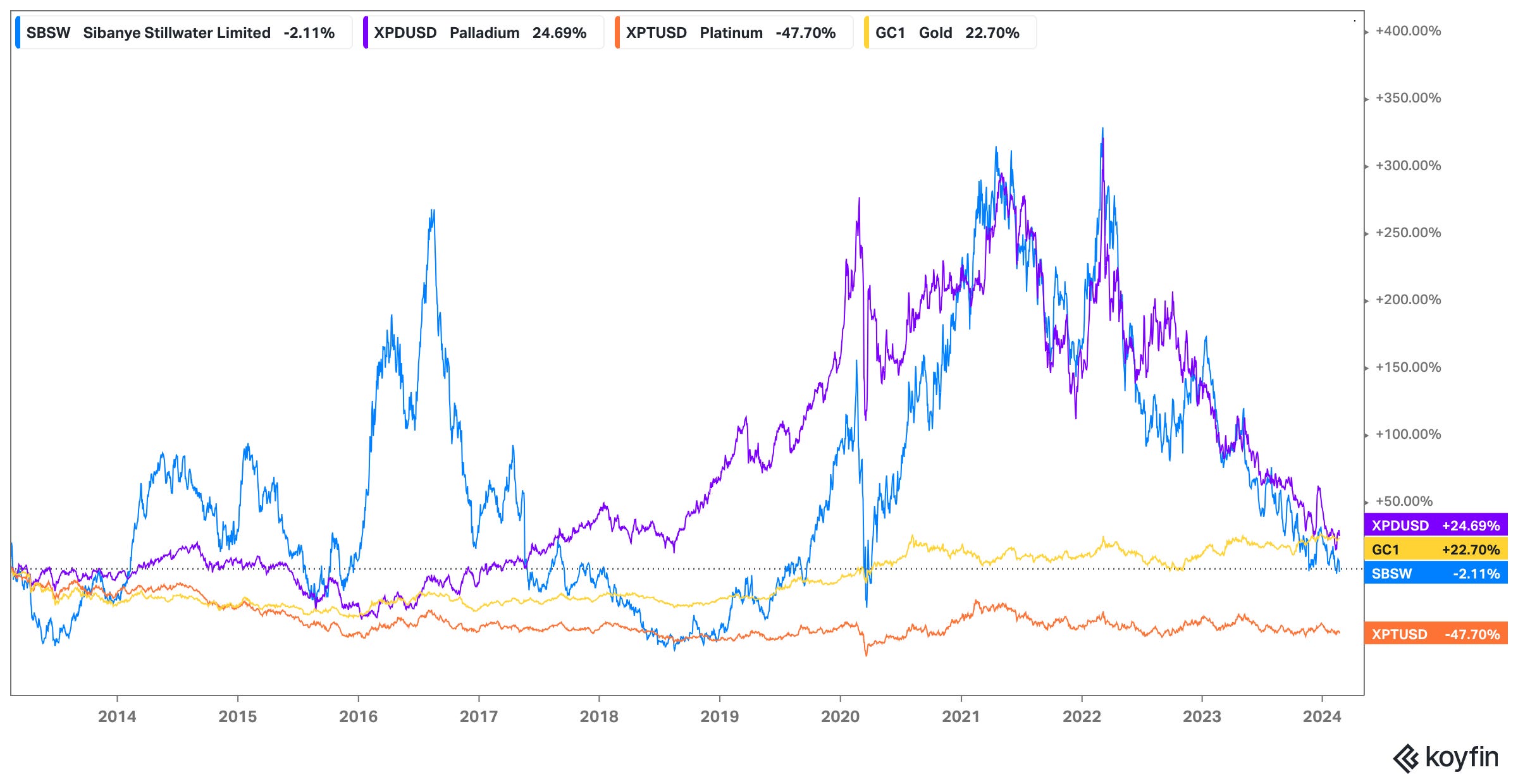

If we look at the stock itself, we can see that for several years the stock has simply followed palladium pricing.

Over the past few months, the company has underperformed its price basket.

