When money falls from the sky

An unexpected turn of events for Altisource Portfolio Solutions (ASPS)

Once upon a time, a guy named Bill Erbey started a company called Ocwen Financial that would grow from a tiny mortgage servicer in Florida to an empire spanning all 50 US states and peaking at billions in revenue before it became embroiled in legal battles due to taking advantage of borrowers at every phase of the mortgage servicing process. People didn’t read the fine print, and Ocwen fleeced people so good that eventually the Consumer Financial Protection Bureau got involved. At its peak, it was the largest non bank servicer of mortgage loans. In the end, Ocwen paid billions in settlements and was barred from engaging in some forms of its business by regulators for several years. Did Ocwen do anything wrong? Probably no more than anyone else in the industry. They ultimately ran afoul of regulators, most likely, because they flew too close to the sun and got too greedy. In 2017 Ocwen was banned from originating mortgages in dozens of states. Revenues declined more than 60% from 2014 till today.

Anyway, what does this have to do with Altisource? Along the way (in 2009), Ocwen spun off its foreclosure servicing business as Altisource. This spin off made hundreds of millions in net income during and after the Great Financial Crisis processing foreclosures. They built a large suite of real estate software tools around all sorts of real estate processes, but foreclosures were the bread and butter.

A lot of that revenue came from referrals from Ocwen, and as the former struggled, Altisource’s fortunes took a turn south. The company’s revenues started nose diving, declining more than 40% from the 2014 peak through 2019. With the start of the pandemic, and a total moratorium on foreclosures, it seemed the fate of Altisource was sealed and the company was doomed for complete collapse. Indeed, revenues continued to collapse through Q2 of 2021, as US foreclosures reached an all time low. This is about the time I started developing a serious interest in the company. Despite the dark history with Ocwen - I thought hey, these guys ran afoul of regulators - but they built more than one multi billion dollar company before, surely they can do it again.

