Sasol had a great week - breaking down the story

When I first said you should keep an eye on Sasol nearly a year ago, the stock was trading just under $8/share and had been selling off from a peak of just under $27/share since the summer of 2022. Sound familiar? Many chemicals and energy companies have followed this same path.

Now I think the time has arrived to become more aggressive on Sasol and I want to break down the story and the value.

A history lesson

Sasol's story begins in the early 1900s when German chemists devised new processes to create synthetic fuels. Essentially, an energy source and a carbon source are combined to create a synthetic, gaseous form of hydrocarbons, which can then be converted into liquid fuels. The earliest experiments focused on doing this with coal, something that industrialized but oil poor Germany had a lot of.

German chemist Friedrich Bergius was the first person to have successfully created synthetic motor fuel from coal, and these ideas were further developed, ultimately culminating in the Fischer–Tropsch process during Weimar era Germany. Franz Fischer and Hans Tropsch, the inventors of this process, filed US patents, which were eventually acquired by KBR Group, the industrial conglomerate founded by M.W. Kellogg, which at the time was a powerful US concern involved in the construction of power plants (and to this day is a multi billion dollar conglomerate).

By WW2, the Fischer-Tropsch process was used for supplying 1/4 of all automobile fuel needs in Germany. Much of this infrastructure was destroyed during the war, but at least some people outside of Germany - including in the United States and South Africa - were paying attention to how the Germans had figured out how to create petrol fuel without oil.

South Africa had similar problems. It was coal rich, but didn't have many oil deposits. In the 1920s, South African scientists, with the support of the coal mining Trade Associations and specifically a company called Anglovaal Group, began looking at the work being done in Germany. They funded scientific research to replicate the results, purchased the patents for the Fischer-Tropsh process, and in 1950, founded Sasol.

It took Sasol 5 years to build the original coal-to-liquids terminal in Sasolburg, now by far the largest implementation globally of the Fischer–Tropsch process. In March 1955, they sold their first commercial fuel. A dream nearly thirty years in the making had been realized. By 1960, Sasol was still a "garage band" business with an annual turnover of just 1.36M ZAR, but this would all change during the 1960s as the company first began building a distribution network of pipelines across South Africa and in the late 1960s as fuel prices began skyrocketing, investment started pouring in. The company built a large refinery and by 1971, was supplying the fuel for Formula One racing. By the mid 1970s, Sasol had literally built two towns - Sasolsburg and Secunda - refining and coal mining operations, and had thousands of employees. By the end of the decade, Sasol was a public company.

