The market is kicking me in the teeth

And why I'm just gonna keep taking it if I have to

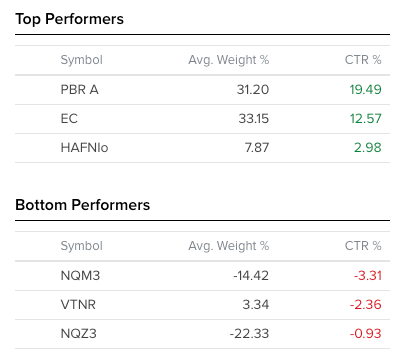

I began the year nearly entirely allocated to a few stocks: PBR.A, EC, and HAFNI.OL. Those all did really well. I held them. I bought them all when they were cheap and hated - as I usually run my book. Those stocks paid me nearly 20% of the NAV I started the year with just in dividends. I sold Hafnia a few months back, got some PBR called away recently, and reduced my EC position a bit also by having shares called away.

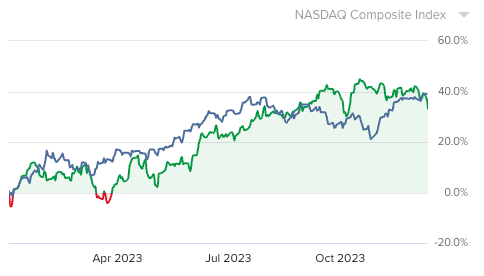

Well, along the way this year, I started looking at some other cheap stocks, and in Q2 and Q3, started buying them. Mostly, Braskem, Sibanye Stillwater, and Vertex Energy. In June I started shorting the Nasdaq. My performance has been bad ever since. The past few weeks have seen one of my worst drawdowns of the year, with both my core and speculative longs suffering.

My combined losses on Nasdaq futures shorts, Vertex, Sibanye Stillwater, and Braskem are up to around 10% of my total NAV. Meaning they have erased what would have been an additional 15% of performance for the year.

And yet, I’m not making any changes. I invest in two kinds of companies:

- Those that are cheap and pay well

- Those that are incredibly cheap and could pay well in the future

I bet against expensive markets and expensive stocks, even though that sometimes results in losses.

While this strategy doesn’t always work in practice, I can’t come up with a better theoretical way to succeed over time in the markets. It’s true, I frequently buy companies with problems. Problems are what makes a company cheap. In cyclical sectors, problems exacerbate weakness even further. Most of my buying from the past several months has been concentrated in VTNR, SBSW, and BAK.

If you follow me and my trades, I’m sorry if I’ve lost you money. I don’t have a crystal ball and I allocate money into what I see as the best opportunities. All I can do is say what I’m doing and my reasons for doing it. So I want to put out there in simple terms why I have been buying a lot of these companies, and why despite the current conviction test, I’m staying long.

Vertex Energy (VTNR)

I have followed Vertex for many years - starting with when it was a penny stock. This company has grown up and gone from ~$50M in quarterly revenue a few years ago to $1B in quarterly revenue today. This growth was funded with very expensive debt financing and ~50% dilution. The company has had very large capex demands over the past 2 years and made a very expensive hedging mistake in Q2-22 which tarnished market opinions. Furthermore, there was extensive insider selling in the teens and high single digits. When an insider finally bought earlier this year, it was followed by the death of a board member whose estate liquidated his shares after the company finally made a decent quarterly print.

Sentiment is awful, shorts are cocky (short interest is now above 20%), and an April 2025 maturity of a gigantic term loan (> 50% of current market cap) at 16% loom over the stock. And yet I’ve been a buyer since $5 and now have ~10% of my portfolio allocated to the name. Why?

It’s simple - their conventional refining made $65M last quarter on a $286M market cap. Their renewable diesel project is nearing completion. I estimate capex for 2024 will be ~1/3 of 2023 capex and 1/4 of 2022 capex. The company has half the cash on hand it needs to pay down its term loan and engaged Bank of America a few months ago. Prepayment penalties expired on October 1st.

I see in Vertex a company that is going to be generating an enormous amount of cash flow relative to their current market cap. Refining is a tough business, and if a refinery can achieve even a 5% long term net margin, they are doing well. At 2.5%, VTNR is very cheap in the long term, and probably trades today at 1-2x normalized FCF.

I believe the company will find a way to pay down or refinance its term loan. I believe they have options - deferring capex, selling off non core assets (of which they have many and have already shown they can monetize them). Due to the maturity dates, that must happen within the next 5 quarters. I don’t think more dilution will occur. Leverage is already down to 1.3x and will fall further. I think once the market figures this out, short sellers will figure out how wrongly they’re positioned and rush for the exits just as the market regains confidence.

Sibanye Stillwater (SBSW)

I bought Sibanye - a name I have also played before - because the 70% drawdown from the peak and 50% YTD drawdown was simply too juicy to ignore. The detractors say that Sibanye is in South Africa, a failed state (true), that the company has a high cost structure (untrue, most of their production is on the average or low end of the cost curve, and the few high cost assets are being shutdown), and that the company has a lot of debt (in reality it is close to net cash).

