Is it different this time?

A brief history of bubbles

“Booms start with some tie-in to reality, some reason which justifies the increase in asset values, and then — and this is the critical feature of speculative mood — the market loses touch with reality.”

— John Kenneth Galbraith

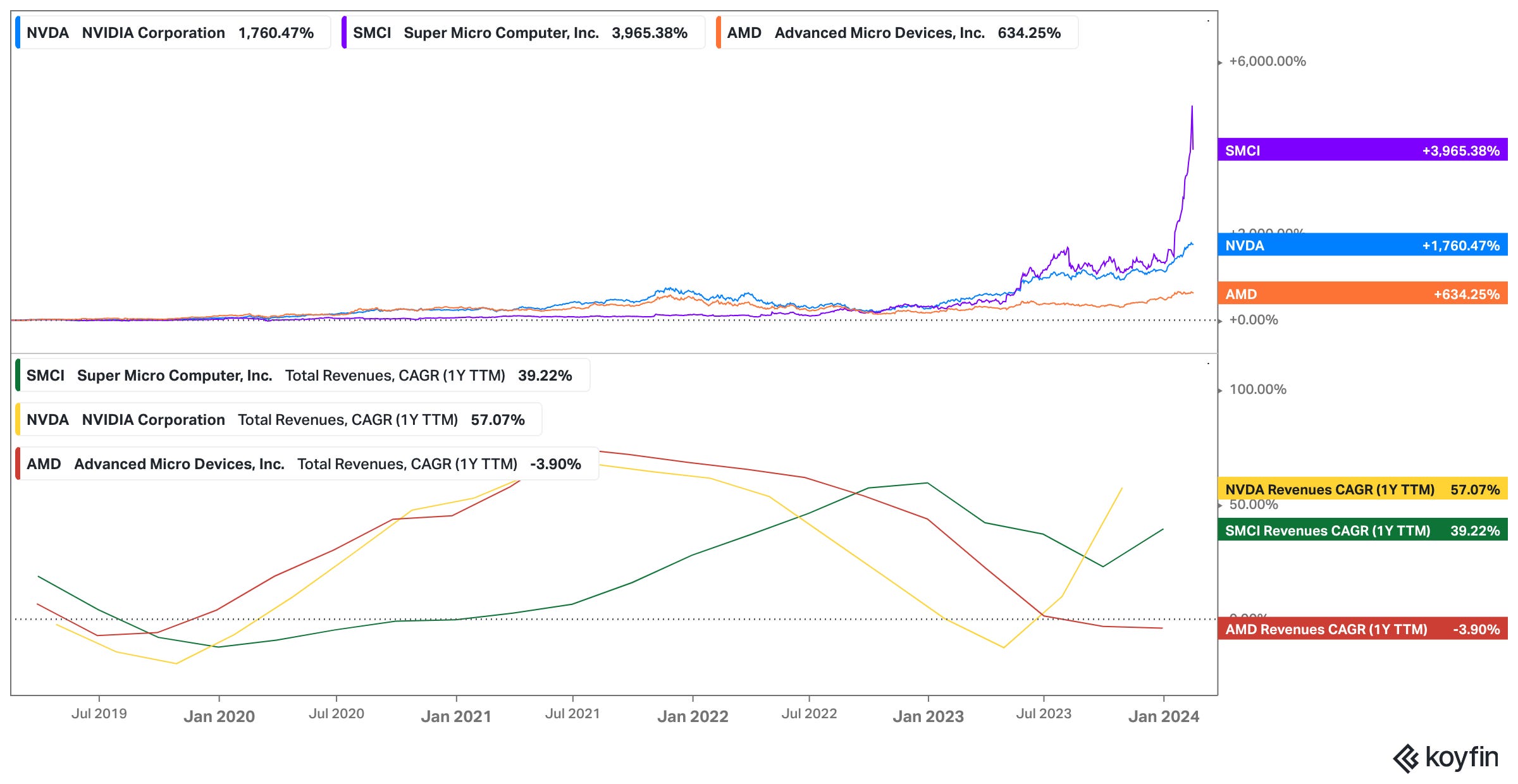

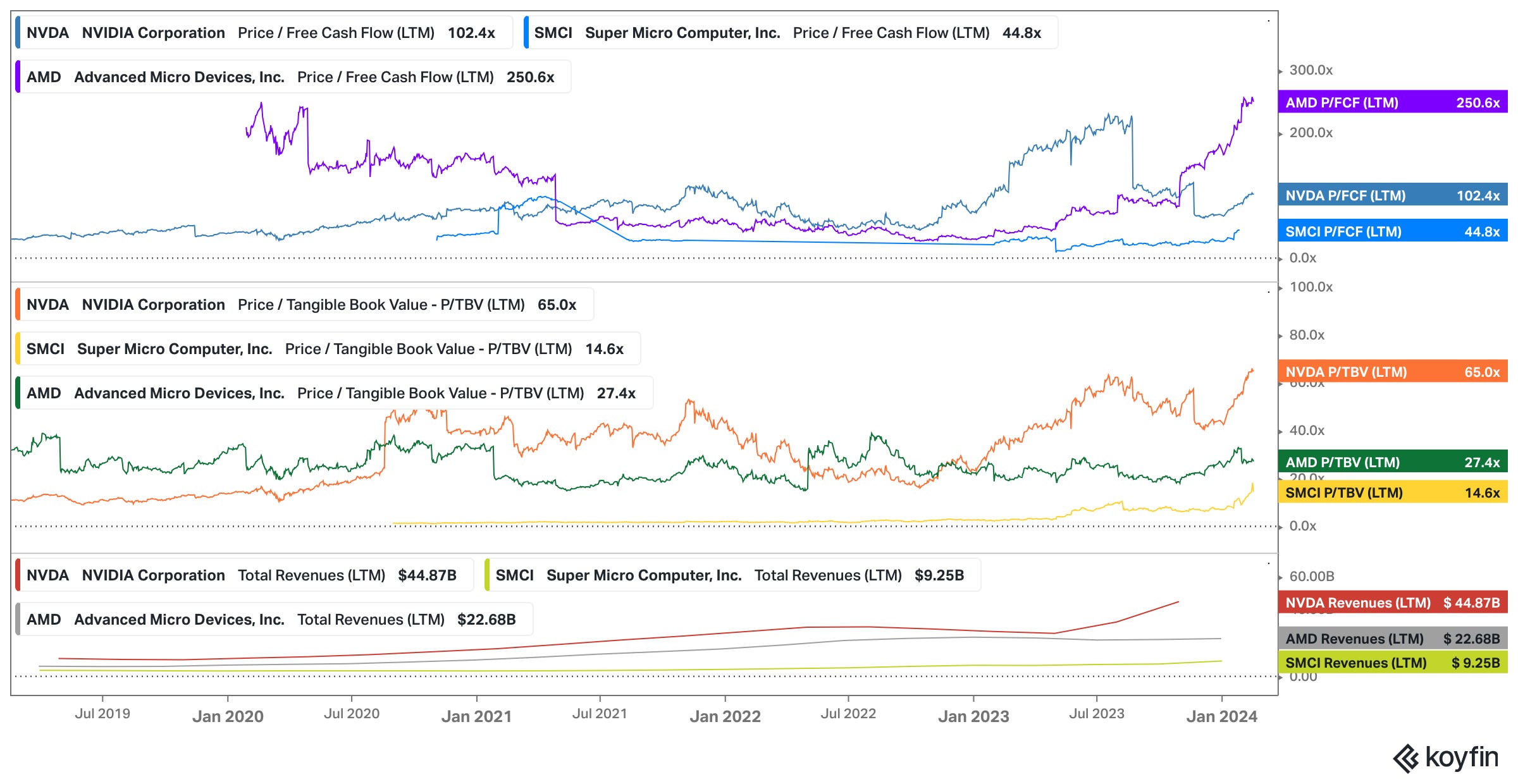

Well, we’ve all seen the stock price charts on NVDA and SMCI. Perhaps you’ve even made some money chasing. Perhaps we should all be making money chasing. And this is exactly what bubbles are made of.

To be clear, there is certainly some logic for why these company stocks have skyrocketed (along with others like TSM, Qualcomm, and Broadcom, not to mention the Magnificent 7).

Every couple of generations at most, for the last several generations, there comes along some transformative breakthrough which promises to change everything. Here are some of the narratives that have accompanied historic bubbles:

- 1750 “New trade routes in the east will bring untold riches to those who can exploit them.”

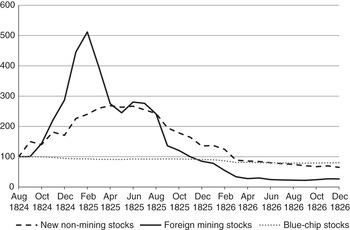

- 1824 “Mining company shares in the New World will bring vast riches to Europe.”

