ASPS Q4 21 Earnings

Expected asset sale adds cash to balance sheet, while top line revenue declines and adjusted loss shrinks

The market is reacting badly to Altisource earnings (-12.5% at time of publishing, to ~$10) on a headline adjusted loss of $0.86/share. GAAP income for the quarter was $4.40 factoring in the Pointillist sale. Here’s the good, the bad, and the ugly.

The Good

As expected, the sale of the Pointillist subsidiary sale closed, adding cash to the balance sheet and reducing debt. In total, the equity deficit decreased from 141.7M in Q3 to 68.9M in Q4. In other words, the Pointillist sale in the end added ~72.8M to the balance sheet and reduced the long term debt. The difference between the realized sales price (of which Altisource netted ~$100M) and the net add to equity mostly represents losses incurred since the deal was announced. The after-tax gain on the sale was $88.9M.

The other positives are that the quarterly adjusted loss was further reduced. Pointillist was always a net drag and the fact that they were able to unload it for so much was a real surprise. Operating expense decreases have more than offset revenue declines.

The company is currently forecasting a return to positive EBITDA (they did NOT say GAAP profits) later this year.

The Bad

Unfortunately ASPS is no longer going ahead with the origination business sale. Presumably, they couldn’t find a buyer for the (truthfully ridiculous) price they were asking, and decided to keep running it. On the plus side, it seems to be outpacing industry growth.

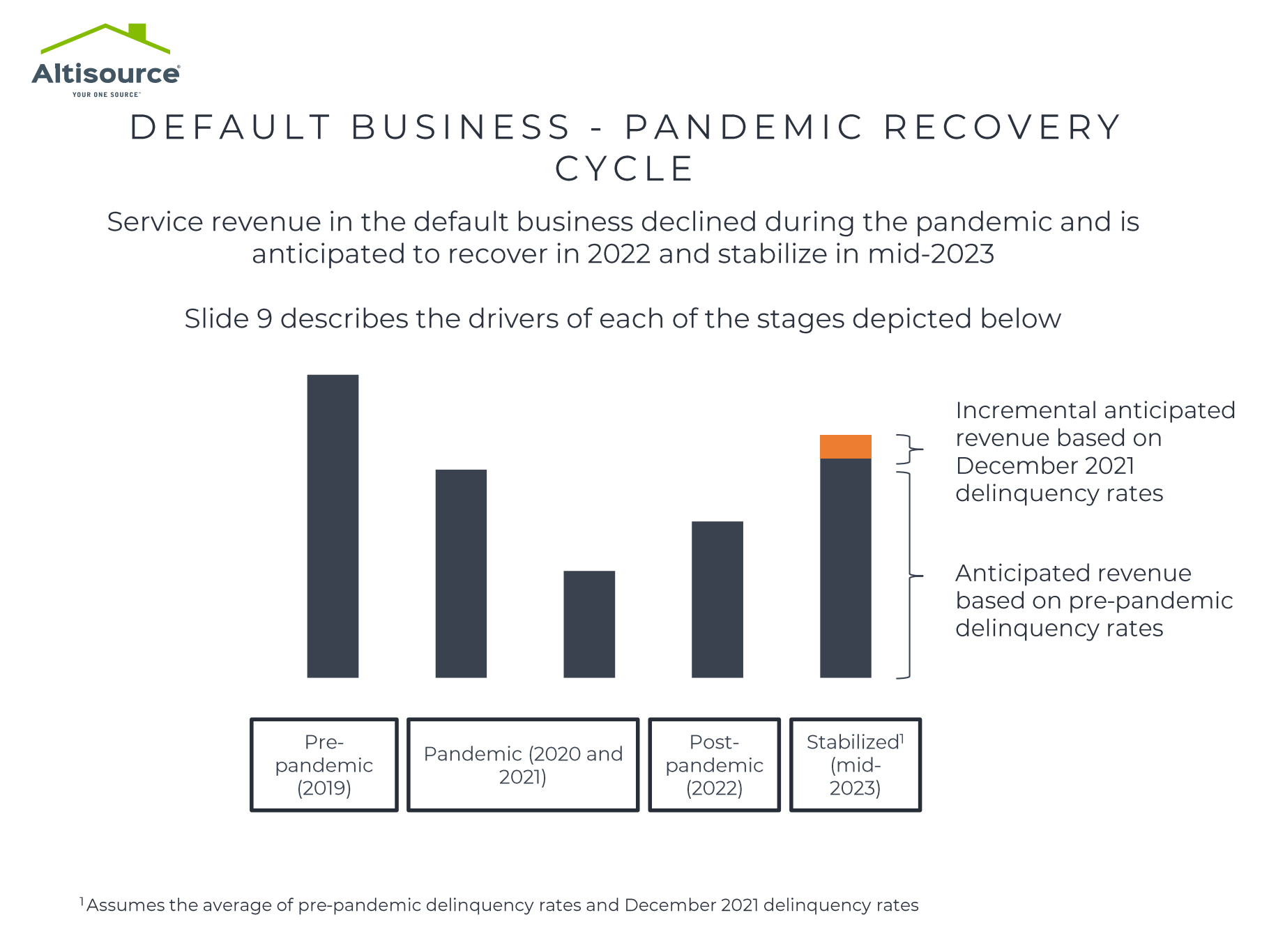

Top line quarterly revenue declined yet again, though more than half of that was expected as Pointillist is no longer contributing to top line revenue (estimated quarterly revenue from Pointillist was a bit more than $3M).

The Ugly

Despite an increase in foreclosure starts and the end of the moratorium, Hubzu, Ocwen, and all other referral revenue declined in Q4.

While this seems disastrous on the surface, and it is possible the company is doing a poor job of executing, it is important to remember that a foreclosure process takes months. It’s a leading indicator rather than something that shows up in quarterly financials right away.

The company is still forecasting continuous improvements based on December 2021.

My Take

I am disappointed that ASPS will not be moving forward with selling the origination business. I was always most interested in the foreclosure business, and I am not super happy about exposure to the other side of the housing market.

That being said, As of writing, ASPS is once again trading below the level that the Pointillist sale was announced, and foreclosures have increased significantly. As Black Knight recently stated:

Foreclosure Starts Surge Sevenfold in January, Hitting Highest Level in Two Years; Though Volumes Rising, Still 20% Below Pre-Pandemic Levels

This is always the trend I was betting on, and the macro level trend is indeed slowly playing out. Anyone who expected it to happen in a month or two was always going to be disappointed. The longer term picture is that we are in an inflationary environment with more macro risks than we’ve had at perhaps any point in decades. Interest rates are going up and due to the Russia conflict, world trade will contract.

This is a recipe for a poor economic environment which will result in more financial distress. Assuming Altisource can execute, and I make no claims on the ability of management to do that - the operating environment for Altisource should become increasingly more favorable. I’m keeping my long position and will likely add on continued weakness.

If the company is able to execute, I still see a potential repeat of their performance in the last cycle, when shares went from roughly today’s prices to well over $150/share, on a much higher share count. The company put excess cash in the last cycle into repurchasing shares. Though again, I make no claims about the ability of ASPS management ability to execute, the idea that foreclosures will return to pre pandemic levels and beyond is still my highest conviction bet. Altisource remains the most accessible way to make that bet.