What happened here is not unlike what happened to many cyclical businesses during covid. Prices crashed, production was rationalized, and there will be profitability again on the other end of the cycle. To me, the appeal of Sibanye is purely around the PGM (platinum group metals) market recovering. PGMs are currently in a supply deficit, despite the cratering price. Total inventory levels are nearing covid lows. PGMs are up 2% today even as Sibanye stock is down over 5%. I bought a large amount of SBSW shares at around $4 when the convertible bond deal was announced. I believe the company will continue to rationalize its production (shutting down higher cost assets) as per announced and completed restructuring over the past few months. I think they will remain at least cash flow neutral and possibly generate small profits at current PGM prices, while their gold production should be profitable now that Kloof has been shut down.

I see in Sibanye Stillwater a company that paid nearly its current share price in dividends over the past 3 years and has no real dividend concerns. While I don’t have a crystal ball for what happens to PGMs or gold, many mining experts are especially bullish on platinum. I think Sibanye will pay big on a metals recovery.

Braskem (BAK)

Braskem is a plastics company. The business is somewhat similar to refining. I first bought Braskem simply because the equity looked cheap compared to the cash generation potential. If you look back over history, Braskem has traded in a truly cyclical range, becoming cheap at times but always going back into the $20s and even $30s. The stock is at $6.80 right now, which is close to the cheapest it’s been in the past 20 years.

Braskem has had a few things going against it. One, the salt mine disaster in Alagoas in 2018 (which resulted in the city of Maceió being evacuated in 2019 and nearly 14B BRL in relocation costs and damages). Basically, the company was using fluid (somewhat similar to fracking) in order to turn salt deposits into a brine and bring them to the surface. There was a structural leak and water started flooding in. The area around the mine began to sink, and ~70,000 people had to be relocated.

While this is a negative story, it didn’t stop Braskem from hitting the mid $20s in late 2021. The mine has finally collapsed, and while that has garnered a lot of negative press and some new groups looking for compensation, it’s far more likely in my opinion that the story is closer to its conclusion than the midpoint. Braskem set aside all the liquidity it needed to pay damages and continue operating for several years. They have assets all over Brazil, Mexico, and the US, and the loss of the Alagaos mine was already built in 5 years ago. Braskem produces 2/3 of the plastics in Brazil and is essentially too big to fail.

The company also has some idiosyncratic factors which are currently headwinds but which will soon reverse. The company’s operations in Mexico have to import natural gas from the US to produce plastics in Mexico (and the Mexican market is in a big deficit). This results in huge transport costs. However, in 2024 or 2025 Braskem will complete a new port which will allow them to bring in LNG by sea rather than truck or train, which will make their Mexican operations extremely profitable, even in the current petrochemicals market.

Braskem is a misunderstood company which has a very comfortable maturity profile and lots of liquidity but is trading like it’s an imminent bankruptcy risk. Other large industrial concerns see this, and multiple offers have been presented (though none accepted) at a 100%+ premium to the current share price.

ADNOC is the current interested buyer, and has presented an offer at ~$15.30 per share. If you ask me who knows the value of the company better - fund managers who think it’s worth $6.80, or industrial giants who think it’s worth more than twice that (and Novonor, the controlling shareholder, who thinks it’s worth even more), I would go with it being worth at least what the industrial giants say.

I think Braskem has zero bankruptcy risk, I think the $2.7B market cap is ludicrous, and I think that this company at this price is a double at the very least and very possibly a multi bagger if held over the cycle. In its best years, Braskem makes more in net profit than it currently trades for. To point out another factor which the market seems to be missing - Braskem should be trading higher as its feedstock cost drops. Petrochemical feedstock costs are greatly impacted by the price of oil derivatives and natural gas - both of which Braskem buys a lot of.

Conclusion

I obviously don’t have a crystal ball and I don’t always make money over short time horizons. Frequently I try to catch a falling knife and get cut. All three of these stocks have been falling knives. I have been buying and I have been losing money.

People often say “Why don’t you wait for the chart to turn? Why don’t you wait for the fundamentals to recover?” The issue with that is you end up actually buying closer to a mid cycle valuation and you’re chasing. How do you then know when to sell? How do you have conviction on pullbacks?

To me, I think about the downside, and I guard against the downside by not using leverage and waiting until I see something as fundamentally cheap. I am buying all of these companies because I see the average price of shares in the next 3-5 years as being far higher than the price of shares today.

Will the tide begin to turn as tax loss selling abates? Will funds stop chasing passive flows pushing end of year money into index funds and start looking for beaten up value? I don’t know. All I can do is learn about companies and make my own decisions about what it’s worth fundamentally and what it can pay me.

I think all of these companies have 100% upside in the most pessimistic case. While the market has been kicking me in the teeth - overvalued companies becoming more expensive, cheap companies becoming cheaper - I don’t see a better way to do it.

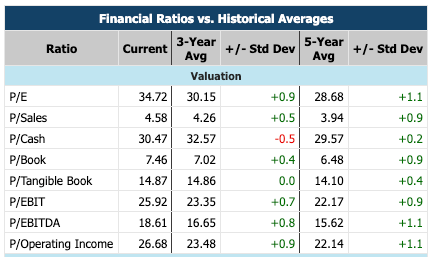

The Nasdaq today is overvalued on nearly every conceivable historical metric. The CAPE ratio for the Nasdaq 100 is over 50 - near an all time high. Meanwhile the market thinks Braskem is literally worth less than half of the offers made by large industrial companies.

History shows that the time to by cyclical companies is when everyone else hates them. The time to sell is when others love them. Value investing may not be a perfect strategy, but it’s the only way to make money in markets that at least to my mind, seems repeatable. I’m sticking with it.