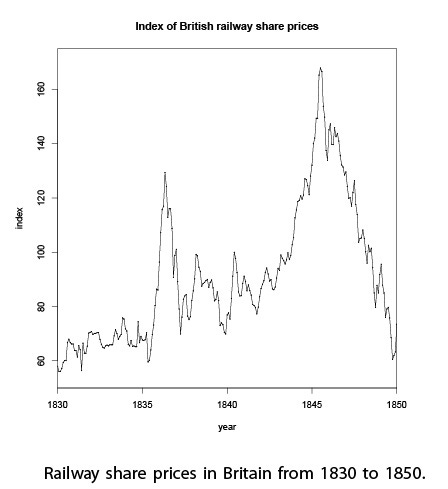

- 1845 “Railroads will connect the world like never before.”

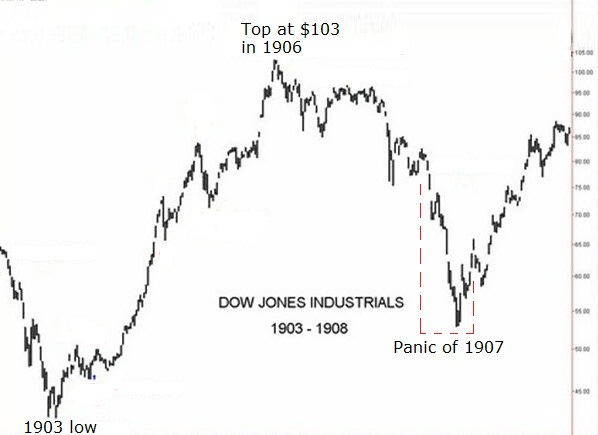

- 1907 “The Telegraph will connect the world like never before.”

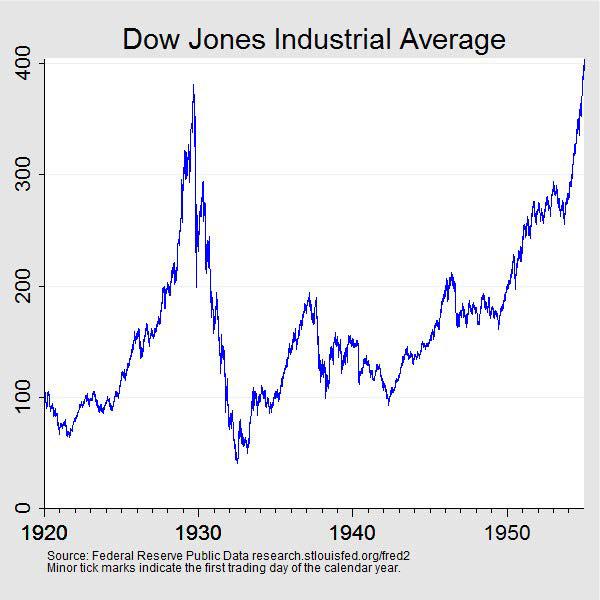

- 1929 "Consumer credit, television, radio, and automobiles…Stock prices have reached 'what looks like a permanently high plateau."

- 1980s “Japan's high growth rate is unique, eue to economic institutions and policies...the growth appears to be exceptional and sustainable.“

- 1999 “The internet will connect the world like never before.”

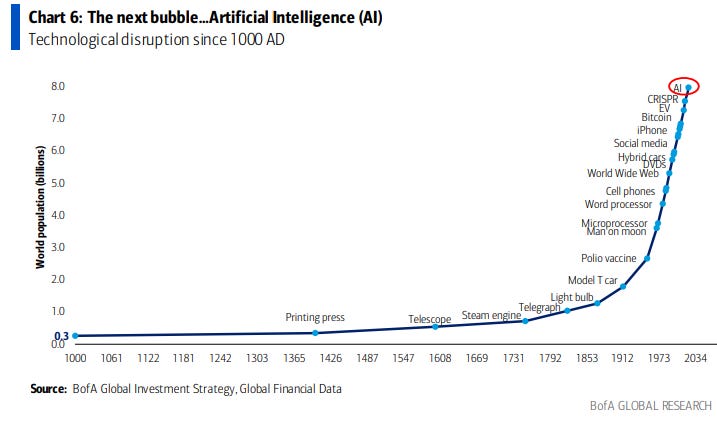

- 2024 “AI will connect the world like never before, and free humanity from labor.”

In many of these cases, the long term narrative was proven directionally correct (though the jury is out on AI) - what was incorrect was the assumption that those things could go up in a straight line forever.