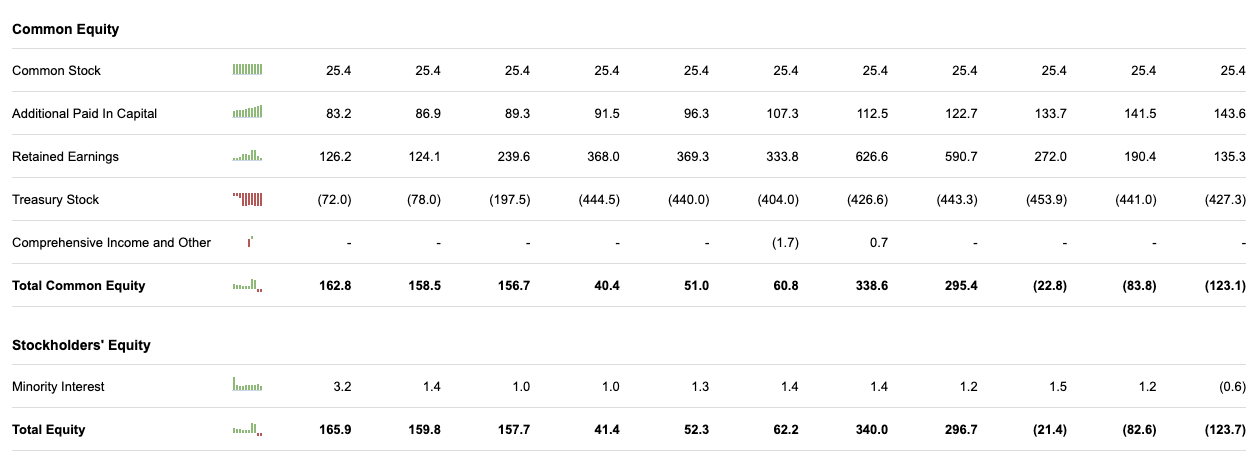

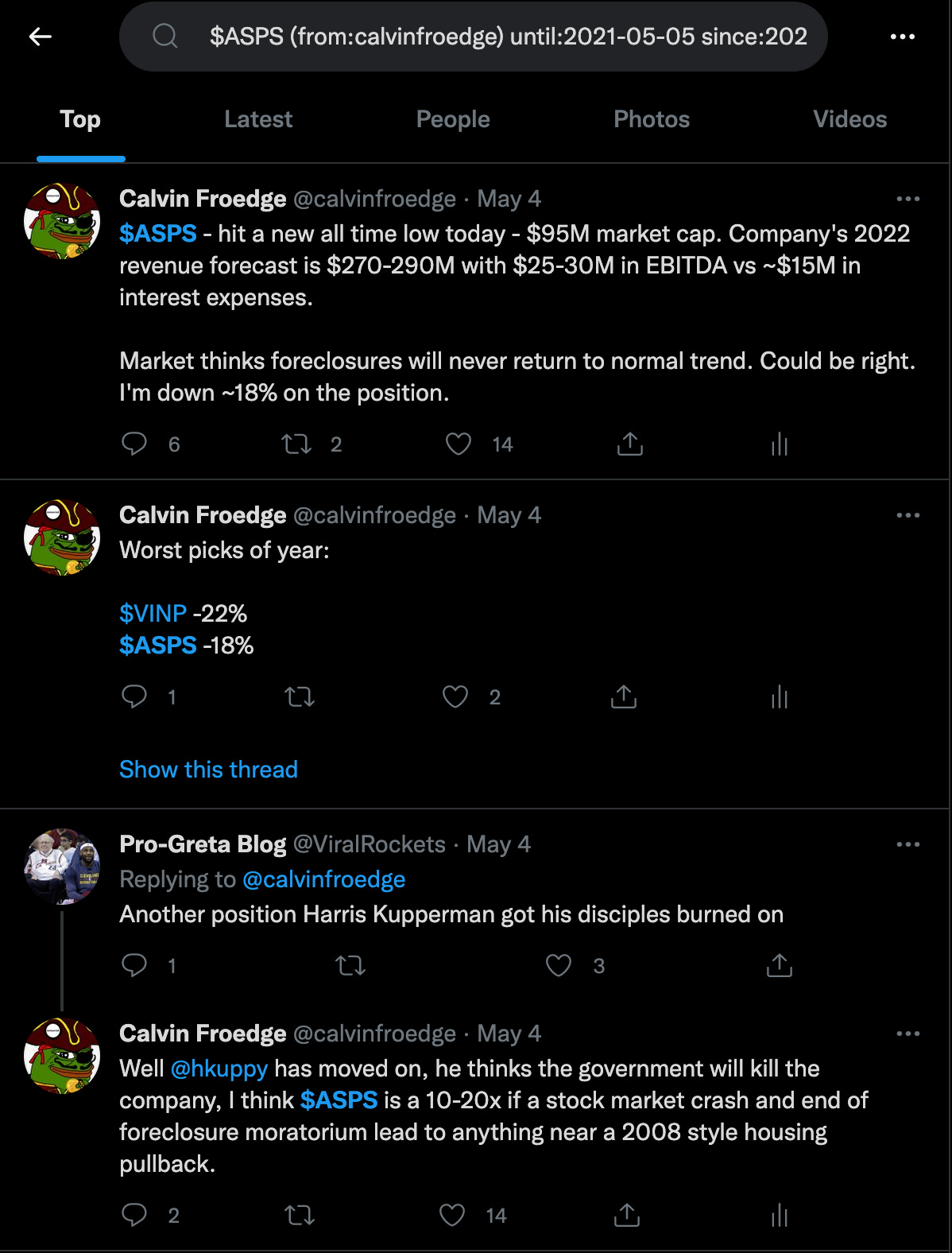

On paper, things looked terrible - negative equity, massive losses, and negative cash balances. Their main source of income (foreclosure processing) had literally been made illegal. Glassdoor reviews for the company from employees were like rats fleeing a sinking ship, warning the other rats still on the ship. This was the sort of company that nobody would touch with their worst enemy’s money. Kuppy, the guy who first brought the company to my attention in 2019 as a “long short” idea on the US housing market, had similarly given up all hope.