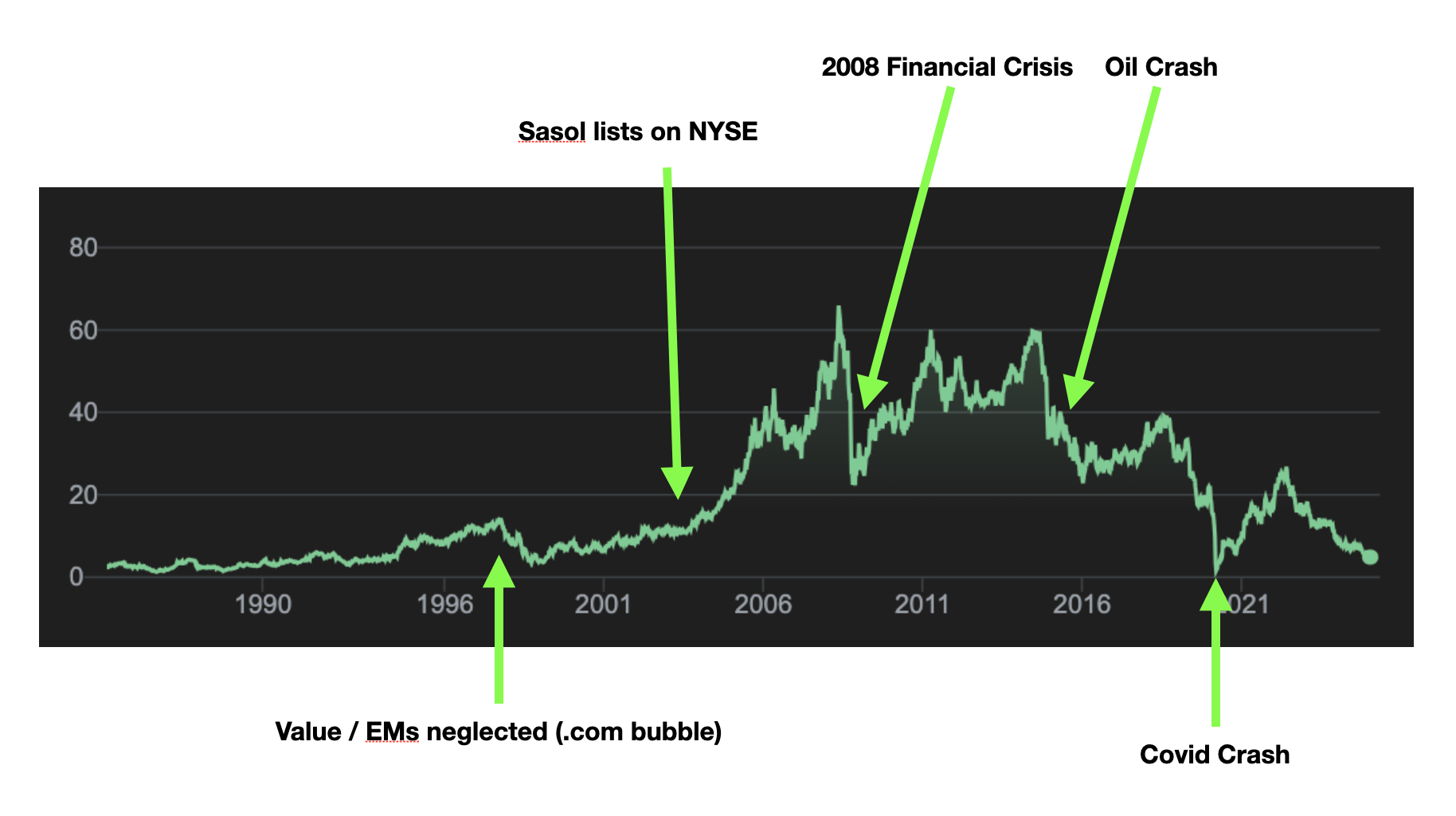

As the 1980s progressed, Sasol grew by leaps and bounds, expanding into chemicals, fertilizers, and ethanol. Sasol became the largest company in South Africa and began diversifying into other countries. In 2003 they listed on the New York Stock Exchange. Now here's where Sasol goes from an incredible growth company, one of the most innovative in the world, to for essentially 20 years, just being a cash cow with a share price that has gone nowhere.