While you can make the argument, “if you kept holding, you did just fine”, the issue is that:

A) Nobody has the patience to buy at 1000 and drop back to 100 and then wait 20 years

and

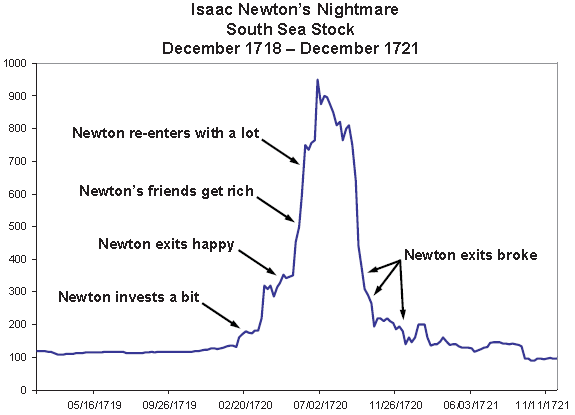

B) The securities / investment options that are present at the beginning of a bubble may not be the companies that in the end build lasting, profitable businesses (almost none of the shipping companies that existed in 1720 exist today, most emerging market mines closed a century ago, many technologies were obsoleted by another within a generation).

Let’s look at some charts.

The South Sea Bubble

The EM Mining Stock Bubble

The Railroad Mania

The 1907 (Telegraph) Bubble

The 1929 Bubble (Television, Radio, and Automobiles)

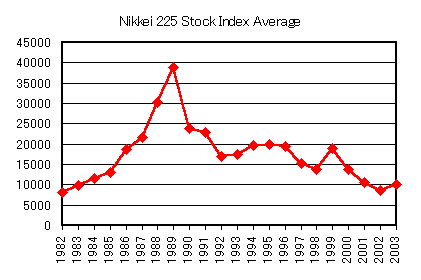

The Japan Bubble (1980s)

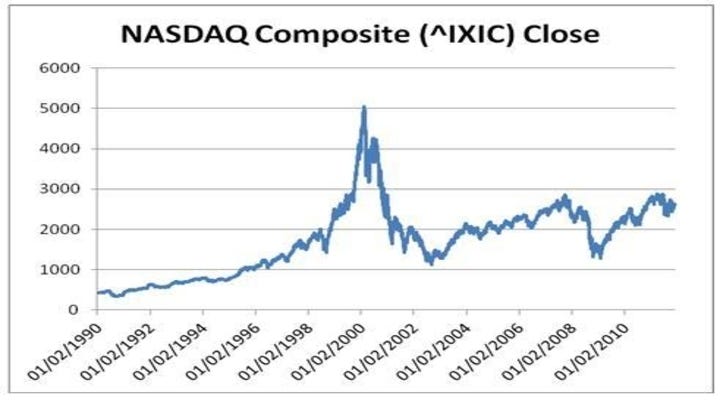

The dot com Bubble (1990s)

The AI Bubble?

I certainly haven’t included an exhaustive list of bubbles here, the larger point is that it’s always the same over medium term (10 years or so). Number goes up, then number goes down. As Jesse Livermore stated, “human nature never changes.”

To anyone who has made a lot of money betting on AI or crypto currencies (and I personally participated and benefitted from crypto, though I was very early), the key lesson is that while the appreciation based on growth rates may seem sensible in the short term, you never see what you don’t see coming.

While this generation of AI (Large Language Models) seem to perform well using GPUs, which has driven NVDA demand, we must consider that we don’t know what the future looks like. I myself was a crypto currency miner (albeit a hobby miner). I built my first miner in 2013. I saw the progression go from CPU mining, to GPU mining, to ASIC (specialized computing) mining. I know that a risk factor for crypto (and lots of other current computing concepts) is a breakthrough in quantum computing that renders current technology obsolete.

The only constant of the past thousand years has been constant and accelerating disruption. 100 years ago, Henry Ford was a genius and a visionary, now his car company still exists, but has trailed S&P 500 returns for decades. IBM, once “the” computing company, hasn’t made a new high since 2013.

All of this may sound like the grumbling and cope of someone who missed the latest bubble. It is, and it isn’t. The idea that strong current growth can be extrapolated to infinity is constantly proven wrong. It was wrong with railroads centuries ago. It was wrong with Tesla just recently. The issue with chasing bubbles is that you never know when they’ll pop, and you can get ruined buying the top or buying the dip. There’s nothing wrong with a little gambling once in a while - all things in moderation, as Socrates said. But you should treat obvious bubbles with the same sort of skepticism and caution that you would treat a casino. Going all in on one thing, at historically high valuations, having no control over the events that unfold next - that is essentially like betting it all on red at the craps table.