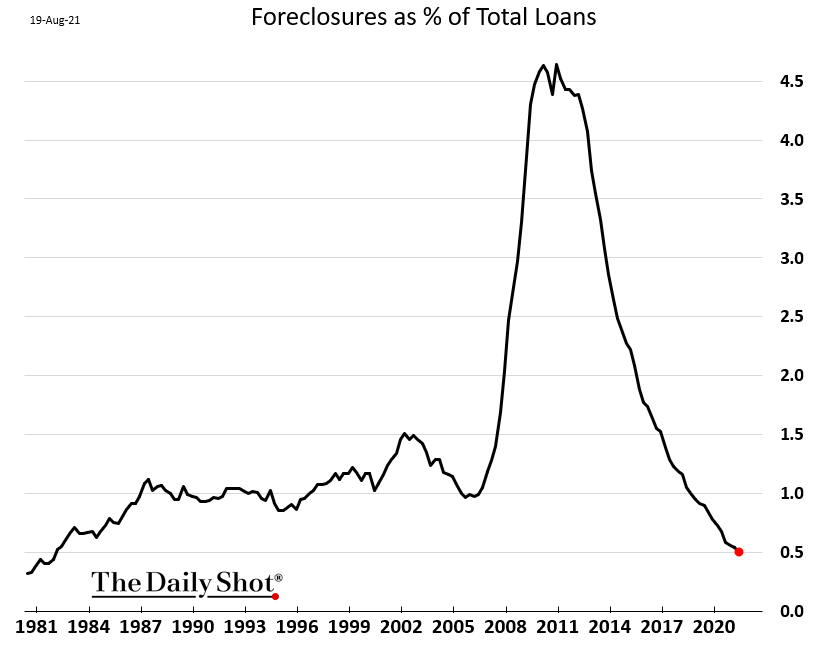

I saw something that everyone else had apparently missed. Foreclosures weren’t just low - they were at forty year lows. Foreclosure rates hadn’t been so low since the early 1980s when the Federal Reserve started raising interest rates to get runaway inflation under control. I recognized that Altisource didn’t need a 2008 style collapse to be a good investment, it just needed a mean reversion. The idea that foreclosures would be “not allowed” forever seemed crazy to me. Certainly, people must pay their debts to be permitted to stay in their homes, right?

Being an investor in mainly cyclical industries, I liked the setup - a combination of Ocwen’s troubles and an unprecedented ban by the CDC of all agencies on evictions. Everyone was convinced the United States was implementing socialism at the Federal level without pausing to think. Then the headline:

“U.S. Federal Court Vacates CDC Nationwide Eviction Moratorium”

I was already long the stock, and literally the day before was on the verge of losing hope:

Well, everything changed on the discovery that rule of law still meant something in the United States (and that CDC didn’t really have authority over the housing market). A ton of money rushed into the stock, and though it would be volatile over the next months, it hasn’t hit the lows since.

However, I kept the position small, knowing that there was a lot of risk, given the company’s dwindling cash position and nearing maturity wall. Then another positive development occurred: the second largest shareholder gave them a credit line roughly equal to their cash position. On top of the continued reductions in burn rate, the debt didn’t look so scary, anymore. Foreclosures were set to restart, and the company now had some time to wait for activity to pick up. I added a little bit.

Then came the disclosure that Altisource had put up its mortgage origination business for sale - a sort of stop gap survival mechanism to cope with the precipitous decline in foreclosure revenues. With $60M in revenue and comps that weren’t directly related going for 10-15x revenue, I thought, “Ok, hey, maybe they can get a decent valuation and pay a good chunk of their $245M debt with the sale”. Things seemed a bit less scary, and I added a little more.