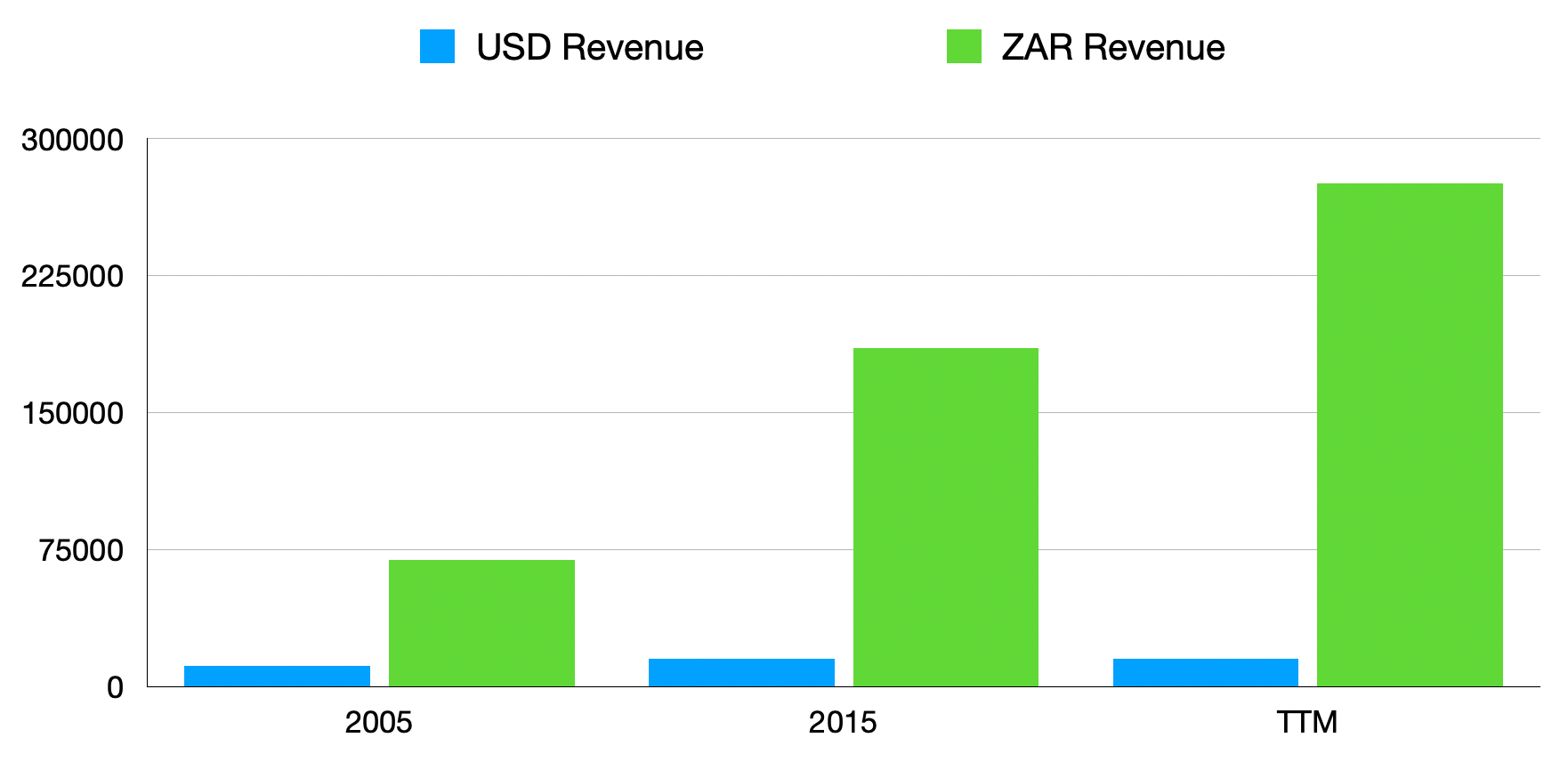

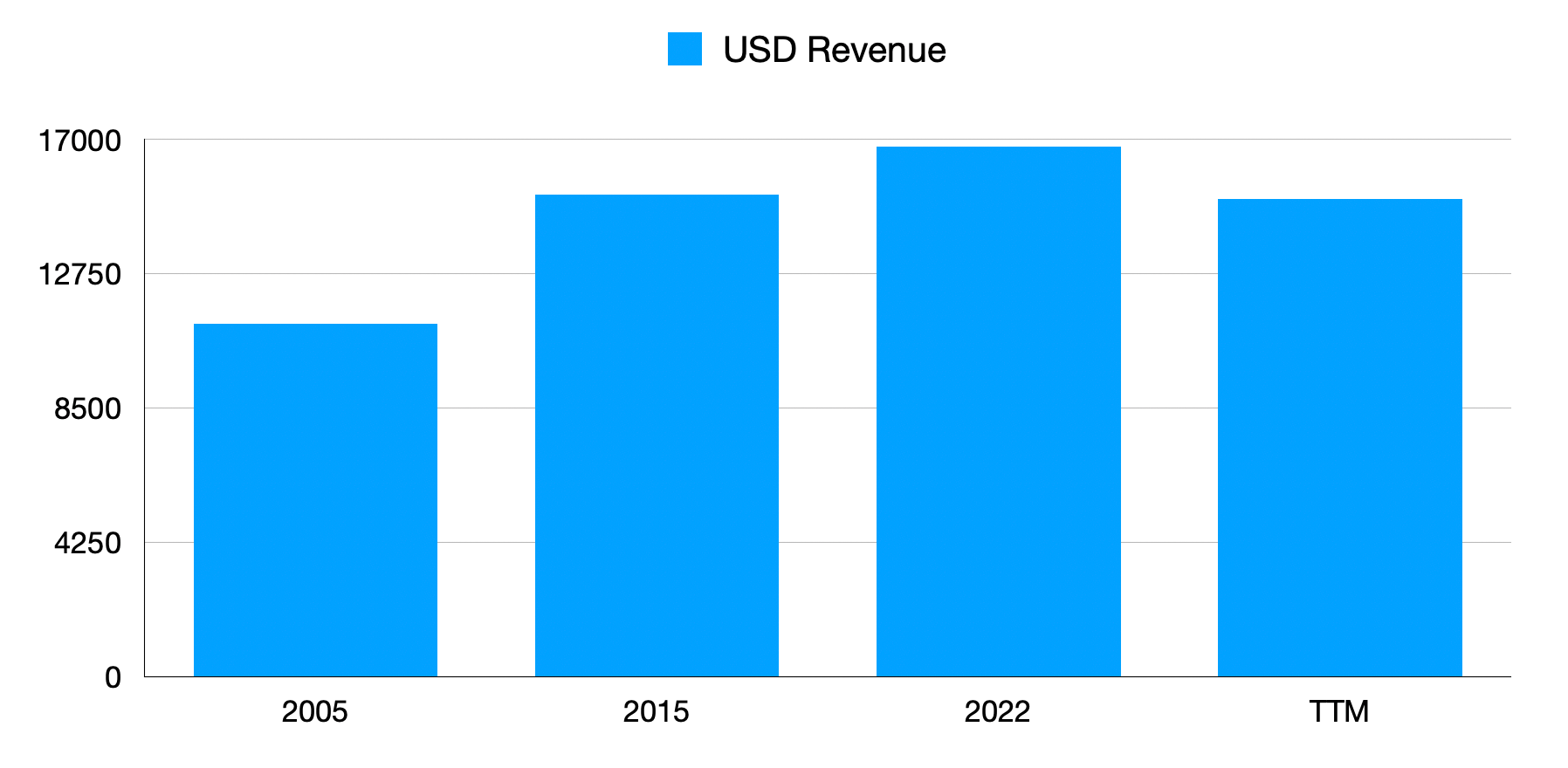

While Sasol has managed to keep up with South African currency devaluation and even grow its USD revenues around 50%, it hasn't kept up with the growth rate of the US economy for instance - GDP has more than doubled since 2005 while Sasol's revenue growth has only been 50%.

Now, that being said - Sasol traded at nearly $40/share as recently as 2018 and at more than $25/share in 2022 when its revenues hit their long term peak. The stock now stands at $5/share, a price not seen in decades other than briefly during the covid period.