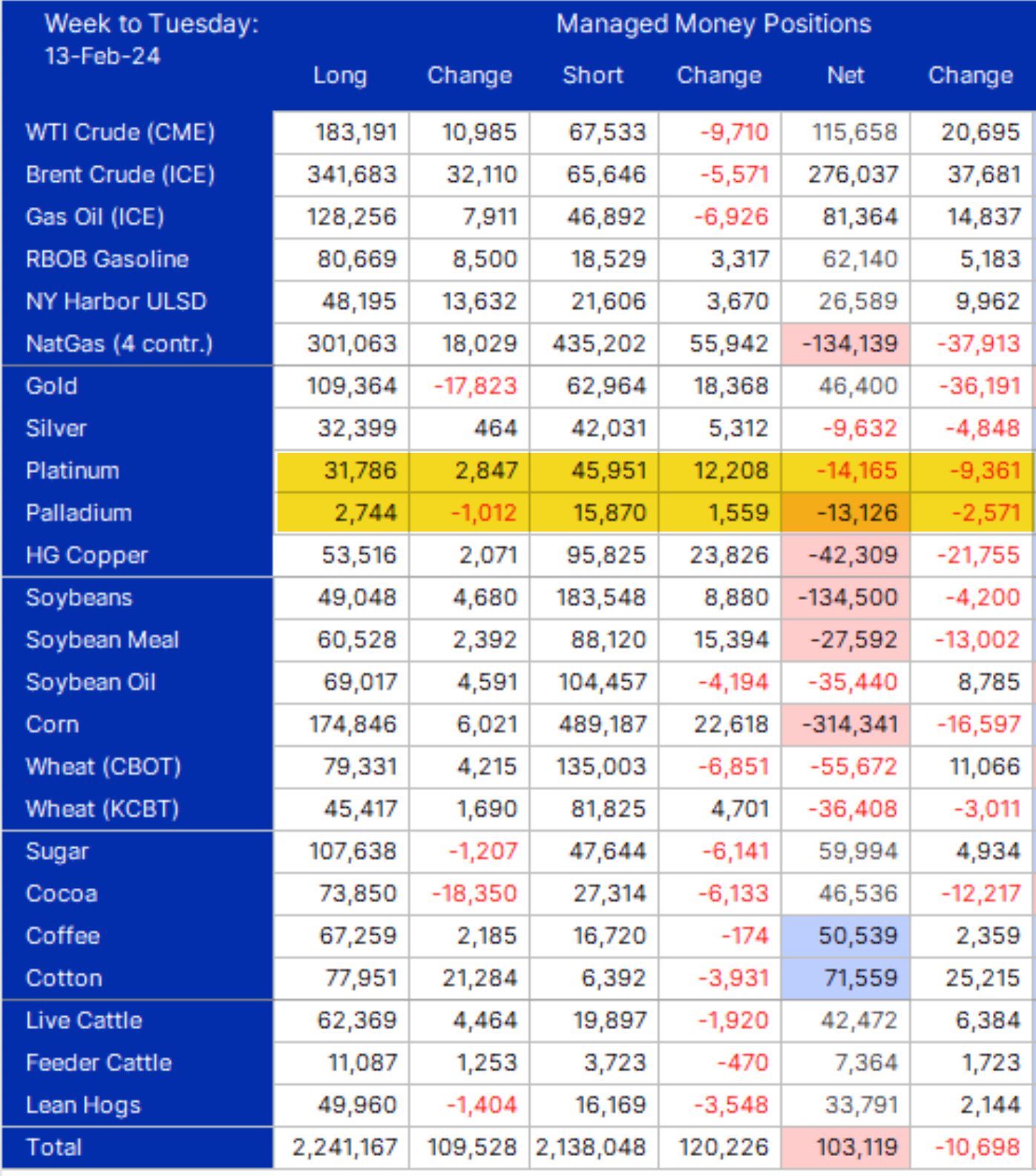

This is while platinum and palladium have large net short positions by managed money (along with many other commodities). Eventually these short positions are going to unwind (we saw a 35% spike in December palladium on just a tiny bit o fshort covering).