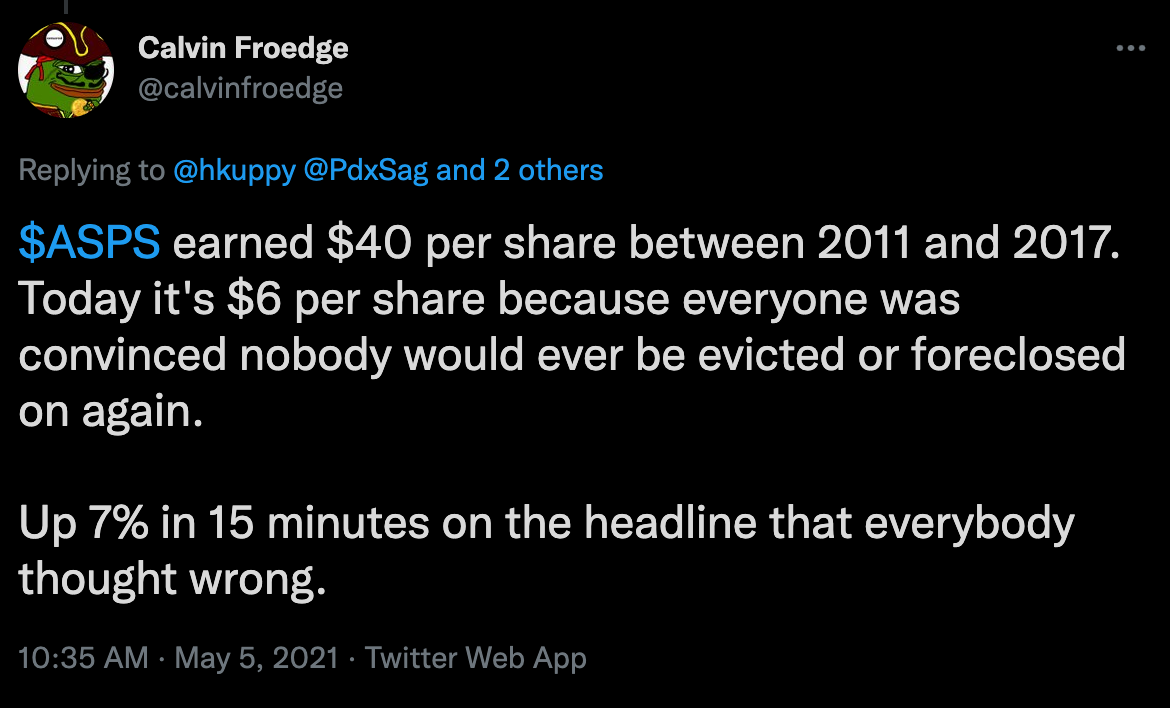

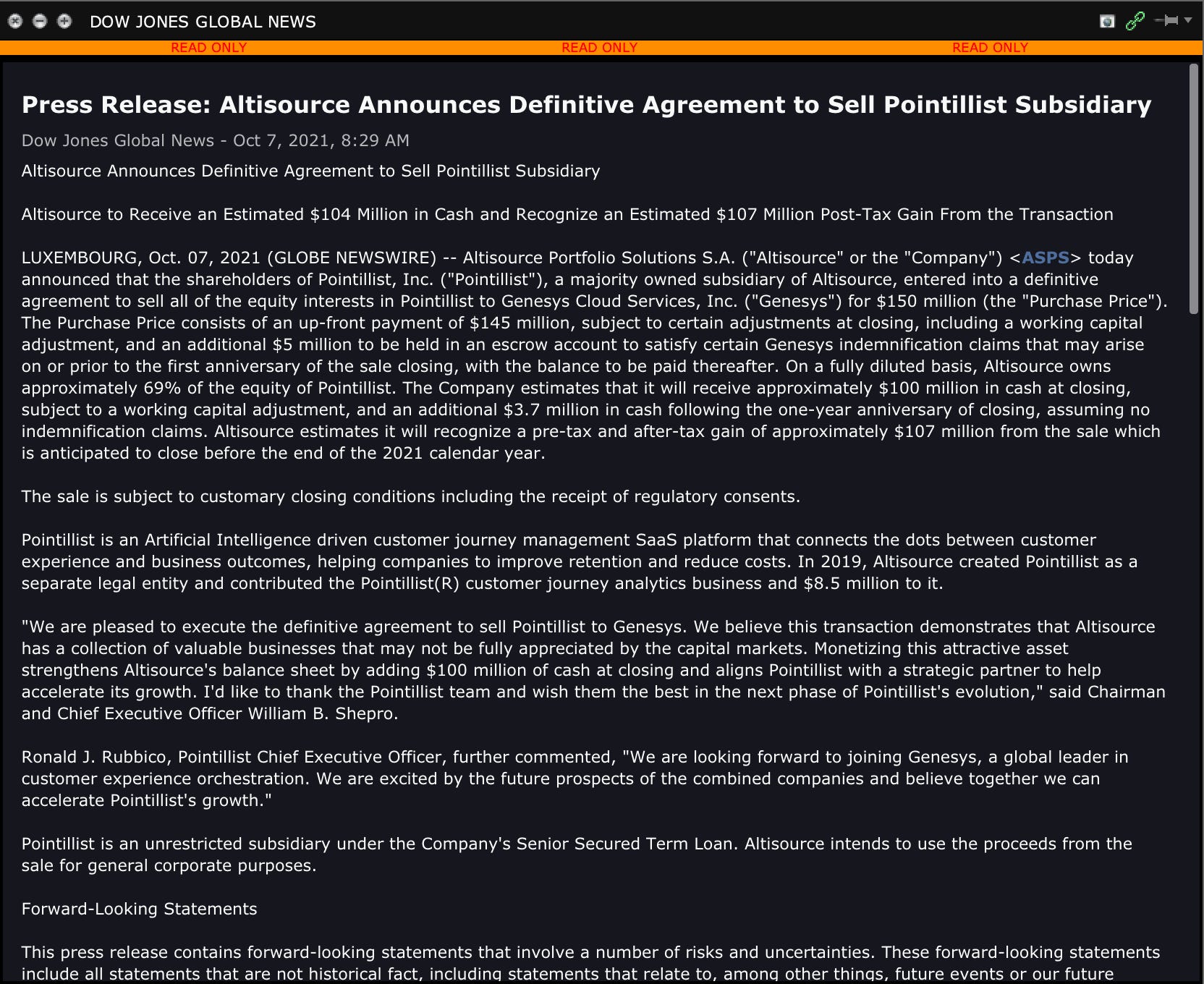

I hadn’t given much thought to the situation for months, other than casually checking foreclosure stats (and confirming that numbers were indeed rising), until a few days ago I saw a news alert from the company that they were selling a software system for managing lead flow called “Pointillist” for $150M (which they owned 69% of). $150M was literally the opening market cap on the company that day. This software package only had around $12M in revenue, like 3.5% of the company’s total revenue.