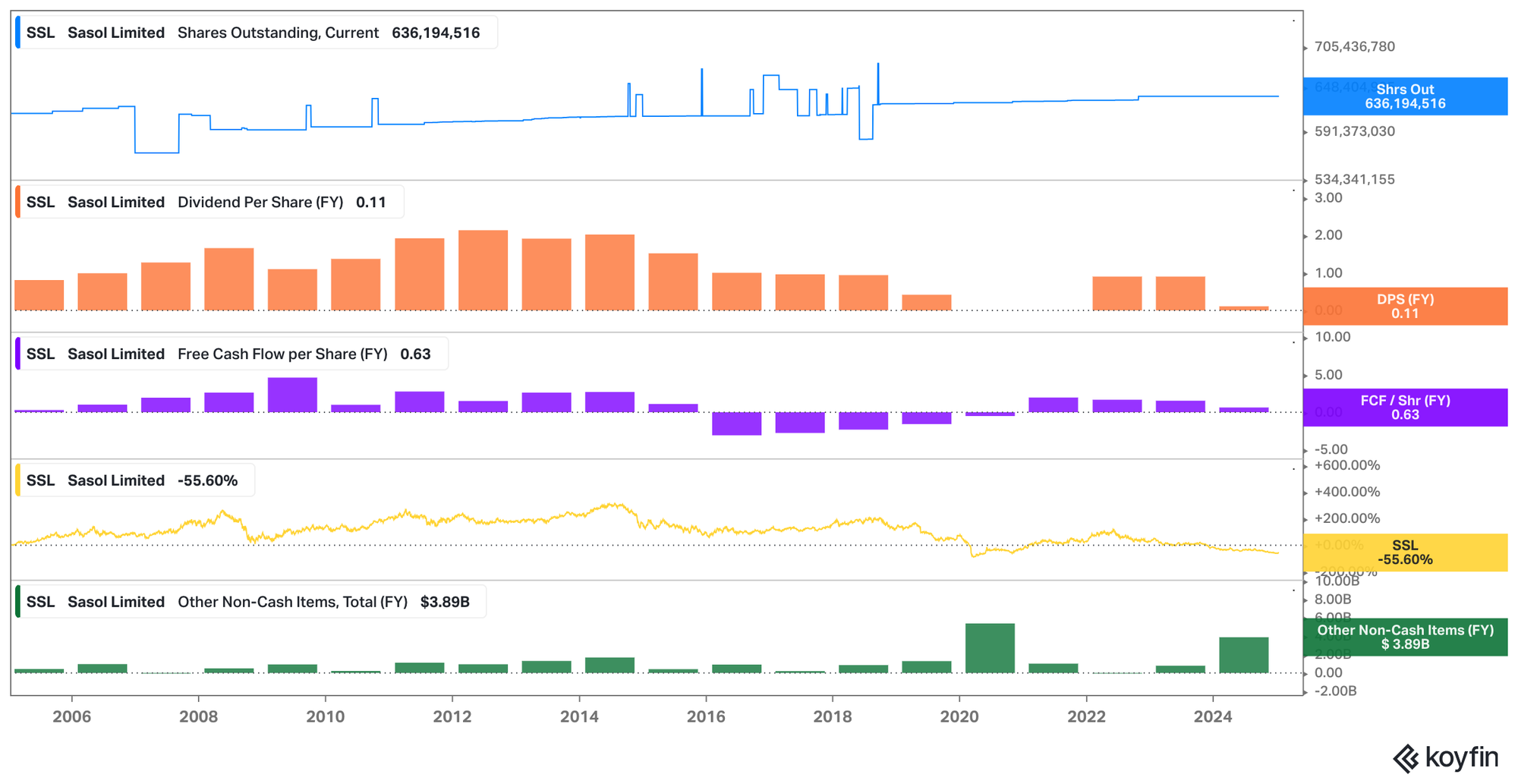

Though the dividend has recently been suspended in favor of debt pay down, this is a company that has generated $5.83/share in free cash flow since covid and paid nearly $2 in dividends. A decade ago the company was paying $2/share in annual dividends with approximately the same level of revenue.

As you can see in the green chart at the bottom of the Koyfin comparisons above, the large non-cash items (impairment charges) are masking what is a business that can still produce a significant amount of free cash flow.