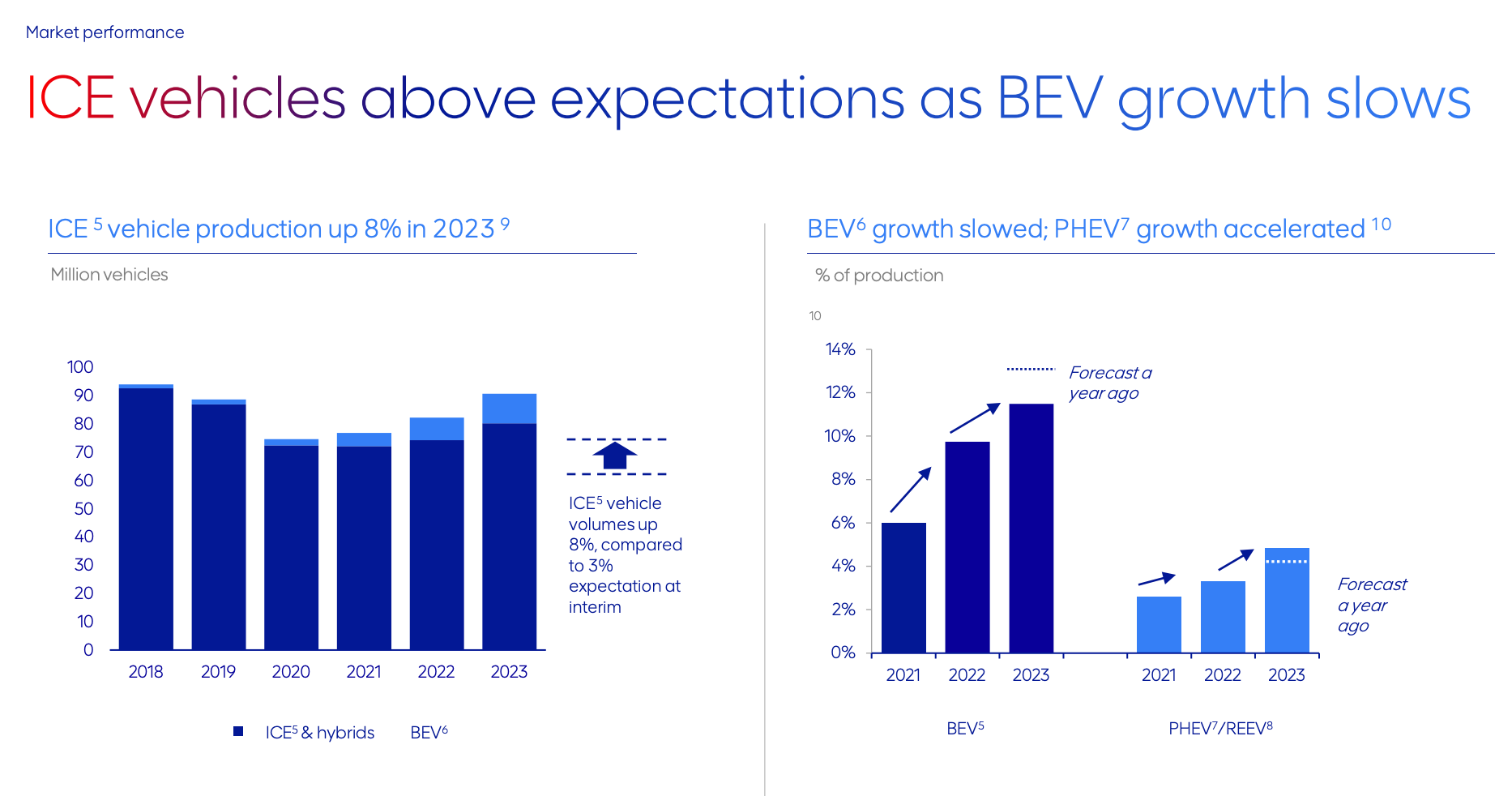

This coincides with the news the demand for BEVs is faltering, many producers (such as Anglo American) reducing production, and ICE sales increasing (catalytic converters are the main demand source for PGMs).

As Anglo American reported recently, ICE vehicles, which are the main drivers for PGMs, are back on the rise. Hybrids, which are growing faster than forecasted, actually contain more PGMs per car due to stricter emissions standards and combustion engine efficiency losses.

The net/net here is that while PGM prices have been weak, there are bright shoots on the horizon, and Sibanye, which is my preferred vehicle for expressing this cyclical turnaround, is weathering the storm nicely, despite the weak share price and balance sheet impairments.