“I didn’t get rich by buying stocks at a high price-earnings multiple in the midst of crazy speculative booms, and I'm not going to change.”

— Charlie Munger

The Sustainable Way of Building Wealth

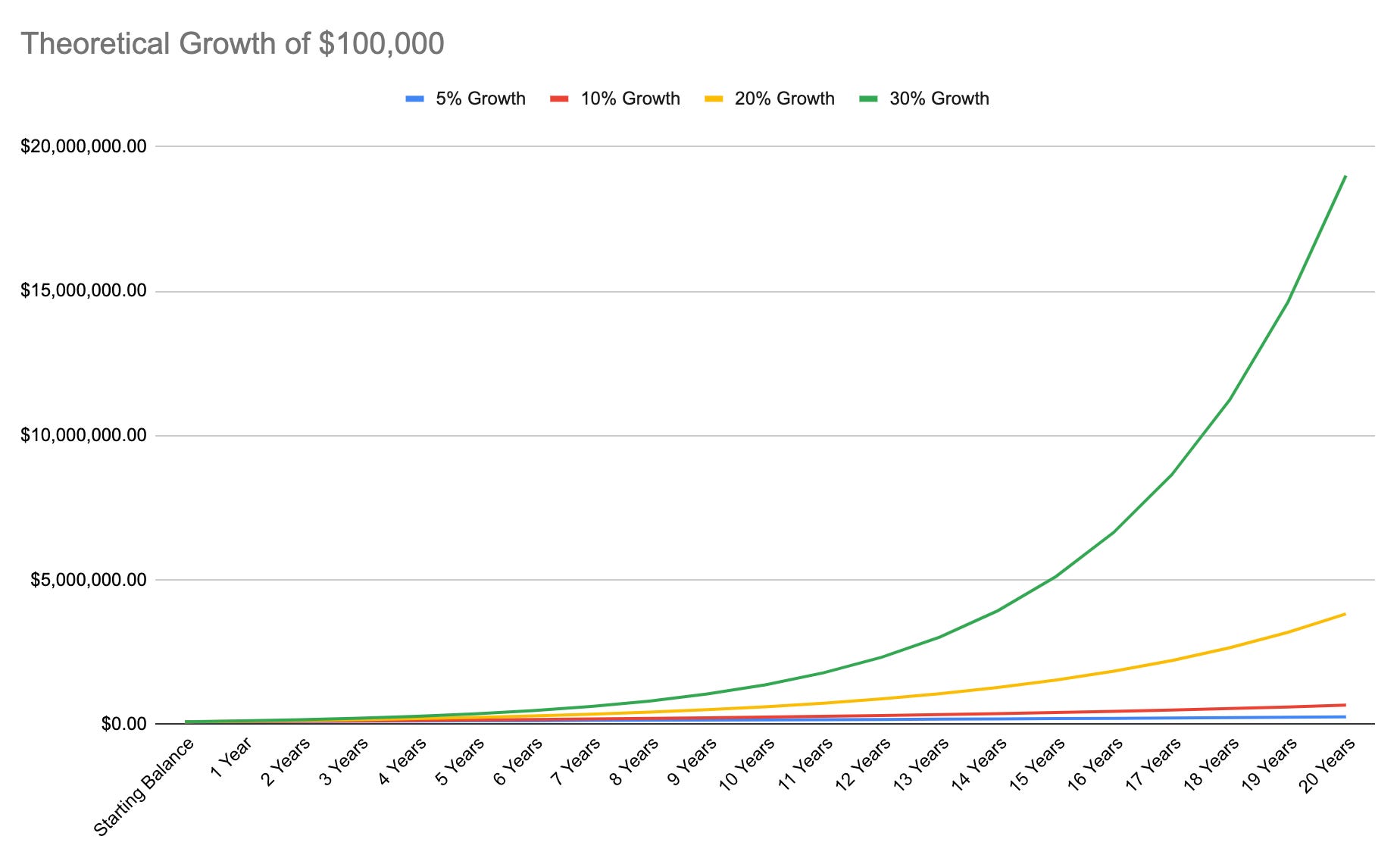

While it may seem quite pedestrian to focus on getting low but sustainable returns in the market, and some may argue that it’s impossible to get more than around 10% consistently (the average annual return of the S&P 500 for the past 30 years is ~10%), I have myself increased my net worth by 10-20x in the past 5 years, depending on whether or not you include private company valuations in net worth. Very little of this came from bubble chasing.