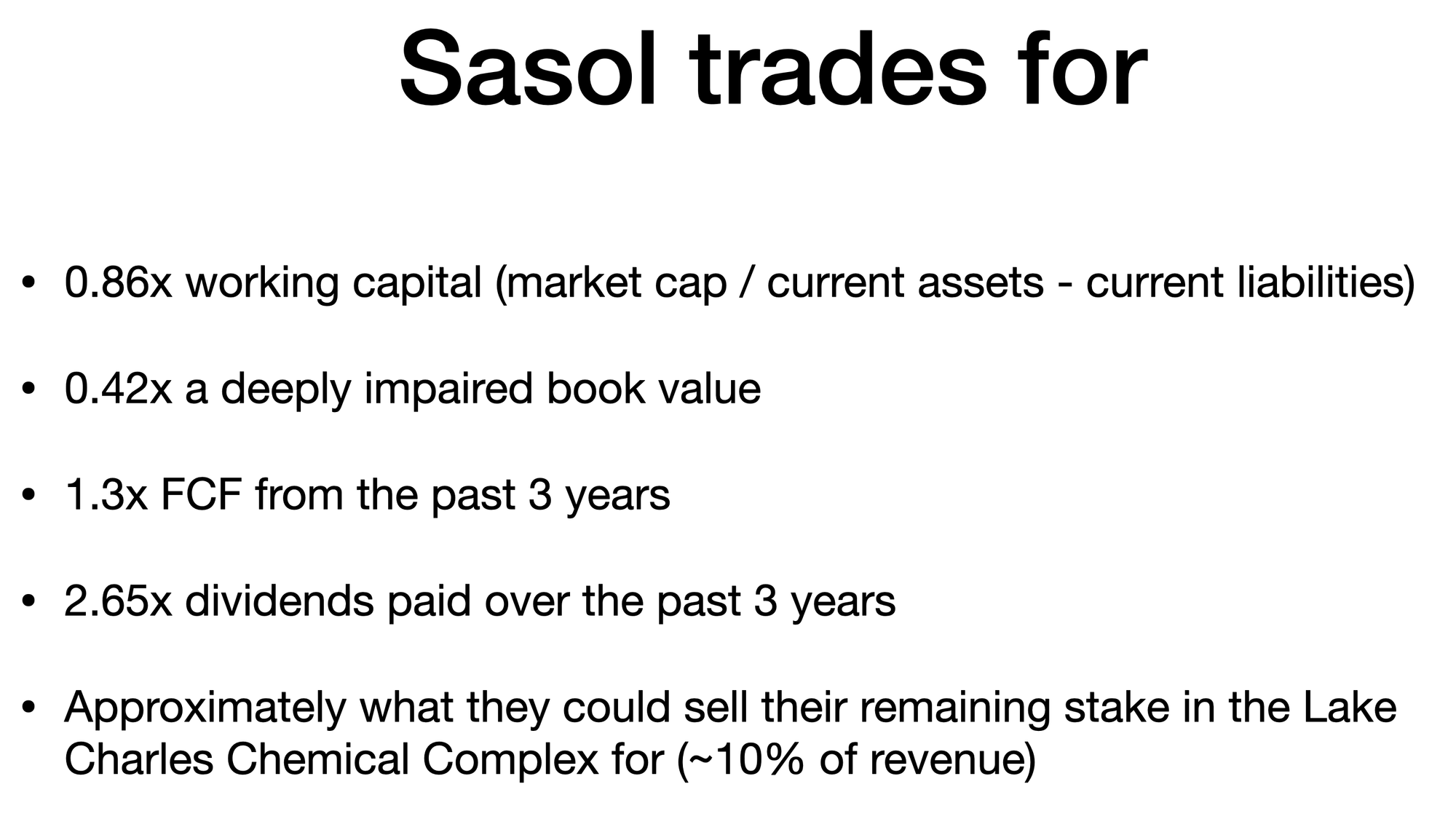

Look, Sasol has hair, as many of my ideas do. It's a mature company with 50% of its revenue in a largely dysfunctional state. But my contention is that Sasol shares purchased today are likely yielding 10-20% annually at some point in the future, and that the business is in fact, too big to fail quickly.

Now let's talk about why it got so cheap, and about catalaysts that make it very probable that Sasol will make another run at much higher prices.