Ok, wow. This seemed too good to be true. The proceeds of this transaction - a net of almost $100M - would pay off nearly half the outstanding debt. I had never even factored in this app into my assumptions around the company’s value. I figured the ancillary businesses as stupid, money losing vaporware that had negative value.

Man, was I wrong! The stock rocketed 40% in the last two business days (and I myself doubled my position the morning I read this news). This single transaction, selling an asset literally no investor had ever mentioned or seemed to care about, would add $7 in book value to a $10 stock. That got me thinking - what will the origination business sell for? What’s the rest of the business worth?

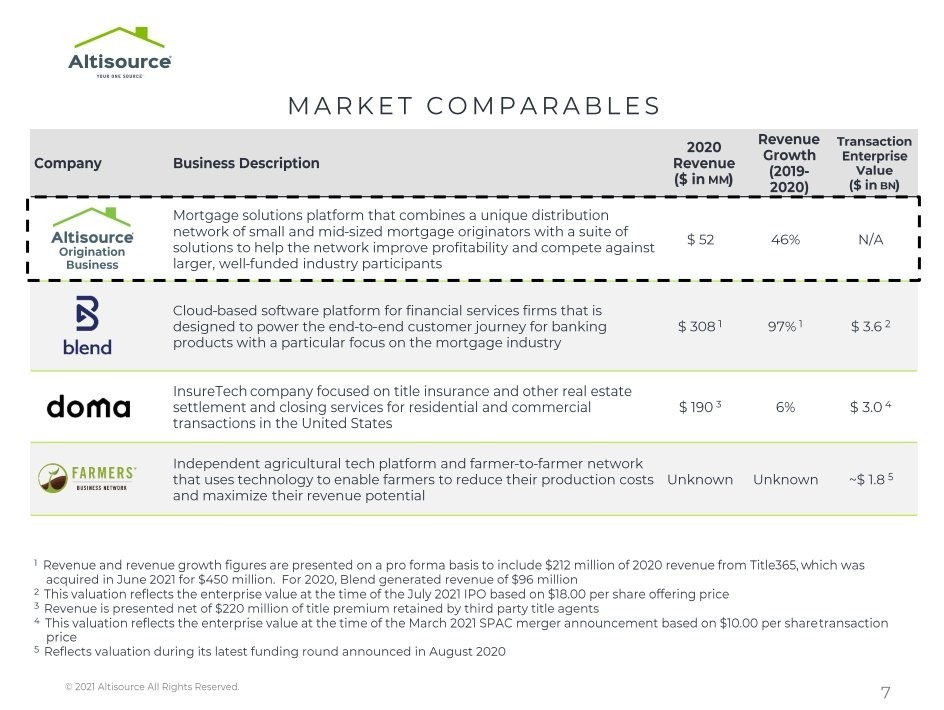

Well, the origination business as of last quarter was set to do around $60M in 2021 after growing 46% in 2019-2020. It grew 16% in Q2 21 alone. One thing I do know, investors love to buy growth, and ironically, struggling Altisource had managed to engineer some high growth businesses as its bread and butter went stale and sour due to multiple factors outside its control.

When I first saw the origination business being up for sale a few months back, I figured there would be no way they could get the sort of valuations their comps got - 10-15x revenue. But after the Pointillist transaction I started asking myself - what if they could? We’re talking $600M at 10x, $800M at 15x - $40 to $50 per share in value creation out of nowhere. Even at 1-2x TTM, it would mean paying off another substantial chunk of the outstanding debt, maybe even all of it, leaving the core foreclosure business I wanted to invest in anyway, along with several other ancillary businesses. What are those parts of the business worth?

Out of pure dumb luck and looking somewhere nobody else bothered to, I truly stumbled into money falling from the sky on this one. The Pointillist transaction hasn’t closed yet, but you can bet I’ll be buying any dips. They say there are no free lunches in markets - this sure looks free to me. At the very least, the company has bought itself years of runway and has assets which are much more valuable than anyone suspected. The bull case, well, you can use your imagination regarding real estate market cycles and where interest rates and monetary policy are going.