While I have caught few bubbles, I have had strong growth nearly every year.

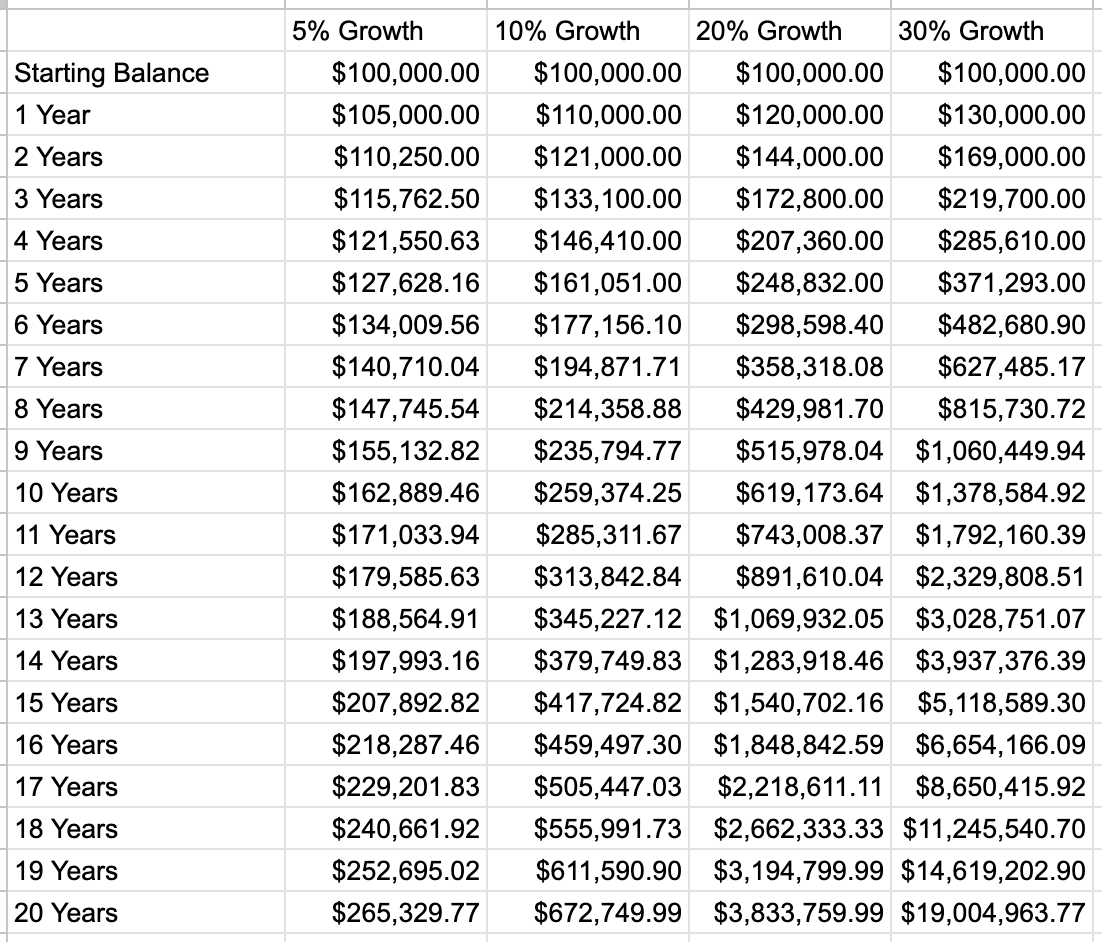

If you look at the tables above, you can see how quickly you can compound even $100,000 in wealth at 20-30% per year. You can become a millionaire in about a decade if you can achieve that sort of growth rate through your investments and entrepreneurship. The key is balance. Avoiding big drawdowns, while achieving strong returns in at least a few areas, will make you sustainably wealthy. From lottery winners to heirs, many people who have a large influx of undeserved cash see that money dwindle away.

Long term wealth is about capital growth and preservation. As amounts become larger, protecting your nest egg involves a lot of diversification, tax optimization, and estate planning. It likely involves many asset classes as well as private businesses and alternative investments. It likely involves more than one jurisdiction. Sustainable wealth doesn’t come from bubbles, it comes from staying in the game for a long time, while making strong returns, even though those returns may be modest in the eyes of bubble enjoyers.